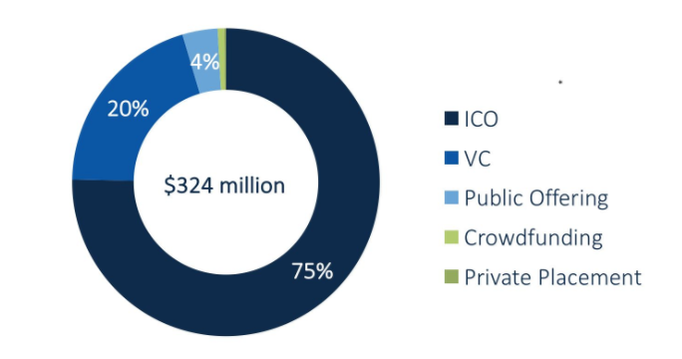

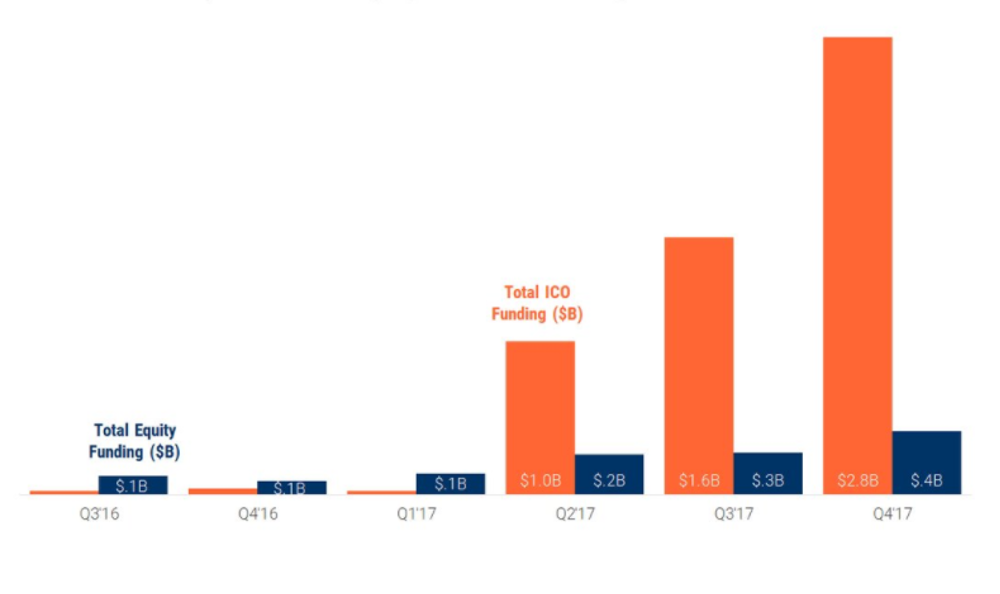

By: Dr. Chris Wedding, Managing Partner In the last quarter, investors poured more than $324M into blockchain for energy companies. Can you believe that? Well, you shouldn’t. But which part is most unbelievable? While $324M seems shocking, it’s all about context. That amount has indeed been raised, but it’s taken 12 months to do so, according to GTM Research. What’s more shocking is that over 75% of this capital has been raised via Initial Coin Offerings, or ICOs. When thinking about this emerging market, it’s kind of like being back in high school: Some investors have FOMO (Fear of Missing Out). But others think they’re too cool to hang out with the kid who just became popular after years of dork-dom. But what should you, oh wise capital providers and ye capital-hungry blockchain entrepreneurs who worship the clean energy gods of purity, know about blockchain-focused energy opportunities? Here are our top 4, out of our longer list of 75. (I exaggerate slightly.) 1. There are 120+ blockchain energy companies. But most are relative newbs. Yep, that’s a term from my kiddos. I can’t wait to finish this blog so I can go tell them I used their word correctly. But do I use the word “newbs” to be mean? Heavens, no. I’m a good Catholic-Buddhist, after all. (Oh, they exist.) What I’m referring to is the age or maturity of most companies in this sector. Research from Solarplaza suggests that most ventures were formed in 2016 or 2017, and investors at the GTM Blockchain Forum note that most founders have little to no operational business expertise. That does not mean that these young ventures lack merit. But it does make the hill to success tougher to climb. (Think steep slopes covered in poison ivy and man-sized Venus flytraps.) As Greentech Media’s Chairman observed [paraphrase]: “We see many white papers for ICOs sponsored by blockchain in energy startups. Some are are interesting. But some are sketchy.” Another panelist at a recent blockchain energy conference noted: "We're currently working with Atari, but we need to be using Playstation 4 to make most [blockchain for energy use cases] work at scale.” An investor panelist put it another way [paraphrase]: “Blockchain is today where the Kardashians were in 2008. When their name is on something, it can print money. But then smart people ask ‘Why? What businesses do they really have? Maybe a clothing line, a home video business (get it?), and a few others?’ But then you realize there is a genius marketing mastermind behind it all. The hype is, in fact, part of the cause for success.” Lastly, all hail innovation. Seriously. This is how it works: First, divergence. Second, convergence. However, we’re very far from the latter. 2. There are a bazillion use cases. And the energy world is 6-trillion-dollars big. Just in case you thought that 120 companies in the same emerging sector was a lot, think again. The Energy Web Foundation, co-led by our friends at the Rocky Mountain Institute, see over 200 potential uses cases for blockchain in energy. Even if only half of those scenarios prove to be real, that is still many, many niche markets ripe for multiple companies to do well in many geographies. Moreover, the energy industry is not a tiny pearl hiding in a small oyster. It’s more like an ocean full of 100-foot long blue whales, as plentiful as squirrels on a college campus. But seriously...no wine glass in hand...The energy market is one of the biggest industries on the planet, and it’s full of intermediaries that control the flow of electricity and money. This creates a huge playground for diverse and interoperable blockchains, distributed and trusted ecosystems of counterparties, and automated and smart contracting abilities.    