|

11/5/2019 Outcompeting lithium-ion in the 2020’s — Which new energy storage technologies might win?Read Now

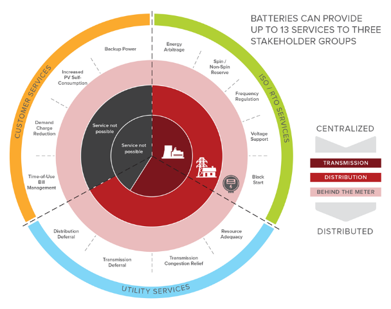

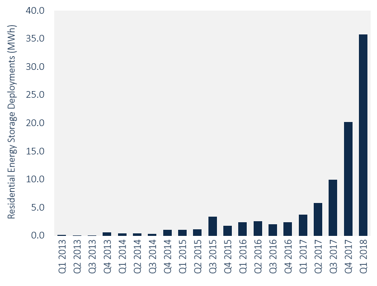

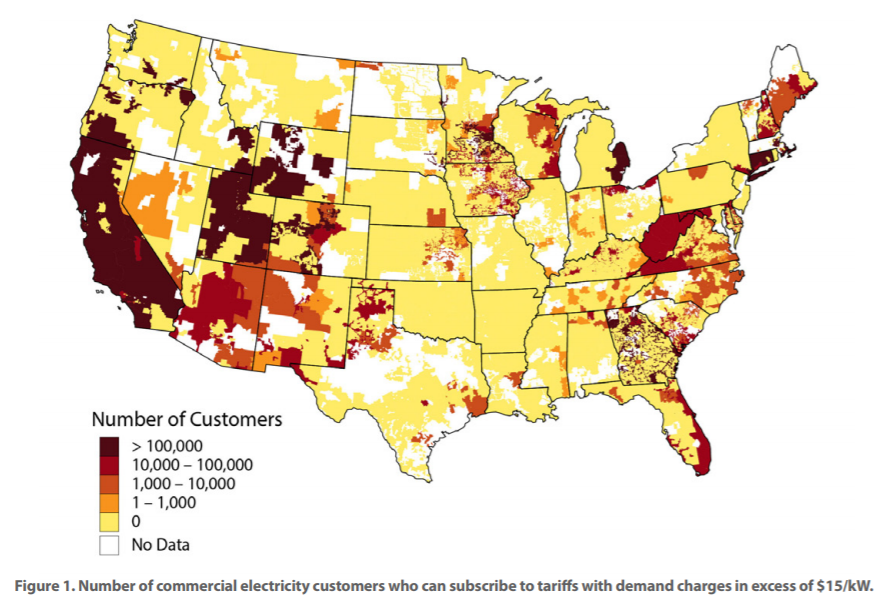

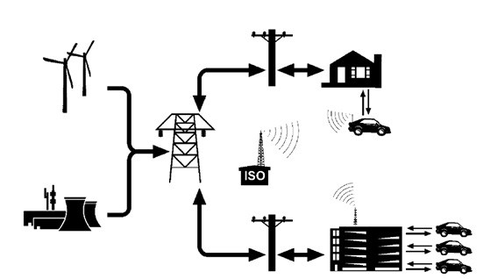

By: Chris Wedding, PhD “You miss 100% of the shots you don’t take.” Depending on whether you are from the South or the North, you’ll think that quote was attributed to Michael Jordan or Wayne Gretzky. With two degrees and a professorship at UNC Chapel Hill, I’m definitely going with MJ. Regardless, this pithy wisdom applies to our topic at hand — Innovators that harnessed blood, sweat, tears, and billions of dollars to shoot for the moon with bold battery solutions that did not work out. The silver lining (or maybe it’s lithium) is that those were the early days. And it’s better to gamble with pennies than with gold. Going forward through 2040, Bloomberg projects $620B to be invested in the battery sector. That’s a frighteningly large amount of capital. So we better learn lessons from those early failures and invest these dollars intelligently. First, a review of why batteries are wonderful... Below are three figures which tell a compelling story. #1 The 13 benefits that batteries can create for building owners (behind the meter), utilities (front of the meter), and grid operators (e.g., Independent System Operators). — Source: RMI  #2 The surprising growth of residential energy storage installation in the U.S. — Source: GTM Research / ESA U.S Energy Storage Monitor  #3 Areas of the U.S. where commercial and industrial energy storage can produce an attractive return on investment today, not in some distant future where Elon Musk is the next billionaire president. — Source: NREL  And now, a list of battery companies “with arrows in their backs” The following companies were cutting edge, but the cuts went too deep. God bless them for being innovators that were too early. A123 Systems

