|

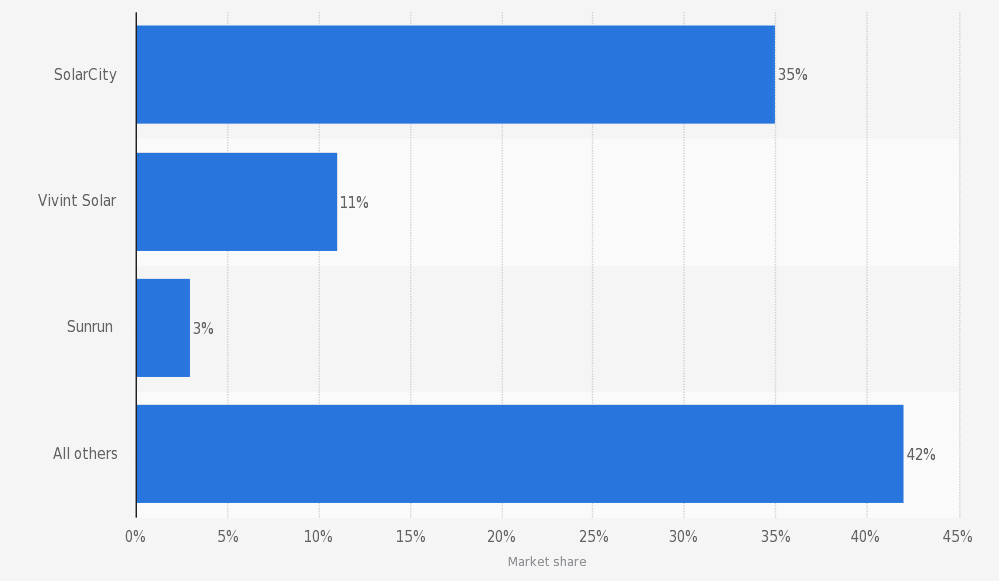

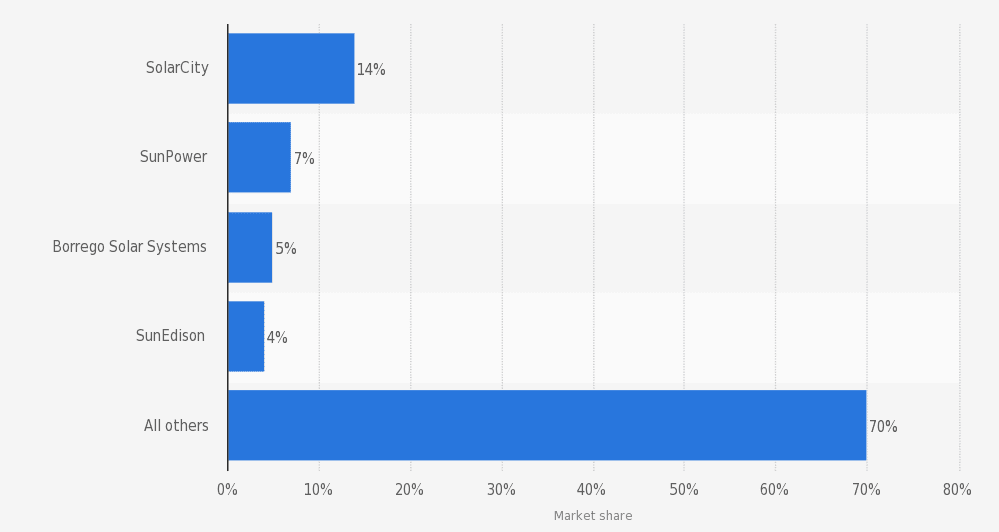

Fragmented Commercial and Industrial Marketplace The recent barrage of articles detailing the bankruptcy of a renewable energy giant (SunEdison) and the pending sale of Elon Musk’s third favorite company (SolarCity) has been nothing short of suffocating. IronOak Insights contributed our own sobering account to the stockpile of SolarCity acquisition articles last week as we didn’t want our readers to think that we were living under a rock. But outside of those two headline grabbing companies lies a diverse ecosystem of large scale developers working to expand the commercial and industrial solar landscape. Per the graphs below, while only 42% of the U.S. residential solar market in 2015 was serviced by regional installers, 70% of the C&I solar market in 2015 was serviced by companies whose names were not SolarCity, SunEdison, Sunpower, or Borrego Solar. Let’s dive into some of the activity within the fragmented C&I solar marketplace. Leading Residential Solar Installers in the U.S. in 2015 (market share by MW installed)  (Source: Statista) Leading Non-Residential Solar Installers in the U.S. in 2015 (market share by MW installed)  California’s Cash Crop