3. ICOs are crushing equity investors. But that can (should?) not continue. In the broader universe of early-stage blockchain companies, ICOs are killing venture capital. I mean, like the Incredible Hulk vs. me in a boxing ring, or some such awful mismatch. However, the U.S. Securities and Exchange Commission is taking a pretty hard look at ICOs — in the past, present, and future. And let’s just say that their eyebrows are raised, you know, where one is raised higher than the other. While many ICOs have tried to avoid SEC oversight, when it walks like a duck and quacks like a duck, then...It’s a security. (If you don’t know what I mean, take a look at their guidance here.) All is not lost for conventional equity investors. Venture capital and corporate strategic investors bring value that can be far greater than capital alone. (The latter is the extent of the contribution from ICOs.) The other benefits of working with institutional equity investors include rich networks that can lead to partners and customers, insights on corporate governance based on lessons learned from dozens of past ventures, and deep sector expertise to allow for threat and opportunity recognition beyond what the core team might focus on while their heads are down building a company.  Capital Raised for Blockchain Companies: Q3 2016 to Q4 1017 Equity (blue) vs. ICOs (orange) Source: CBInsights, Tokendata  4. Blockchain is not just for nerds. It’s for the C-suite.

Some famous venture capitalists have said that they look for the next big investment opportunities by watching what scientists, engineers, and other smart folks are doing outside of work, perhaps late at night or on the weekends. Blockchain may have started out that way. But today, it’s a topic that rises up to, or comes down from, the highest level in organizations — the C-suite or the Board of Directors. Why is that? One guess is that they see blockchain as a disruptive innovation focused on challenging core competencies and going outside of the box to amplify corporate synergies, finding opportunities in AI, and gobbling up low-hanging fruit. Just kidding. I was trying to use as many meaningless buzzwords as possible in one sentence. But the reality is not too far off: The top level of management is charged with finding and responding to risks and opportunities that lurk further out, beyond the blocking and tackling of tactical business execution, metaphorically crouching behind a dumpster to surprise the marathon runner in mile 20. Wrap up, Part 1: What are some things that investors love about blockchain? Blockchain-based energy companies can be attractive because...

Wrap up, Part 2: What are some attributes that investors hate...ur...worry about blockchain-based energy ventures? Investments in blockchain-based energy companies can be challenged because...

Conclusion: Is there one? OK, so like many emerging sectors for investment, there is plenty of risk and reward. But as they say, “Sitting on the sidelines is no way to win a game.” (Can you tell that it’s almost March Madness. I grew up in Kentucky and am a professor at Duke and UNC, so go blue!) As IBM put it in a recent Tweet, “We do not know where #blockchain will go, but there is a need to jump on board!”