Alevo

Aquion Energy

Better Place

Fisker

In aggregate, these companies raised more than $5B from smart, accomplished, and connected investors, such as the following:

Sources: Pitchbook, Crunchbase, Greentech Media, PV Magazine, VentureBeat, and the New Yorker Finally, 10 lessons for “keeping your shoes clean in a cow field” #1 Focus. Focus. Focus. — Some battery manufacturers tried to serve multiple markets and geographies, across both stationary (power grid) and EV (electric vehicle) sectors. You have to pick. Say no. You’ve heard it before: “If you try to please everyone, you’ll end up pleasing no one.” #2 Vet storage technologies the way that investors vet energy project investments — This matters because ultimately tech needs to scale into deployments. Below are six questions to ask of a battery technology and company:

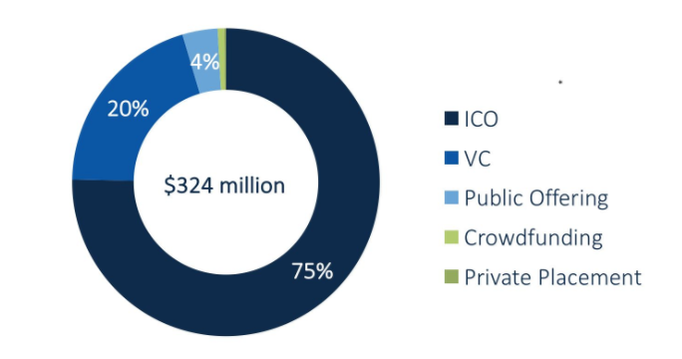

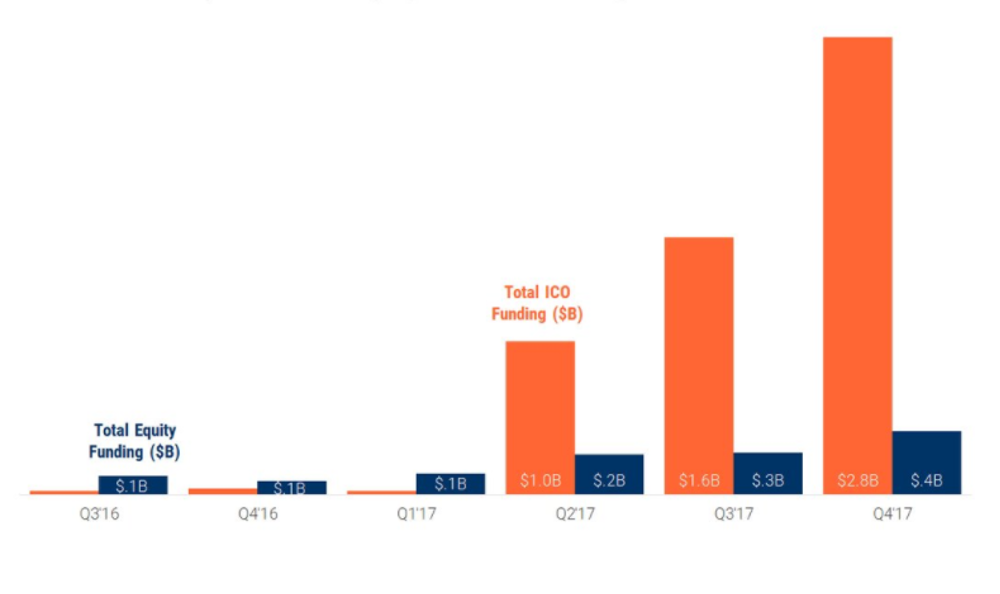

#3 Apply the pre-mortem — Watch for “froth.” If all investors are in love with the company, ask why it could fail. Once you identify the flaws, ask whether there are risk mitigation strategies, and if you believe them. Ignorance is not bliss. #4 Manage burn-rate like a hawk — Raising a big round, or being on a rocket ship based on confident financial projections are not excuses to spend too much. Pretend your dad was a CPA like mine. Make sure a board is in place and that they firmly hold the executive team accountable, without applying a death grip. #5 Compete against the giants with your eyes wide open — If the battery technology company wants to oust lithium-ion batteries from their global dominance, then get ready for a long, uphill battle. Granted, at the top of that hill, you might see a pot of gold waiting. But you may have aged a decade in the process. Or maybe instead you should just climb a different hill: Find a niche use case where lithium-ion is not the answer. Find its weakest performance parameter, innovate to excel on that same attribute, and then find the one customer segment in a specific geography that loses sleep over that problem you could solve with a non-lithium-ion solution. #6 Don’t depend on business-to-customer sale channels — As individuals, we are fickle, distracted buyers. Businesses are not. They seek what’s best for them and buy in large quantities. Find battery companies that make businesses happy. Then sell to them in order to reach your ultimate customer, whether it is the business or that business’ customers. For example, make the utility or auto manufacturer your friend, not your foe. #7 Partner with strategic investors — These guys (and gals) provide three benefits: (1) They might be more patient with their capital, allowing time to maximize company value before exiting an investment. (2) They can provide fantastic validation that the storage company has market potential and may indeed scratch their own itch. (3) They can be extraordinary customers that “make the business,” adding serious revenue through large contracts. #8 Raise capital before you need it — Plenty of companies run