As the perpetual leader in the U.S. solar race, California dominates every other state with its relentless pipeline of large-scale solar PV projects. The state’s consistent appeal exists because above-average electricity rates are coupled with some of the best insolation in country, along with a small state program called the California Solar Initiative. In addition to solar electricity generation, all of that sunshine has long supported California’s agriculture industry, and now California-based solar developers, like CalCom Solar, are targeting Ag companies as perfect companions for mid-scale PV facilities. CalCom recently completed a 2.2 MW solar farm for a fruits and vegetable grower, and the single-axis tracker installation now stands as the largest customer-owned, net metered system in Monterey County. CalCom is one of many developers across the country that are leveraging USDA REAP (Rural Energy for America Program) grants along with the federal ITC to provide attractive PPA rates for applicable off-takers. PFMG Solar (Partners For Many Generations), a top 15 U.S. solar developer, also takes a targeted approach in California by focusing on mid-scale solar solutions for suitable school districts. PFMG recently completed a 1.5 MW installation for a California school district and they’re a likely candidate to pick up some of SunEdison’s solar assets related to education centric off-takers. Full Steam Ahead in Colorado and North Carolina Just this week, Xcel Energy received the Colorado Utility Commission’s approval to move forward with the utility’s plan to develop 29.5 MW of PV from community solar projects. This is welcomed news for Denver-based community solar developer SunShare who commissioned a1.5 MW community solar garden in Arvada, CO on June 21st. SunShare joins Community Energy and Clean Energy Collective as the three juggernauts supercharging the community solar space in Colorado. Community Energy made headlines recently when they offloaded six North Carolina-based projects to Duke Energy with a total capacity of 30 MW. North Carolina’s solar market has remained strong despite the repeal of the state’s lucrative 35% solar tax credit. San Francisco-based Ecoplexus also recently completed six projects in NC, totaling 54 MW and requiring $79M in total investment. Ecoplexus has 36 MW under construction and claims more than 1 GW in their development pipeline that spans across 12 US states and dispersed international development. The West Texas Solar Patch Have you ever imagined an oil field man camp with LED lighting, tankless hot water heaters, and bike racks? Me neither, but maybe that concept becomes a selling point for solar field workers relocating to West Texas for the impending solar boom. ERCOT, the grid operator that services 90% of the Texas electric grid, is anticipating more than 560 MW of PV to be installed in Texas during 2016. That’s more than double the 212 MW installed during the previous year. Texas already ranks 9th in the U.S. in terms of installed solar capacity, and many analysts are expecting that ranking to climb up in the coming years. Texas, specifically West Texas, has some of the highest insolation in the U.S., large tracts of suitable land, low regulatory costs, and above average electricity rates. Although solar produced electricity will only account for 3% of the state’s generation capacity in 2017, ERCOT is projecting solar to supply more than 17% of the state’s electricity by 2030. While a large percentage of the anticipated development will come from utility-scale developers including First Solar and Recurrent Energy, regional developers will still have the opportunity to fill a void in the marketplace. I recently spoke with a developer that was already complaining of long interconnection study delays, so make sure to get your paperwork started sooner rather than later. Comments are closed.

|

sign up for ironoak's NewsletterSent about twice per month, these 3-minute digests include bullets on:

Renewable energy | Cleantech & mobility | Finance & entrepreneurship | Attempts at humor (what?) author

Photo by Patrick Fore on Unsplash

|

© 2009-2022 IronOak Energy Capital, LLC | (888) 249-3013