0 Comments

Let’s be clear about one thing. It really could have been you.

You knew about cryptocurrency way earlier than your friends. You could explain blockchain to your grandmother in less than 60 seconds. But you did not pull the trigger. Some hint of disbelief that something so newfangled and profoundly nerdy could not take over our collective financial imagination. So, here you are today with a severe case of FOMO, watching cryptocurrency values skyrocket (and plummet and skyrocket again), and your 20/20 hindsight dreams of overnight millions squashed. We are all feeling it, though funny enough, the ones that are feeling it the most are probably the ones that did invest and are riding that roller coaster up, down, up, up, down, up. Why didn’t I buy more!?!? $1,000 dollars invested in Bitcoin in 2013 would be over $300,000 today (though this could easily spike or plunge 25% just while I am writing this piece). The agony! As of this writing, Bitcoin had lost more than 60% of its value since its peak at over $19,000 in late December. Heed the crash and avoid Bitcoin like the plague, or buy low as smart investors do during an overcorrection? Again, the agony! An unintended consequence of the fervor around Bitcoin, as well as some other popular cryptocurrencies like Ether and Ripple, is the new public debate about the potential of blockchain to disrupt (!) industries other than just the financial sector. Any industry that is founded on the flow of information and money qualifies, so that’s basically everything. But is blockchain a panacea, destined to democratize data and money, all the while disintermediating the entrenched intermediaries that dominate the global economy? Of course, there are camps firmly planted on both sides of that debate. I am not here to stake my flag on one side or the other. Rather, I aim to take a sober view of where blockchain may actually be the revolutionary technology that it is touted to be, and where it fails to live up the hype. Before we get started, there are any number of awesome explanations as to what blockchain is - see here (PwC) and here (IEEE) for two of my favorites. Here is my heroic attempt to distill blockchain to its bare bones essence:

