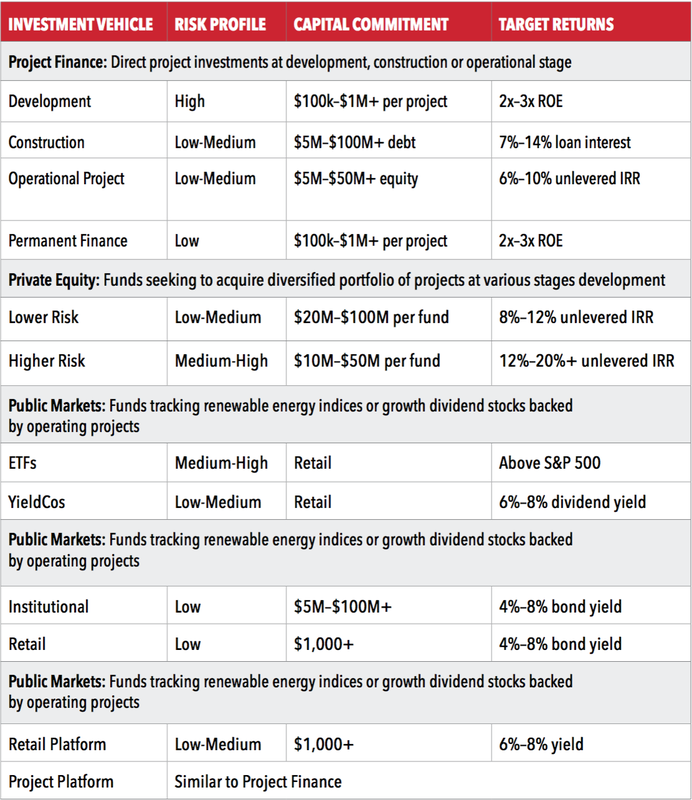

Originally published in Real Assets Adviser, a Publication of IREI. A revised version was published on CaroFin. Renewable energy became mainstream in 2016. The perceptions that renewable energy is easily outcompeted by conventional fossil fuels, burdened by technological risk and uncertainty, or simply an environmental luxury for the wealthy have been thoroughly debunked. Do not let these myths cloud your judgment, as renewable energy is now a considerable presence within the energy market. This is not a hypothetical or some potential future, but the ground truth reality in today’s market, which many investors and industry experts project will remain the case for the foreseeable future. The following article will center around investing in renewable electrical power generation. There are other forms of renewable energy that do not pertain to electricity, such as biofuels, or that are complementary grid edge technologies, such as energy storage. We will also leave aside traditional low-carbon generation sources such as large-scale hydroelectric and nuclear plants. In 2016, more than 50 percent of new installed capacity came from renewable electricity for the second year in a row. This phenomenon was largely driven by wind and solar, but also included some less prevalent generation sources such as biomass and geothermal. Non-hydro renewable energy sources now comprise nearly 9 percent of total U.S. electrical generation, according to the U.S. Energy Information Agency. And the lion’s share of that renewable generation capacity has been built over the past six years. This is not an anomaly, but rather appears to be the start of a period of sustained growth. Wind and solar are projected to account for 64 percent of the estimated $11.4 trillion invested in energy globally through 2040, according to Bloomberg New Energy Finance. The key drivers underpinning the remarkable emergence of renewable energy are: (1) dramatic cost decreases in solar and wind to the point where they are often the lowest cost of new generation available to the grid, (2) structural decline of coal and nuclear in large part due to low-cost natural gas, and (3) policy incentives and broad public support for renewable energy. Renewable energy is not a passing fad or a trendy alternative to conventional power sources; it has become the predominant form of energy development and investment in the United States and globally. Before considering available investment vehicles, some current context would be useful. In 2016, renewable energy investment dropped 18 percent to below $288 billion. However, much of this drop can be attributed to dropping technology costs, as total renewable power capacity increased by more than 9 percent. The costs for solar panels and wind turbines have fallen by 80 percent and 35 percent, respectively, since 2009, according to the International Renewable Energy Agency. Of this total, over 70 percent was in direct project investments, as opposed to corporate investments or M&A, notes Bloomberg New Energy Finance. While it stands to reason that a primary way in which to invest in renewables is through direct project investments, there are a range of other vehicles to consider based on an investor’s level of sophistication, risk tolerance, liquidity preference and investment horizon. The discussion below should not be considered a direct endorsement of any of the strategies or investment vehicles that are identified. Nor should this be considered a comprehensive review; there are a wide array of alternatives within each broad investment theme that should be considered before making an investment. Specific investment strategies should be developed in accordance with each investor’s investment goals and with the assistance of a professional investment adviser.  The remainder of the article can be downloaded here.

