|

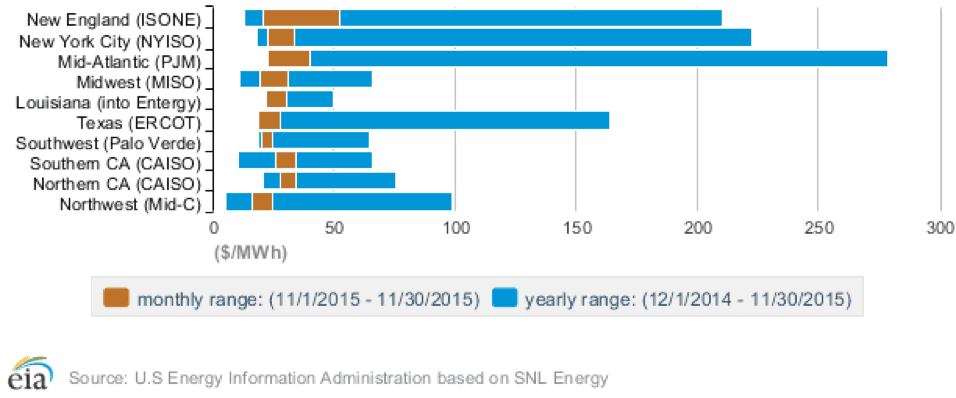

Monthly and Annual Range of Wholesale Electricity Prices  (Source: EIA)

Related data points:

PPAs are getting structured with shorter terms, which actually may end up being a boon for solar project investors Contracted revenue provides the basis of solar project financing. When long-term power purchase agreements (PPAs) came into use for solar projects, they created stable cash flows that risk averse investors could trust. The simplest solar projects being built today still rely on PPAs that typically range from 15 to 20 years. This PPA model is being adapted to current market conditions, with some potentially unintended consequences. Recently, evidence is mounting in regulated markets that utilities are signing PPAs for shorter durations. For example, Duke Energy, serving more customers than any utility in the U.S., is now consistently on record as offering progressively lower PPA rates over shorter timeframes. For a solar project developer, this can be seen as problematic, as you now have a shorter period of secure cash flows generated by your project, which could undermine the basis for a project’s valuation. But this all hinges on what you believe about the future of wholesale electricity prices. Once the term of a PPA is complete for generators that are “in front of the meter,” an option is often available to then switch to selling the electricity generated on the wholesale markets. Given the downward trends in PPA rates, which are now consistently falling below the $60/MWh threshold, the wholesale market may end up yielding higher returns if wholesale rates increase according to industry projections. Thus, a solar project with a shorter PPA may end up yielding higher returns than one with a longer PPA, albeit with some additional merchant risk associated with participating in wholesale markets. Quantifying merchant risk can be a complex task, and is not to be disregarded, but neither does it need to render a project financially infeasible. Are utilities preparing for a future with higher natural gas prices? From the perspective of the utility negotiating the PPA, there are some interesting implications for why a utility like Duke Energy would want to short-term negotiate PPAs. Fundamentally, they must believe that electricity generation will not get substantially more expensive in the future. This is likely a product of the mantra that natural gas prices will remain low for the foreseeable future, an assertion that does not seem to be supported by an objective forecast of the price of natural gas. If natural gas prices rebound in the future, as they inevitably will at some point, wouldn’t it be prudent to have a portfolio of long-term solar PPAs to keep electricity retail rates from spiking? This possibility seems largely absent from the current thinking around PPAs, even as electricity generation from solar has become cheaper than natural gas. n addition, there must be the belief that solar PPAs and other equivalent electricity sources will become progressively cheaper in the future. If trends from the past decade are any indication, this is a safe bet. Yes, solar costs are projected to continue rampant decreases in costs over both the near- and long-term future. So, the solar PPA that Duke signs in 2018 will likely be at a lower rate than the one signed in 2016. But, if natural gas prices do not support continued expansion of natural gas power plants, can solar project pipelines be able to make up the difference? Perhaps, but it is no sure bet. Thus, the question is one of scale and hedge risk against a future in which today’s anomalously low natural gas prices do not continue in perpetuity. Evolution of solar project investing is driving out investors seeking high yield As solar project finance emerged from its inception as a niche market to a broadly appealing investment class, the search for risk-adjusted returns has naturally become more of a challenge. Early investors in solar project finance were attracted by the double-digit return potential based on long-term contracted cash flows. As the perception of high technology risk receded into the past, the overall risk profile of solar projects started to look more like bonds and other fixed income assets. Stable and predictable cash flows backed by a tangible asset coupled with very low long-term operating costs and free fuel made for an enticing proposition. Looking over a cash flow statement, solar projects started to look like many other revenue generating infrastructure assets - bridges, toll booths, pipelines, etc. Large infrastructure funds and other investors familiar with these types of revenue generating assets entered the market and started to compete with the incumbents, specialty investment funds. But now we are seeing a new type of entrant into the market. Now, the cat is out of the bag, so to speak. Solar project investing is no longer a niche activity, and there is a swell of interest in acquiring solar projects for their predictable cash flows. But as the solar industry has matured, there is less value being left on the table. Or rather, solar investors are no longer able to easily generate unlevered returns in the double digits, at least not without the help of incentive programs such as SRECs to generate revenue outside of the PPA structure. Whereas private equity and investment funds with higher costs of capital have been big players in financing solar projects to date, we may be seeing a shift to banks, insurance companies, and institutional investors with large appetites for low risk, and more modest returns over long time horizons. As large solar portfolios start to enter the market seeking investors, increasingly they may be turning to the funds with the greatest tolerance for lower returns. Their success in this market will depend upon how quickly that can become savvy on the intricacies of solar project finance. Further reading:

Comments are closed.

|

sign up for ironoak's NewsletterSent about twice per month, these 3-minute digests include bullets on:

Renewable energy | Cleantech & mobility | Finance & entrepreneurship | Attempts at humor (what?) author

Photo by Patrick Fore on Unsplash

|

© 2009-2022 IronOak Energy Capital, LLC | (888) 249-3013