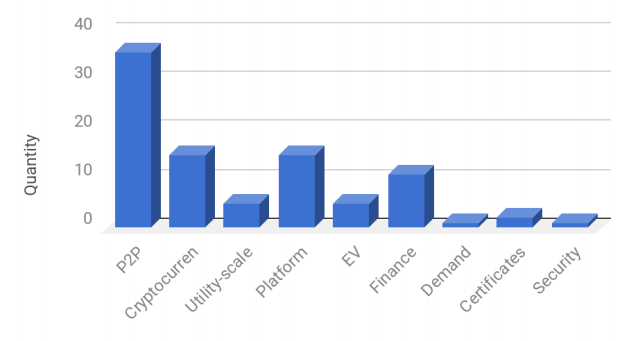

That sounds kind of revolutionary, so what am I missing? At its core, blockchain is most suitable in contexts in which data transfer (communication) is challenging, trust and privacy is highly valued, and data security is paramount. Again, this sounds like virtually everything that takes place on the Internet. This comes to bear primarily in two places: (1) the increasing number of unwieldy, siloed data systems that are highly susceptible to cybersecurity issues (e.g., see here for the 17 biggest data breaches in the 21st century) and (2) markets that are hampered by unnecessary inefficiencies, limitations, and complexities due to costly intermediaries. Seen through this lens, the energy sector is an excellent test case to take a deeper look into potential applications and pitfalls of blockchain technology. Sounding the Emergency Horn for Energy Monopolies The electric grid is arguably the most impressive technological achievement in the modern world. At the very least, it is certainly one of the most impactful to our everyday lives. The extraordinary cost and complexity of the electric grid initially lent it to monopoly protection by governments seeking order and control over its development and management. The last several decades have seen the unraveling of the heavy regulation supporting electric utility monopolies in many areas of the world, which have given way to more competitive markets in which many different types of energy providers, generators, and other service providers vy for customers. This has opened the floodgates to a much more diverse set of actors engaging in energy transactions via the grid, yet antiquated regulation and entrenched utility interests still limit the ways in which producers and consumers can transact for power and energy-related services, especially micro-transactions. Blockchain applications in the energy sector are positioned squarely at the crossroads of deregulation and the empowerment the market participants (e.g., consumers, prosumers, generators, etc.). Consumers and producers can form a more direct relationship with each other using blockchain technology wherein smart contracts (very smart) are used to transact for power and other grid services. As direct procurement and contracting scales, the role of the electric utility may be relegated to managing the transmission and distribution infrastructure, which, in many markets, would be a significantly reduced role in the functioning of the market. (Gulp.) This simple example may naturally lead you to conclude that peer-to-peer (P2P) energy trading is the inevitable future for the energy sector. Imagine you have excess rooftop solar generation you would like to sell your neighbor across the street -- the blissful life of the prosumer. This fanciful scheme is actually being tested and enacted in a small number of demonstrations. However, for reasons that we will get into shortly, P2P energy trading is neither the most likely nor nearest-term viable application of blockchain technology. Where Blockchain Finds its Groove in the Energy Sector Let’s start with the good news. The ballyhooed explosion of cryptocurrencies, which has fueled the popularity of blockchain, is not the only game in the energy sector. There are a wide range of applications from energy trading (e.g., grid management, microgrids, wholesale and P2P trading) to asset management (e.g., data collection and processing) to renewable energy certificate tracking to mobile payments (e.g., electric vehicle charging), among many others. To say that there has been an explosion of emerging companies in this space in recent years would be an understatement. But how many companies have a legitimate product, and, importantly, a viable market application with willing [and ready] customers is an entirely different question. Most energy and blockchain companies still bask in rose-tinted fields of possibility, while precious few have deployed a commercial product beyond demonstration projects. Not to despair, we are still in the early stages. But neither does that mean that this process of innovation and experimentation will inevitably lead to a wholesale disruption (!) of the electricity sector. As with many prognostications (especially related to technological innovation), please take my ranking of energy + blockchain applications in order of their long-term viability and timing to market with the requisite grain of salt:

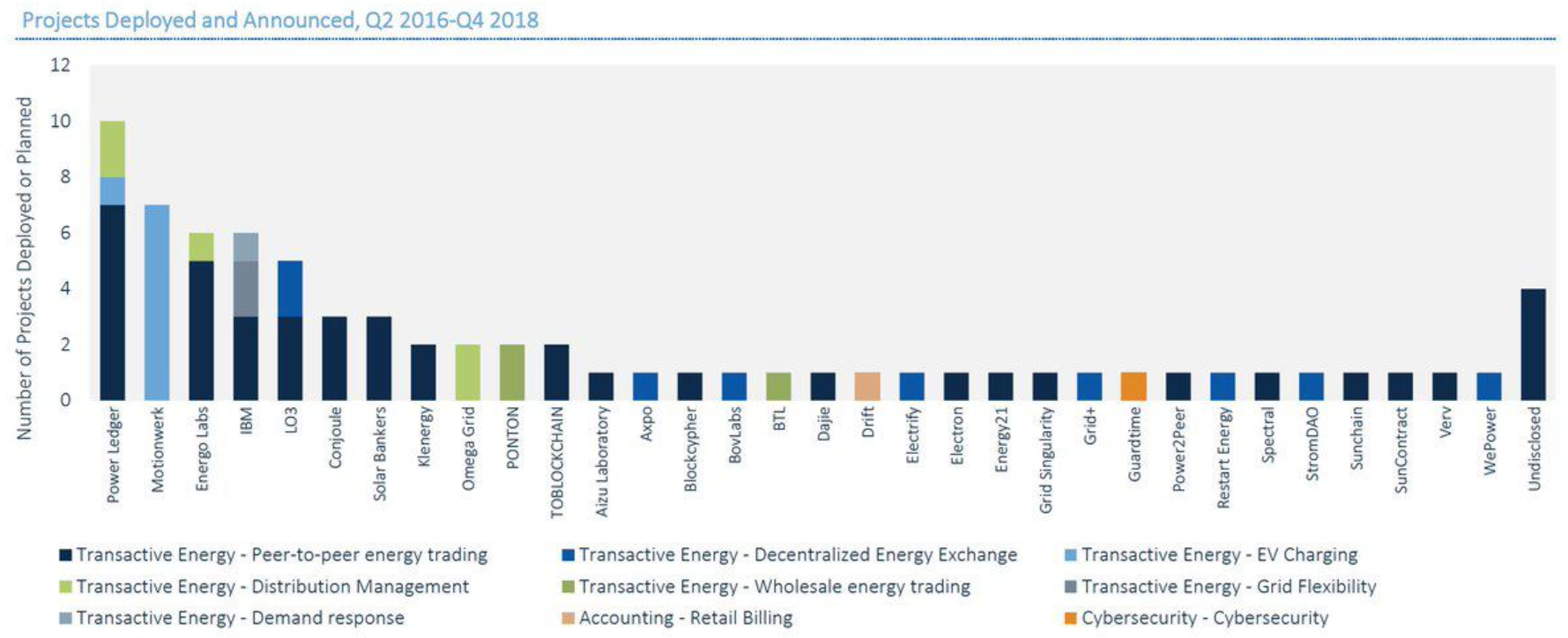

Check out SolarPlaza’s comprehensive guide to companies in the energy + blockchain space. The World Energy Council takes a different tack with their energy + blockchain use case taxonomy. While certainly extensive, I am relatively certain both of these excellent resources have missed some under-the-radar companies and sub-sectors that will emerge in the coming months and years. That said, it is no small task to track this rapidly evolving space. The bottom line is that blockchain may not be a panacea, but it certainly could be part of an enabling technological solution to drive the transition to a more distributed, digital, secure, and renewable electric grid. One of the more encouraging developments has been that blockchain has not only unleashed a wave of innovation at the startup level, but also inspired the formation of a number of non-profit consortia working in collaboration to support the energy + blockchain space. The Energy Web Foundation, HyperLedger, and Enerchain are among the most prominent efforts, each of which is backed by the who’s who of corporate behemoths. So, pick your favorite energy technical challenge (as if I had to even ask) and keep up with the rapid pace of progress. Energy-backed Cryptocurrency Beat Down As we started on this journey, I led with the remarkable explosion of interest and speculation in the cryptocurrency markets. To be clear, this is by no means limited to cryptocurrencies that you could recognize by name -- Bitcoin, Ether, Ripple, etc. Various market tracking websites list over 4,500 cryptocurrencies worth nearly $500B. To put that in perspective, the US Gross Domestic Product (GDP) is a bit over $18T, which means that the global cryptocurrency market is valued at over 5% of the US economy. (You can thank me later for that bit of cocktail chatter.) If you want to kill a couple of hours, take a look through some of the more esoteric cryptocurrencies, and your mind will be blown at the number of completely ridiculous schemes underpinning these financial instruments: Coins to gain VIP entrance to Las Vegas strip clubs to coins that allow you to buy objects in video games. This explosion of cryptocurrencies are a true testament to human ingenuity. At least one cryptocurrency plainly states that it is merely a means for guileless investors to give them money for nothing. Kudos for the honesty. In the energy space, there are a number of attempts to use cryptocurrencies or tokens as a medium of exchange for power and other energy services. The general proposition is that a coin or token is minted by a company, which confers upon the owner the right to some future consumptive good. A simple example would be a coin could be exchanged for X kWh of electricity generated by a solar farm. Sounds pretty simple and compelling, right? Upon deeper inspection, a number of key friction points become clear. First, these coins presuppose that an independent exchange functioning separate and apart from the existing energy markets can arise magically out the much lauded network effect. More consumers demanding, purchasing, utilizing, and trading coins, and more producers generating electricity in exchange for coins, selling those coins for other cryptocurrencies, and then monetizing those cryptocurrencies outside of the exchange. A producer generates electricity and exchanges the right to consume that electricity for a coin. That coin gets purchased with another more liquid cryptocurrency like Bitcoin or Ether, which can then be exchanged for a fiat currency like U.S. dollars that has exchange value for other goods and services in today’s economy. A consumer buys the coin with their Bitcoin, Ether, etc., and then can either consume the services underpinning the coin (e.g., electric power in many cases), hold it, or trade it to someone who places an even greater value on those services. Now, the real magic lies in believing that transacting for kWh’s of electricity in this exchange will be an overall better proposition for the producer. In other words, will the producer be able to generate more revenue with a similar or greater degree of predictability using some energy-backed coin or token compared to more conventional methods of either project finance using long-term power purchase agreements (PPAs) in the case of standalone renewable energy projects or net metering in the case of rooftop solar on homes? The answer is anyone’s guess. But there are certainly blockchain-based energy companies banking on producers flocking to alternative forms of project finance or market compensation. There is a part of this puzzle which simply does not make sense. Imagine you have the opportunity to make a wager based on the future value of a kWh of electricity. How bullish are you that kWhs in the future will be worth much more than they are today? History would indicate that electricity prices do not tend to skyrocket in value in well-functioning