0 Comments

By: Dr. Chris Wedding, Managing Partner OK, so you’re now ready to take your business to the next level by growing faster with outside investors. And you’ve already had the “come to Jesus” realization that giving up a percentage of equity and profits just means that you get a smaller piece of a bigger pie pumpkin, instead of owning a larger piece of a smaller pie (or one that’s already been destroyed by mold and cockroaches.) So, are you ready to hit the road, rack up those frequent flyer miles, pitch to 50+ investors, pre-order the champagne bottles, and get ready to play ping pong in the office between customer meetings? Maybe. But let’s agree that there is always room for improvement, and that no one is ever really ready for anything. (Except maybe Michael Phelps.) Here are 11 items to consider when you get ready to raise investment capital. 1. Your Vision Are your 5-year plans for the company both ambitious and believable? If you lack ambition (e.g., 3% growth per year), then you might elicit yawns from investors. If your projections are not believable (e.g., zero to 40% market share in 3 years), then you might instead cause laughter. (We’re big fans of humor, but not this kind.) 2. Competitors Do you have competitors? Please do not say, “No.” That’s a surefire way to have your follow up emails and calls ignored. Competition is a sign of market validation, that others believe your idea is a good one. Now the important part: Why are you better? Have you created a table showing 3-6 competitors (column headers) compared quantitatively (e.g., scale of 1 to 4) across 5-10 attributes (rows of the table)? And once you’ve done that, and done so honestly, will your competitive advantage be obvious to investors? 3. Runway How much capital do you have in the bank to cover both operating needs (i.e., to continue advancing the ball on the proverbial court) and fundraising expenses (e.g., travel, marketing costs) over the next 6-12 months? Or how much near term revenue do you expect to realize with a high degree of certainty? If it’s not enough to cover both buckets of expenses, then you may end up out of breath, sweating and exhausted, before reaching the white tape at the finish line. 4. Prepared Materials - Teaser, Pitch Deck, Financial Model Based on our experience, I am confident that you are confident that your financial model, pitch deck, teaser, and related fundraising materials are 90% ready to go. However, the devil is in the details. (And we don’t want any devils.) Moreover, there is power in many minds and many eyes taking an outsider’s perspective on your company or project opportunities and challenges. It is common to spend 4-8 weeks conducting internal due diligence and recreating or refining these materials. 5. Your Brand Brand building may sound like an afterthought, or a consideration only for Fortune 500 companies. However, research suggests that many customers’ buying decisions are largely made before we ever talk to them. Their unconscious analysis is based on word of mouth and online research. Here are questions for which you need to have the right answers:

6. Your Team Does your team have the relevant experience and credentials to convince investors that you all can “get *$#! done”? This is about breadth and depth. How are they compensated - salary, commission, equity? How motivated are they to see the company succeed? And how about an Advisory Board? Having one helps build credibility and support customer acquisition and/or deal flow. Nobody knows everything, so stand on the shoulders of giants and tell the world how great those shoulders are. 7. How much is enough? It’s easy to err on the side of raising more money vs. less. But the flip side, of course, is that larger amounts of investor capital may mean a greater burden (e.g., collateral at risk, size of financial returns required) and lack of control for you (e.g., equity ownership). However, the opposite is also true: If you raise too little capital, then you either do not make it to the next important milestone where additional value is created, and/or you are stuck in capital raising mode too frequently, to the detriment of actually running your business. Finally, the amount of capital you seek to raise is a large determinant of the type of investor that will find your venture interesting. 8. Strategic or Financial Investor As a refresher, financial investors -- e.g., banks, VC, project financiers -- place capital primarily to generate financial returns directly from the entity into which they invest. On the other hand, strategic investors -- e.g., corporate investor -- may be investing to generate returns from your company as well as from synergies that are created through overlap among your expertise and theirs (e.g., different product lines, divisions, geographies, customer base). They tend to be slower to invest, but can sometimes offer preferred investment terms, consider higher valuations for your company (i.e., you get to eat more of that pumpkin pie), and/or create lucrative distribution channels. 9. Use of funds How will you invest the capital? Why do you plan to allocate dollars that way (versus other scenarios)? Be ready to explain the logic and provide details. Expect to be questioned as if you were sitting in a dark room under a bright lamp in an old industrial warehouse. (I exaggerate slightly.) 10. Risks No investment is without risk, unless you want to get rich on US Treasury bonds. (Good luck.) And it’s never fun to be blindsided by critics. So, please, please, please do not ignore a thorough discussion of risk factors when talking to investors. However, don’t forget to also provide a point-by-point response for how you seek to minimize those risks. Below are examples of risk factors to address:

11. Unit costs Detailed financial models with multiple scenarios and various Excel tabs are not the quickest documents to digest. Similarly, 5-year financial projections are helpful but only show aggregated analysis. What investors really need to understand in the initial conversation is this: A customer-, site-, unit-level assessment of costs and benefits at a high level (e.g., one slide). From this, they can assess the strength of the business case and move on to hear the rest of your pitch. 12. How thick is your skin? Our job is to ask tough questions, and to play the devil’s advocate. We are on your side, but based on our line of questioning, it may seem like our goal is bury your business plan and financial model in red ink. Au contraire. Our constructive criticism prepares you to handle the tougher questions when they come from investors. We’re like benevolent drill sergeants who guide you through boot camp so that you’re prepared for your best showing when trying to earn investors’ confidence. To learn more about the capital raising process, here are three related blogs we’ve written on the topic: |

sign up for ironoak's NewsletterSent about twice per month, these 3-minute digests include bullets on:

Renewable energy | Cleantech & mobility | Finance & entrepreneurship | Attempts at humor (what?) author

Photo by Patrick Fore on Unsplash

|

© 2009-2022 IronOak Energy Capital, LLC | (888) 249-3013