|

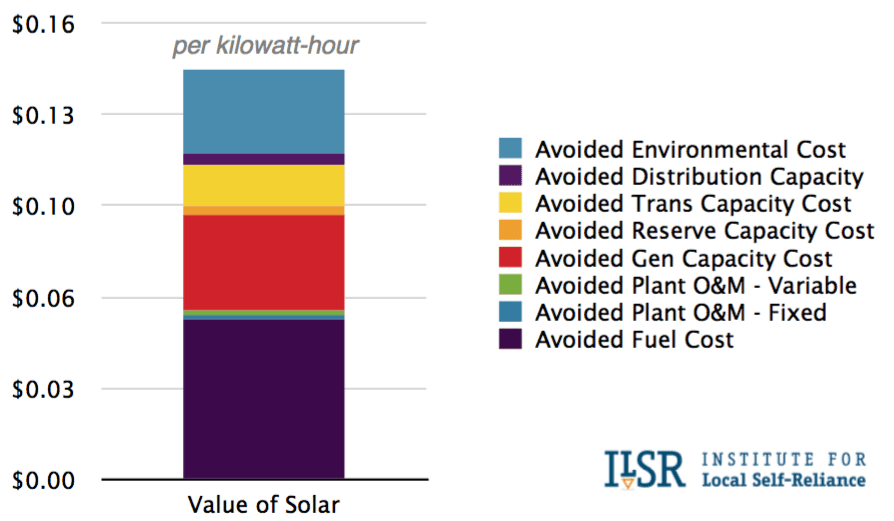

3/30/2016 What future Value of Solar policies could mean for the solar industry: 3 key things to knowRead Now There has been a wave of contentious net metering policy battles waged across the U.S. in 2016. Some net metering policies have remained largely intact, as in California, though much to the chagrin of the utilities. Other net metering policies, such as those in Nevada, have been fundamentally restructured, to put it kindly - though many would say they were just plain gutted. As with the ITC, a significant part of the solar industry formed around the net metering policy structure, and like many industries is reluctant to let go of such a foundational policy. But the aforementioned battles beg the question - is net metering the appropriate policy for solar looking to the future? Many believe that it has been a necessary stopgap policy measure, but not one that needs to live in perpetuity. One alternative that has been floated is the idea of a Value of Solar (VOS) policy that seeks to compensate solar based on a more nuanced understanding of the value that it provides to the grid. That is an easy enough idea to get behind, in theory, but just what could VOS mean for the industry?  (Source: Institute for Local Self-Reliance)

Utilities and solar investors both come out on top with a VOS policy

Avoided costs hold the key to understanding how the “Value of Solar” is framed

Playing up the environmental costs angle could be the greatest strength of VOS

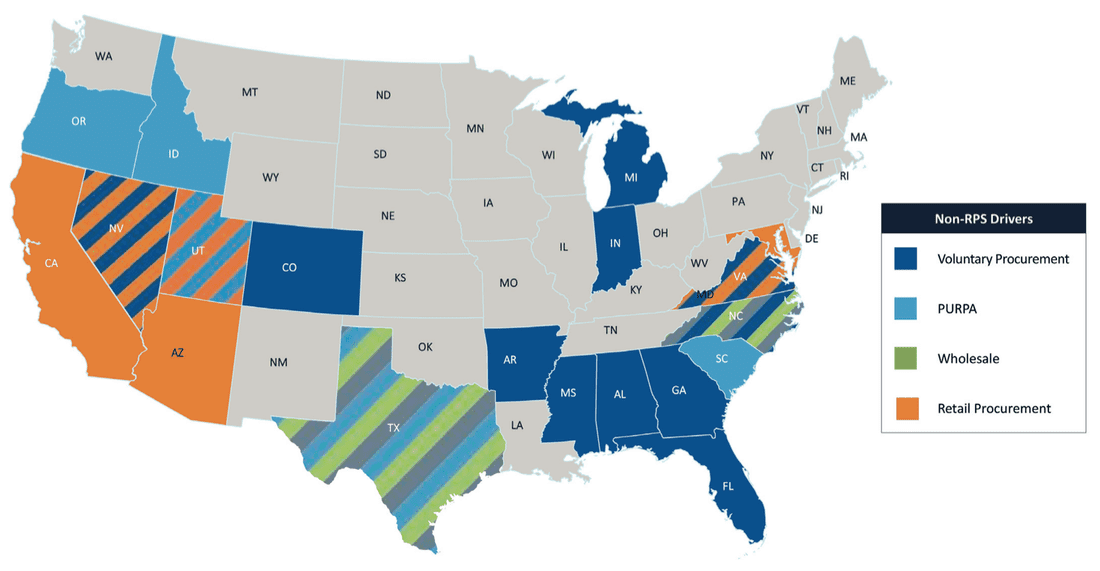

The City of Austin, TX and the State of Minnesota have led the charge on the initial VOS studies, and have proposed different cost structures and calculation methodologies. It would have been easy to anticipate that VOS would have taken off, especially as a substitute for the much-maligned net metering policies, but so far it has not. But if the recent solar policy battles are any indication, the days of the old net metering policies may be numbered. VOS may open the door for a more nuanced treatment of solar in our energy policy. States with > 50 MW Non-RPS Utility PV in Development  (Source: GreenTech Media)

Related data points:

Conventional wisdom says that the solar market is policy-driven, but this is changing in a big way The most vibrant and active solar markets are driven by Renewable Portfolio Standard (RPS) programs with supporting net metering and feed-in-tariff (FIT) programs, or so goes the conventional wisdom. California and Massachusetts exemplify this supposition, as their RPS programs undergird two of the largest utility-scale solar markets in the U.S. But evidence is mounting that the solar market will no longer be driven exclusively by RPS mechanisms. In 2015, 39% of utility-scale solar was procured using non-RPS mechanisms, and this is projected to increase to 52% in 2016. This begs the question - what is driving this marked shift? Falling costs are making solar more competitive with conventional generation The fact that solar has been undergoing rapid cost reductions is a borderline platitude at this point (see here for a good summary of key facts). Estimates for the average installed cost of utility-scale solar in the U.S. was $1.45/watt in 2015, with more reductions projected in the coming years. However, the real interesting question is how these cost reductions are changing the dynamics of competition across energy sources for utilities. Grid parity is considered the holy grail for utility-scale solar, and grid parity (or better) with prevailing natural gas prices has become a reality in many U.S. states (see here for some more detail on grid parity). This change in the market is making it real easy for utilities to make the simple economic argument that signing 20-year PPAs at below $60/MWh is not only the most prudent course of action from a bottom-line perspective, but also the best hedging strategy, which is discussed further below. This has also given rise to a new wave of avoided-cost contracts in states where solar is cheaper than conventional alternatives. This was enabled by PURPA (Public Utility Regulatory Policy Act), a landmark energy law from the 1970s that mandates that utilities purchase electricity from independent power producers (IPPs) if their cost is below the marginal cost of increasing the utility’s generation capacity through conventional means. This type of arrangement greatly reduces the risk of developing solar projects of a certain size, and has fueled the markets in states such as North Carolina. There is another big story behind the rise of non-RPS utility-scale solar related to the role of corporate PPAs, which you can dig into in a previous blog. The hedge against variable (and volatile) natural gas and coal fuel costs is attractive Many utilities are starting to see the writing on the wall in terms of their exposure to variable and volatile fossil fuel prices. Do not believe the hyperbole that oil and gas prices have reached a “new normal” with prices hitting lows not seen for many years (see a good discussion of peak oil here). We are likely amid an anomalous period of low petroleum prices brought on by a confluence of factors - namely, historically high oil prices prior to the 2008 recession which escalated investment in exploration, and cheap financing made available through low interest rates. The current oil and gas low prices are undercutting the ability of firms to invest in exploration, which will eventually erode the current surplus and lead to future deficits and much higher prices than we see today. As discussed in a previous blog, even the most conservative projections of future natural gas prices has them increasing, with many projections substantially above current prices. The future of coal is a more complicated matter, but suffice it to say that any utility which maintains coal as a primary long-term energy procurement strategy will be taking on a great deal of policy and financial risk. When seen from this perspective, any rational observer of the U.S. utility sector would naturally conclude that they need to invest heavily in hedge strategies to protect against the inevitability of volatile and unpredictable fossil fuel prices. As many utilities have gained exposure to and comfort with solar PPAs as a compliance mechanism to meet RPS targets, it started to dawn on them that there could be substantial benefits to using PPAs as a hedging strategy. As a consequence, we are now witnessing a boom of procurement taking place outside of the RPS-driven solar markets, at least partially driven by the desire to increase their portfolio of low-risk electricity generation from solar PPAs with predictable rates for 10-25 years. It seems somehow fitting that utilities are increasingly more willing to exchange their variable-priced fossil fuel capacity for variable-generation solar capacity. Further reading:

C&I solar market starting to attract some attention from investors

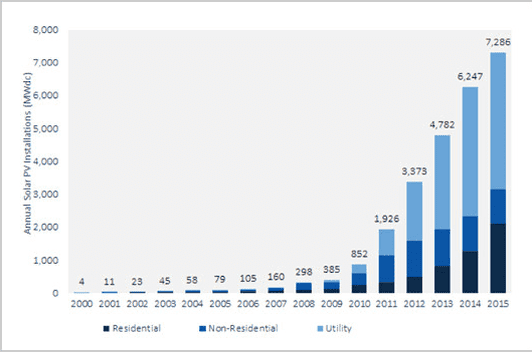

Commercial and industrial (C&I) solar has, to a certain degree, fallen between the cracks in the landscape of solar financing. Utility-scale solar, given its high capital requirements and relatively straightforward risk profile, has been an easy sell for debt providers, tax equity investors, and well-capitalized equity investors. Small-scale rooftop solar has found success in third-party financing and leasing models that have unlocked a wave of deployment, especially in states with favorable net metering policies. Compared to these two markets, C&I has been a more difficult market to serve. The smaller scale of the projects is often unattractive to many investors, and can create a bottleneck when it comes to finding tax equity investors. Moreover, the higher transactions costs and more opaque risk profile compared to utility-scale solar have handicapped this sector in the eyes of many underwriters and investors. The challenges faced by the C&I market are not evidence of any underlying weakness in the value proposition, but rather that different approaches are needed to serve this highly untapped market space. Increasingly, investors are recognizing this need, and entering the C&I market with the intent to reduce transaction costs, standardize the due diligence and underwriting process, and bundle projects to achieve the scale necessary to access more efficient capital markets. There are excellent prospects of higher risk-adjusted returns and comparatively less competition for those successful in mitigating the risks inherent to the C&I market. Lucrative opportunities increasingly concentrated in states with healthy SREC markets As solar deployment has accelerated and installation costs continue their downward trend, it would be reasonable to conclude that there should be no shortage of lucrative solar project investment opportunities. But then, you would be overlooking the countervailing impact of progressively lower and shorter term PPAs, particularly in markets dominated by a small number of incumbent utilities with concentrated negotiating power to determine the terms. PPA rates are now consistently falling below the $60/MWh threshold, sometimes with no escalators, and for periods as short as 10 years. Returns to solar project investors are being squeezed to the point where traditional investors in the space may be starting to look elsewhere to meet their hurdle rates. Solar project investment activity is increasingly focusing on the handful of states with healthy SREC markets. Massachusetts and New Jersey are the most prominent in the mix. Massachusetts SREC I bid prices are trading above $450/MWh and SREC II bid prices are around $270/MWh, though these markets are on hold due to pending legislation. New Jersey SREC bid prices are all hovering around $280/MWh. Washington D.C. and Maryland both have SREC programs with bid prices above $100/MWh, which rounds out the most impactful programs from a price standpoint. These additional revenue streams can help to offset the lower PPA rates, and increase risk-adjusted returns to a level that is attractive to many investors. You may ask - what is driving these SREC bid prices? To which I would respond - the oldest economic story in the book is playing out in these markets The supply of solar (solar project installations) and the demand for solar (driven largely by RPS and solar carve-out policies) govern SREC prices. The extension of the solar ITC is projected to increase the solar pipeline over the next five years, thereby increasing the supply. On the other hand, there is concern about dwindling demand for SRECs, as program caps and other RPS targets are met. Already in Massachusetts, we are seeing developers faced with increased risks due to caps being hit for the SREC II program. When you combine the increasing supply with decreasing demand, you quickly get the picture that SREC prices may not be able to exist at their current levels for many years to come. This eventuality has motivated solar developers and investors to quickly take advantage of the current market conditions in these target markets. The latest U.S. Solar Market Insight Report from GTM Research and the Solar Energy Industries Association reveals that the U.S. installed a record 7.3 GW of PV capacity in 2015, with solar installations surpassing natural gas capacity additions. Overall, solar accounted for 29.5% of all new energy capacity additions in the U.S. in 2015. U.S. Solar PV Installations, 2000-2015  (Source: GTM Research / SEIA U.S. Solar Market Insight Report) Among the different solar sectors in the U.S., residential PV has been the fastest-growing market segment, expanding by at least 50% over the past three years and 66% in 2015. By Q1 2016, the number of U.S. homeowners with rooftop solar is expected to cross the 1 million mark. Indeed, the falling costs of installation paired with rising retail electricity rates make residential solar economics increasingly attractive in a growing number of states. A GTM study released in February found that 20 U.S. states have reached grid parity for residential solar. However, the increase in rooftop solar installations and the accompanying rise of net energy metering policies have revealed several issues underlying high penetrations of solar, among them:

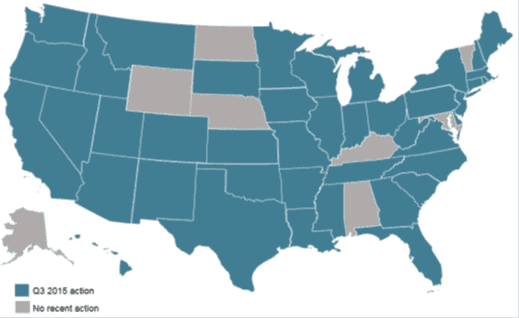

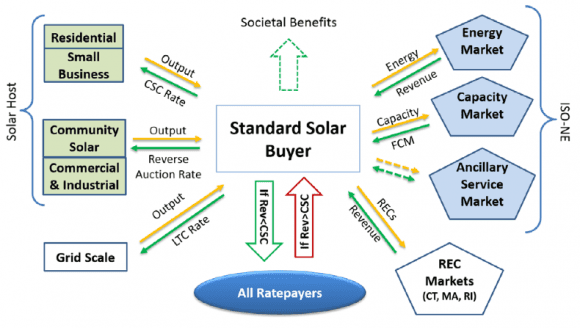

In response to these concerns, and especially the concern among utilities that a decline in sales will generate insufficient revenue to cover the fixed costs of maintaining the grid, some utilities have suggested imposing higher fixed charges on their customers as a method to recoup costs. In 2015 alone, 61 utilities in 30 states requested public utility commissions to increase fixed charges, making it the most frequent policy proposal impacting distributed solar in the last year. 21 utilities in 13 states proposed adding new or increasing existing charges specific to residential solar customers, with the median requested increase at $5 per month. While seemingly a “quick fix” for utilities’ declining revenue concerns, fixed charges do not vary with usage and cannot be avoided with energy net metering credits. Thus, higher fixed charges significantly reduce the financial value of installing solar PV systems. Moreover, fixed charges harm low income and low usage customers and they fail to provide accurate price signals to customers, thereby reducing customer incentives to save on energy use. Research institutes, think tanks, and regulatory agencies have suggested other approaches to address concerns associated with net energy metering in high solar penetration states, among them: time-of-use pricing, smart metering, locational marginal pricing, minimum bills, and revenue decoupling. These suggestions are currently being weighed by legislators and public utility commissions in at least 27 states. Unfortunately, rate review processes are lengthy, and in the meantime the solar industry is paying the price for policy uncertainty. After the Nevada Public Utility Commission’s controversial December 2015 decision to slash net energy metering, many residential solar installation companies halted operations in Nevada, with giants like SolarCity and Sunrun exiting the state. This month, Massachusetts reached its net metering and REC caps, halting operations of solar developers and installers in a state that has more solar jobs than any other state except California. Recent Action on Net Metering, Rate Design, and Solar Ownership Policies  (Source: N.C. Clean Energy Technology Center, 50 States of Solar: A Quarterly Look at America’s Fast-Evolving Distributed Solar Policy Conversation.) One state that has remained below the solar radar is suggesting a new approach for addressing solar rate design concerns. Maine’s new proposal for replacing net energy metering with a market aggregator is making ripples in the solar policy world for its innovative ratepayer-focused approach. The proposal contemplates the creation of a market aggregator that would purchase energy, RECs, capacity value, and ancillary services potential from distributed energy generators at a fixed per-kWh rate guaranteed under a 20-year contract. Centralizing procurement is supposed to reduce transaction costs and create new opportunities for the aggregator to sell the different attributes solar energy provides in applicable markets. Based on a Maine Public Utility Commission March 2015 study that estimated the value of distributed solar at $0.337/kWh, the proposal suggests a starting purchase price from distributed energy generators of $0.20/kWh, higher than the current net energy metering rate ($0.13/kWh) but lower than the $0.337/kWh Maine value of solar estimate. The Public Utility Commission can set a different rate (higher/ lower) based on market conditions and other criteria (there is a lower rate for small commercial projects of 1 to 5 MW). For the wholesale distributed generation market, the aggregator will conduct a quarterly reverse auction for specified levels of installed capacity, with the lowest offer winning a purchase contract from the aggregator who then sells the energy and attributes in the applicable markets. The program is hailed by solar advocates, utilities, and regulators as meeting the needs of all stakeholders involved. Solar customers enjoy rate certainty for a period of twenty years, which is the common term for solar equipment financing. At the same time, all ratepayers are set to enjoy the revenues from the sale of the aggregated energy and attributes in wholesale markets, which are to be allocated equally across the entire rate base. Overview of Market Transactions  (Source: Strategen, A Ratepayer Focused Strategy for Distributed Solar in Maine.)

The bill incorporating the new solar program was endorsed by a bipartisan group of lawmakers, environmental organizations, utilities, solar installers, and consumer advocates. According to the bill’s sponsors, the new program will not only boost Maine’s solar industry but also save $100 million for ratepayers. For those who thought that community solar marks the second revolution in the solar market, Maine’s promising new solar purchase program serves as another example of how aggregation of solar generation and attributes could increase returns for all parties involved. The emerging lesson from these two examples is that with solar energy, economies of scale could be achieved without unnecessary investments in large and expensive infrastructure. Innovative market models and creative policy approaches will determine the next leaders of the solar world. First, states across the country are rapidly reaching grid parity, a long-awaited panacea for the persistent U.S. solar industry. As a quick refresher, grid parity occurs when the cost of generating renewable electricity falls below the cost of purchasing power from electric utilities. Said another way, grid parity makes switching to renewable energy a no-brainer. There are now 20 U.S. states that have reached grid parity as solar installation costs have continued to decline and retail electricity rates have continued to rise. Second, more than 50% of new utility-scale solar in the U.S. in 2016 will be driven by non-RPS obligated development. Although state-mandated renewable portfolio standards have bolstered utility-scale development in past years, the economics of solar now stand on their own enough to support the majority of new utility-scale installations. Let’s dive into what’s driving this sharp increase in mostly voluntary, large-scale development.