markets. In the renewable energy space, electricity prices have plummeted in recent years. So, why would someone invest in an energy-backed cryptocurrency if the ceiling is so low on the value of the kWs of electricity backing the coin or token? From the issuer perspective, part of the appeal of minting an energy-based cryptocurrency is that it is a means for producers to acquire other, more liquid cryptocurrencies which have seen extraordinary increases in value recently. This has had appeal with the growing speculative fervor surrounding Bitcoin, Ether, etc. without using any of your precious dollars. It is a classic arbitrage scenario for you economics nerds. Imagine, for instance, that you, the producer, generated one MWh of electricity, were granted some energy-backed coin, and exchanged it for 10 Ether on January 1, 2017. At the time, you got a great deal, as the value of the Ether that you received was around $80 ($0.08/kWh), better than what you could have gotten in the merchant markets or through a PPA or net metering agreement. You decided that it was not worth your while to exchange the Ether for dollars, and you just held onto it. Today, you looked at your digital wallet, and lo and behold, the 10 Ether that you received from the original one MWh that you sold is now worth over $8,000. In just over a year, you grew the value derived from that MWh by over 100x! What is not to like about that? But who knows what is going to happen with Ether (or any other cryptocurrency) over the next year? So how long can the dream last? For the consumer, there needs to be interest in directly consuming those kWh of electricity, but that will not likely cut it. In addition, the consumer will need to believe that the exchange value for the coin or token will have a future speculative value greater than the purchase price. That has been a relatively easy sell to date, but there may be a weakening of that foundation with the growing volatility in many cryptocurrency values in recent months. The bottom line is that many energy-related cryptocurrencies are, either directly or indirectly, betting on Bitcoin, Ether and the other dominant, liquid cryptocurrencies to continue this meteoric rise (and fall only to rise again) in value, which is driving this explosion of coins and tokens to get a piece of the action. Is that the basis of a healthy, functioning cryptocurrency exchange? Only time with tell... An Obligatory Word about Energy Consumption You energy conservationists out there may be exclaiming -- “But doesn’t blockchain use an exorbitant amount of energy to run?!” Not really, and certainly not for the use cases that we are talking about. The doomsayer prognostications of world energy consumption being dominated by blockchain largely revolve around a faulty extrapolation of energy consumption from Bitcoin mining. Even the NYTimes got in on the hyperbole, though CNBC had a more sanguine view. Not to slip down that slope, but the bottom line is that this is a symptom of an immature technology scaling exponentially. No right-minded person could have possibly anticipated the speculative fever that would envelope Bitcoin, which has fueled increasingly extravagant investments in energy intensive processing capacity to compete as a Bitcoin miner. This can and will be corrected over time, just like it has been for the Internet, which was consumed by similar criticisms during its early years. So, this is a bit overwhelming, yet how can I be among the smarter people in the room on energy + blockchain... With a healthy balance of enthusiasm and skepticism, it is well worth your time and effort to keep a tally on the energy + blockchain space. There will inevitably be a litany of failed companies, over-hyped experiments, and even a likely SEC regulatory backlash (see the SEC Chairman’s latest statement on cryptocurrencies and ICOs). Notwithstanding, there is literally no doubt in my mind the blockchain technology is here to stay, and will, in all likelihood, catalyze a lot of change in how energy is financed, produced, bought and sold. It will not change everything, and will certainly not do it overnight. Blockchain is in its toddler years. Stumbling about (think explosion of crypto-schemes, coins, tokens, etc.) and occasionally articulated a coherent word of phrase (think legitimate business value proposition). Over time, and with a lot of falling down and bumping heads (you can tell I have a young child), this little toddler will grow up into being a much more mature little person (even then with a lot of room to grow). Until then, just enjoy the ride (and heed the SEC when they say that things are about the change). |

sign up for ironoak's NewsletterSent about twice per month, these 3-minute digests include bullets on:

Renewable energy | Cleantech & mobility | Finance & entrepreneurship | Attempts at humor (what?) author

Photo by Patrick Fore on Unsplash

|

© 2009-2022 IronOak Energy Capital, LLC | (888) 249-3013