Last year, IronOak Energy’s investment advisory practice had some challenges competing against yieldcos on behalf of our solar investor partners.

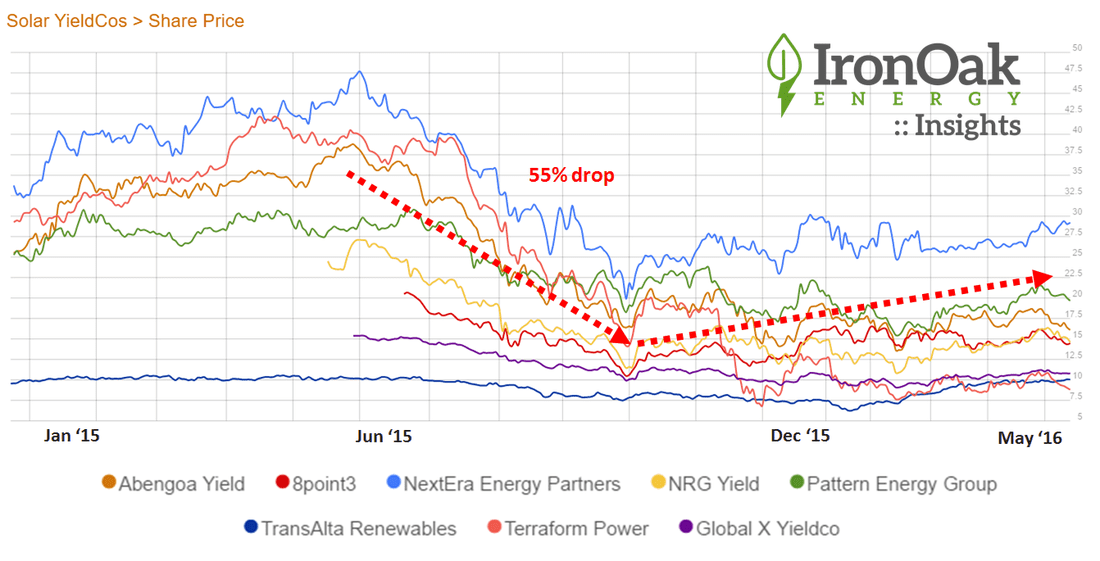

We kept abreast of the yieldco’s up/down trends at IronOak’s stock chart. They were offering what some called “a stupid low” cost of capital. That was sometimes said as a judgment on the the yieldco business model. Other times it was a said with a slight jealousy: “I wish our yields were still attractive at those levels so we could win more deals with predictable long-term cash flows.” Developers licked their lips. Those low-yield requirements made their discounted cash flow models really sing. As we all know, in late summer last year, both developers and yieldcos bought their share of Kleenex boxes. But this was great news for private equity and helped improve their returns. Many claimed the model was broken. We thought that was shortsighted. Sometimes innovators hit a speedbump, but then they hit the accelerator again. Now several yieldcos are getting ready to go to public markets. It’s not time for them to be big-time project buyers at attractive costs, but that time will come. For now, private equity still rules. Comments are closed.

|

sign up for ironoak's NewsletterSent about twice per month, these 3-minute digests include bullets on:

Renewable energy | Cleantech & mobility | Finance & entrepreneurship | Attempts at humor (what?) author

Photo by Patrick Fore on Unsplash

|

© 2009-2022 IronOak Energy Capital, LLC | (888) 249-3013