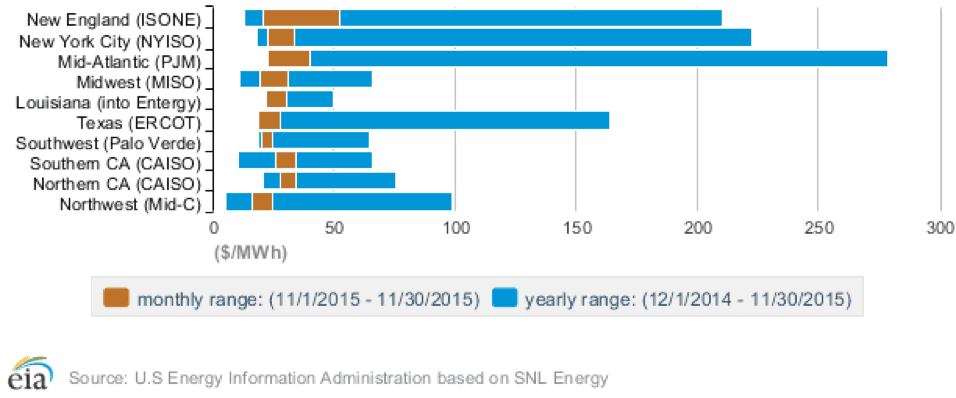

Among the 19 states with more than 50 MW of non-RPS, utility-scale development slated for 2016, some unlikely players in the Southeast appear, including SC, GA, FL, AL, MS, and AR. Although large-scale development is a positive sign within these emerging markets, retail customers rarely have the opportunity to directly participate in the benefits of a diversified fuel mix. The West Coast includes much more intriguing markets, including states like Oregon, which just this week passed a senate bill to incentivize utility scale development between 2 and 10 megawatts. California’s progressive utility companies are further up the learning curve and are now directly engaging retail customers in large-scale solar development, just not always for the customer’s benefit. For example, Marin Clean Energy, a community choice energy program, offers retail customers the option of procuring 50% or 100% of their power demand from utility-owned solar farms at rates that are about 3.5% below current retail rates. On the other hand, PG&E, through their Solar Choice program, offers customers the ability to opt into solar at a premium of 3.58 cents per kWh compared to current retail rates, meaning PG&E is charging their customers more if they choose to power their homes or businesses using solar. Although the Solar Choice program accomplishes similar goals of community solar, including access to solar for renters and homeowners with homes that are unsuitable for on-site PV generation, PG&E is actually using their own customer base as off-takers with PPA pricing that far exceeds competitive pricing for traditional utility-scale development. It makes sense that historically conservative utilities across the country are now embracing large, centralized solar generation, but the hope is that a growing number of consumers will also begin to benefit from the cost-effectiveness of utility-scale PV generation. Corporates and communities ramp up 2016 pipeline The EIA expects 9.5 GW of new solar capacity to come online in the U.S. in 2016. This comes one year after the solar industry added a record breaking 7.3 GW of new solar capacity, marking the first time in U.S. history that solar exceeded natural gas in terms of new capacity coming online. In addition to the notable increases in utility-scale generation, corporate buyers emerged as a major participant in the large-scale generation market. Companies like Apple, General Motors, Google, and Lockheed Martin are ramping up solar generation to power their own facilities, creating a giant marketplace that barely existed just one year earlier. According to the Rocky Mountain Institute, corporate purchases of renewable energy tripled in 2015 with more than 3.4 GW of installed capacity. However, 15 of the 20 announced deals were from first-time corporate buyers, so the jury is out on whether this pace can be sustained in 2016. Much has been written about the growth of the community solar marketplace, and if we had to guess, industry estimates are actually conservative. New community solar programs seem to be announced daily, including a provision within the same Oregon solar bill mentioned earlier. New York is rumored to have pent up demand for community solar developments, and Minnesota’s community solar market is red hot. It was reported this week that BHE Renewables, a subsidiary of Warren Buffet’s Berkshire Hathaway Energy, purchased a 66 MW community solar portfolio comprised of 21 projects across 16 counties in Minnesota. The developer, Geronimo Energy, had previously sold 34 MW of Minnesota-based community solar to BHE Renewables, and seems poised for additional development with BHE Renewables as the take out partner. We will continue to keep tabs on the progress of both community solar and corporate solar purchases throughout this high-growth period. Monthly and Annual Range of Wholesale Electricity Prices  (Source: EIA)

Related data points:

PPAs are getting structured with shorter terms, which actually may end up being a boon for solar project investors Contracted revenue provides the basis of solar project financing. When long-term power purchase agreements (PPAs) came into use for solar projects, they created stable cash flows that risk averse investors could trust. The simplest solar projects being built today still rely on PPAs that typically range from 15 to 20 years. This PPA model is being adapted to current market conditions, with some potentially unintended consequences. Recently, evidence is mounting in regulated markets that utilities are signing PPAs for shorter durations. For example, Duke Energy, serving more customers than any utility in the U.S., is now consistently on record as offering progressively lower PPA rates over shorter timeframes. For a solar project developer, this can be seen as problematic, as you now have a shorter period of secure cash flows generated by your project, which could undermine the basis for a project’s valuation. But this all hinges on what you believe about the future of wholesale electricity prices. Once the term of a PPA is complete for generators that are “in front of the meter,” an option is often available to then switch to selling the electricity generated on the wholesale markets. Given the downward trends in PPA rates, which are now consistently falling below the $60/MWh threshold, the wholesale market may end up yielding higher returns if wholesale rates increase according to industry projections. Thus, a solar project with a shorter PPA may end up yielding higher returns than one with a longer PPA, albeit with some additional merchant risk associated with participating in wholesale markets. Quantifying merchant risk can be a complex task, and is not to be disregarded, but neither does it need to render a project financially infeasible. Are utilities preparing for a future with higher natural gas prices? From the perspective of the utility negotiating the PPA, there are some interesting implications for why a utility like Duke Energy would want to short-term negotiate PPAs. Fundamentally, they must believe that electricity generation will not get substantially more expensive in the future. This is likely a product of the mantra that natural gas prices will remain low for the foreseeable future, an assertion that does not seem to be supported by an objective forecast of the price of natural gas. If natural gas prices rebound in the future, as they inevitably will at some point, wouldn’t it be prudent to have a portfolio of long-term solar PPAs to keep electricity retail rates from spiking? This possibility seems largely absent from the current thinking around PPAs, even as electricity generation from solar has become cheaper than natural gas. n addition, there must be the belief that solar PPAs and other equivalent electricity sources will become progressively cheaper in the future. If trends from the past decade are any indication, this is a safe bet. Yes, solar costs are projected to continue rampant decreases in costs over both the near- and long-term future. So, the solar PPA that Duke signs in 2018 will likely be at a lower rate than the one signed in 2016. But, if natural gas prices do not support continued expansion of natural gas power plants, can solar project pipelines be able to make up the difference? Perhaps, but it is no sure bet. Thus, the question is one of scale and hedge risk against a future in which today’s anomalously low natural gas prices do not continue in perpetuity. Evolution of solar project investing is driving out investors seeking high yield As solar project finance emerged from its inception as a niche market to a broadly appealing investment class, the search for risk-adjusted returns has naturally become more of a challenge. Early investors in solar project finance were attracted by the double-digit return potential based on long-term contracted cash flows. As the perception of high technology risk receded into the past, the overall risk profile of solar projects started to look more like bonds and other fixed income assets. Stable and predictable cash flows backed by a tangible asset coupled with very low long-term operating costs and free fuel made for an enticing proposition. Looking over a cash flow statement, solar projects started to look like many other revenue generating infrastructure assets - bridges, toll booths, pipelines, etc. Large infrastructure funds and other investors familiar with these types of revenue generating assets entered the market and started to compete with the incumbents, specialty investment funds. But now we are seeing a new type of entrant into the market. Now, the cat is out of the bag, so to speak. Solar project investing is no longer a niche activity, and there is a swell of interest in acquiring solar projects for their predictable cash flows. But as the solar industry has matured, there is less value being left on the table. Or rather, solar investors are no longer able to easily generate unlevered returns in the double digits, at least not without the help of incentive programs such as SRECs to generate revenue outside of the PPA structure. Whereas private equity and investment funds with higher costs of capital have been big players in financing solar projects to date, we may be seeing a shift to banks, insurance companies, and institutional investors with large appetites for low risk, and more modest returns over long time horizons. As large solar portfolios start to enter the market seeking investors, increasingly they may be turning to the funds with the greatest tolerance for lower returns. Their success in this market will depend upon how quickly that can become savvy on the intricacies of solar project finance. Further reading:

Related data points:

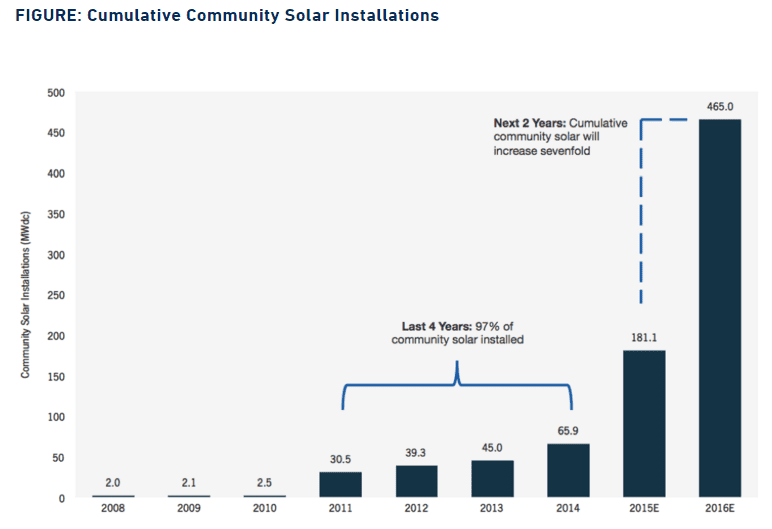

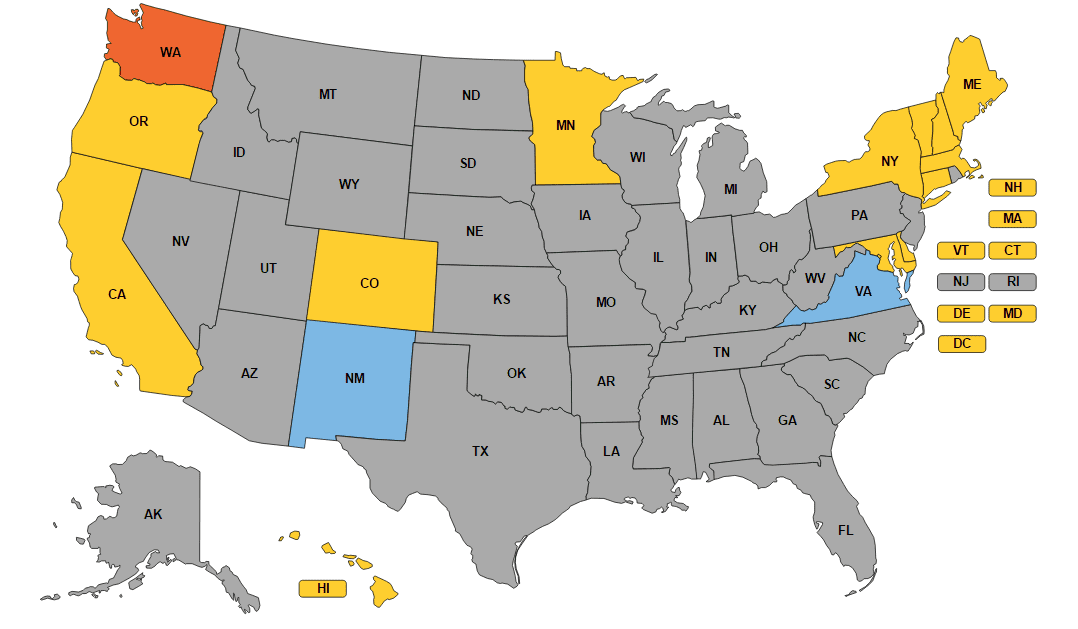

In June 2015, six months before Congress extended the solar ITC beyond 2017, GTM Research predicted that by 2020 community solar will be a half-gigawatt annual market. With the new ITC extension, the recent IRS private letter ruling on community solar, and EPA’s Clean Power Plan gradual march forward, more and more actors in the solar industry are starting to realize the prospects created by community solar programs across the country. Indeed, community solar could well mark the second revolution in the solar market. For those who have missed the rooftop solar revolution, community solar could be the second chance to get on the solar train.  (Source: GTM Research) Why community solar and why now? A relatively new concept in renewable energy, community solar allows customers who might find solar panels to expensive or impractical to install on their property to enjoy the benefits that come with owning solar panels without the need to install a solar facility on their property. The primary purpose of community solar initiatives is to reduce member costs and risks through a joint investments scheme in a community solar facility to be located in a suitable location in proximity to the contracting community. By aggregating customer-generators, project participants could benefit from the electricity generated by the community solar farm, which costs less than the price they would ordinarily pay to their utility. With somewhere between half to 85% of electric consumers in the U.S. unable to install solar panels because they don't own their home, don't get enough sun, or don't have the required financial resources, community solar represents a huge, mostly untapped market waiting to be grabbed. Unfortunately, as with every new market, uncertainties are abound. It is therefore not a coincidence that the states with the most community solar projects are generally the states that have addressed investor concerns through strong enabling legislation. These states include Colorado, Minnesota, Massachusetts, and Vermont. Other states are rapidly catching up, and currently 15 states and the District of Columbia are contemplating or have already introduced community solar programs through legislation. Unfortunately, state programs differ widely, and some programs do not offer the same level of investor certainty as others.  (Source: Shared renewables (in blue: pending legislation))

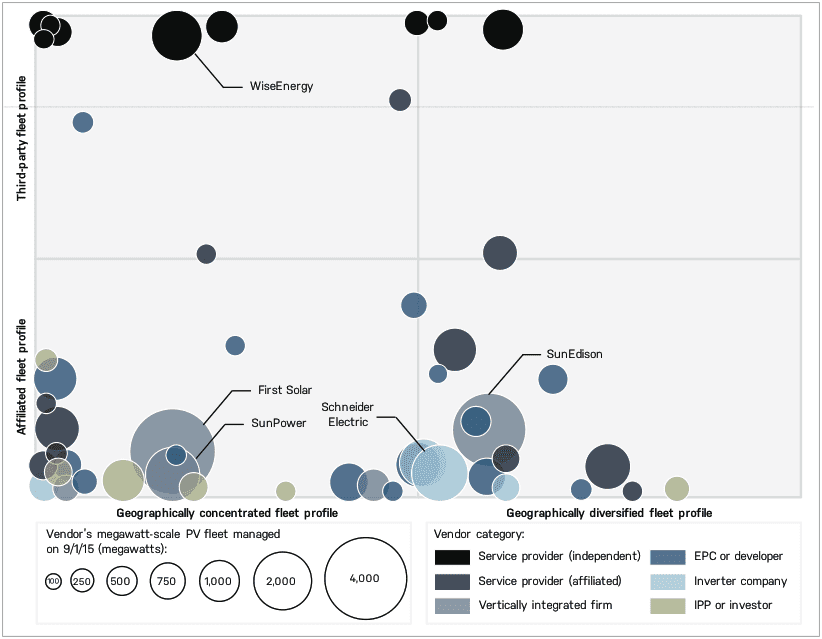

Addressing investors’ concerns In comparison to traditional distributed energy projects, community solar initiatives pose a heightened credit risk. Multiple members with varying degrees of creditworthiness make investors uneasy, to say the least. Moreover, restrictions on exit make community solar unattractive to potential members who have only a small stake in the project and are therefore wary of signing contracts that impose penalties on members who leave the community; while the potential for high member turnover scares investors away. Add to this the usual concern that multiple parties to a transaction mean higher transaction costs, and the reason why investments in community solar are hard to come by becomes clear. However, an in-depth assessment of community solar schemes across the U.S. reveals that several states have done a remarkable job addressing these concerns, making investments in community solar in their jurisdiction not only relatively safe but also quite attractive. To ease operations and reduce transaction costs, Public Utility Commissions in New York, Maryland, Minnesota, and Colorado have introduced an intermediary special purpose entity (SPE) responsible for aggregating membership interests and managing the relationship with the local utility. Thus, instead of contracting directly with the residents in the community, the utility enters into an agreement with the SPE which serves as the project’s manager. The SPE aggregates members and collects payments; provides the utility with member information; and distributes excess credits to members (or instructs the utility how to distribute excess credits). To allow flexibility and innovation, the states left it to sponsors and potential members to determine the terms of their contractual relationships, including conditions for removal and replacement of members. The SPE structure makes member replacement fairly easy. Since utilities are engaged with the SPEs and not individual members, they are agnostic to member exits and replacements. When it comes to removing, replacing, or adding members, the SPE’s sole responsibility is to notify the utility of the change in a timely manner. While not as flexible, other states took a fairly close approach to reducing risk associated with multiple members. New Hampshire, Massachusetts, and Delaware require that the community designates a “host” member with an ownership interest in the solar facility to contract with the utility, administer group relationships, instruct the utility on credits allocation, and control membership structure. Vermont’s community solar scheme is not run by a utility or third-party SPE. Instead, members are free to organize themselves, stipulating their own process for allocating the generation credits among their accounts. The program’s flexibility is hailed as attracting investments in community solar, but projects are only attractive when the terms of subscriber contracts allow for immediate termination of defaulting members. In other states, programs are either overly restrictive (Maine, Washington), are still in the works, or undergoing revisions (Connecticut, Virginia, Oregon, DC, Hawaii, California). What’s next? Through our work with interested investors and qualifying developers, we have come to appreciate the market potential for community solar in the seven “leading” states (New York, Maryland, Minnesota, Colorado, New Hampshire , Massachusetts, Delaware, and Vermont). However, strong opportunities do not mean zero risks. Although the regulatory environment in these states makes it easier for community solar administrators to mitigate risks associated with multiple members, in practice finding and contracting with an alternative member is contingent on the characteristics and contractual terms of the specific project. A profitable project with a simple member replacement mechanism should not experience difficulties in recruiting new members to replace those who defaulted. To ensure that a project is investment-worthy, developers and administrators are therefore advised to include terms in solar community agreements that allow for the immediate termination of defaulting members’ subscription even if such language might mean an initially harder-to-market project. In addition, developers should restrict member subscription, reserving a pool of unsubscribed interested and potential members in the community for future member replacements. From an investor perspective, investors should carefully examine developers’ subscription and management contracts, verifying that administrators and hosts have adequate measures for addressing the risks associated with multiple members. Global Megawatt-Scale PV O&M and Asset Management Competitive Landscape  (Source: Greentech Media)

Related data points:

U.S. solar investment and deployment will continue the charge forward, but not everywhere Clean energy investment reached a record $329B globally in 2015, $56B of which took place in the U.S. The international and national policy winds are all pushing in favor of further accelerating clean energy investment in the coming years. However, there is more complexity at the level of local politics with entrenched utilities and PUCs. Do not underestimate the ripple effect of the conflict on solar policy in Nevada. A class action lawsuit was recently filed in protest of the draconian sanctions imposed on the solar industry and homeowners who had invested in solar systems under a now defunct incentive structure. Add the Nevada dispute to the growing list of local conflicts in Arizona, Hawaii, Colorado, and Minnesota, and a clearer picture of just how embattled the solar industry has become in many places around the country becomes clear. It is curious that so many conflicts are emerging despite the fact that the vast majority of Americans support solar across the political spectrum. An excellent analysis of these “niche-regime” conflicts was recently published by Dr. David J. Hess of Vanderbilt University, which concluded that we can expect continued resistance from incumbent (“regime”) utilities and PUCs that perceive the solar industry (“niche”) to be a threat to their way of doing business, especially in geographies where the solar industry is associated with a political party that is not well represented in local governing bodies. As a result, we may start seeing a more fragmented landscape of solar investment and deployment activity in accordance with the level of local policy support or resistance. Solar investors and developers, who tend to be very sensitive to the policy drivers that underpin their business strategies, will need to remain ever-vigilant of local and state policy, even in the context of the extended solar ITC. That being said, agile solar developers that can quickly adapt to the shifting solar policy landscape, especially in emerging markets, will have a leg up on the competition. Solar development will experience a downtick in 2016, but it will be good in the long-run According to SEIA, the ITC extension will lead to more than 72 GW of solar PV installations from 2016 through 2020, an increase of over 25 GW (or 54%) over baseline expectations without the extension. However, with the pull effect of the solar ITC cliff at the end of 2016 diminished, there may be less solar installation in 2016 than was previously projected. In fact, growth in the solar industry may slow in 2016 to an estimated 8% according to S&P in 2016, compared to the over 20% growth seen in 2015. While this may have negative ramifications for the near-term cash flows generated by some solar companies, and by extension the valuation of some publicly traded solar companies, it will be beneficial for project investors. The smoothing of solar policy support and hence development over the next 5 years will allow for more prudent investment that can generate better long-term returns. There will be more room for patient capital, and investors willing to do the research and diligence to identify good investments for their risk tolerance. The race to the end the solar industry’s dependence on the ITC has gotten moved into the 2020s, a point at which solar will hopefully no longer needs tax equity in order to make sense in most geographies around the U.S. While solar policy and finance dominate the headlines, solar technology will continue up the learning curve Since the implementation of the ITC in 2006, the cost to install solar has dropped by more than 73%. Across the U.S., the average total project cost for solar is hovering around $2.42/watt for non-residential and utility-scale installations. That is what is often meant by the technology learning curve: decreasing system costs. With all of the focus on how rapidly solar has gotten cheaper, some focus has been taken away from how much better the technology is getting. Just over the last 5 years, solar modules have experienced a massive proliferation of technologies, which are pushing the bounds of efficiency and performance. A compelling graphic of the state of solar module technology produced by NREL suggests that previously unheard efficiencies of 30% and higher are now feasible in laboratory settings, and some of these are ripe for commercialization. The crux of the matter, of course, is how cost efficient these cutting edge solar module technologies can be. If commercial solar module technologies can achieve a bump in efficiencies at a price that the market can withstand, we could see some dramatic improvements in solar project finance. The US DOE’s SunShot program is trying to accelerate the deployment of the new generation of commercial solar module technology with their recent announcement of a $22.7M investment across 23 promising projects. Even if we take the cutting edge technologies off the table, the most prevalent types of solar panels being deployed, crystalline silicon and thin-film panels, have become much more efficient in recent years. So, amid all of the hoopla about solar deployment, let’s not lose sight of the horizon for solar module technologies. Further reading:

|

sign up for ironoak's NewsletterSent about twice per month, these 3-minute digests include bullets on:

Renewable energy | Cleantech & mobility | Finance & entrepreneurship | Attempts at humor (what?) author

Photo by Patrick Fore on Unsplash

|

{kind=link}

{kind=link}

© 2009-2022 IronOak Energy Capital, LLC | (888) 249-3013