out of cash before they raise their next round. This was also true for some early stage storage startups. Don’t depend on cash flows for growth too early on in the business. Raise more than you think you need, share the pie, and earn the opportunity to watch it grow. #9 Prioritize capital-light business models — If the battery company wants to use lots of venture capital to build factories, run away. Far away. Instead, contract manufacturing, creative lines of credit, and supportive supply chain partners can reduce capital cost needs. In addition, it always helps to invest in the “brains” of the storage devices. Get some intellectual property, some software, and some automation. #10 Good looks alone won’t cut it — Cool design can’t overcome poor quality or inconvenience. That said, ugly form factors can also be recipe for inducing yawns if there is any consumer component to the sales cycle. Find the balance. But keep your eye on the target: High performance. In conclusion… I’ll conclude with a relevant metaphor that takes me back to my days in Kentucky... We’re off to the races. Don’t be too late to make that bet. Pick your jockey(s). Pick your horse(s). The prize money is much more than a bucket of oats.  By: Dr. Chris Wedding, Managing Partner In the last quarter, investors poured more than $324M into blockchain for energy companies. Can you believe that? Well, you shouldn’t. But which part is most unbelievable? While $324M seems shocking, it’s all about context. That amount has indeed been raised, but it’s taken 12 months to do so, according to GTM Research. What’s more shocking is that over 75% of this capital has been raised via Initial Coin Offerings, or ICOs. When thinking about this emerging market, it’s kind of like being back in high school: Some investors have FOMO (Fear of Missing Out). But others think they’re too cool to hang out with the kid who just became popular after years of dork-dom. But what should you, oh wise capital providers and ye capital-hungry blockchain entrepreneurs who worship the clean energy gods of purity, know about blockchain-focused energy opportunities? Here are our top 4, out of our longer list of 75. (I exaggerate slightly.) 1. There are 120+ blockchain energy companies. But most are relative newbs. Yep, that’s a term from my kiddos. I can’t wait to finish this blog so I can go tell them I used their word correctly. But do I use the word “newbs” to be mean? Heavens, no. I’m a good Catholic-Buddhist, after all. (Oh, they exist.) What I’m referring to is the age or maturity of most companies in this sector. Research from Solarplaza suggests that most ventures were formed in 2016 or 2017, and investors at the GTM Blockchain Forum note that most founders have little to no operational business expertise. That does not mean that these young ventures lack merit. But it does make the hill to success tougher to climb. (Think steep slopes covered in poison ivy and man-sized Venus flytraps.) As Greentech Media’s Chairman observed [paraphrase]: “We see many white papers for ICOs sponsored by blockchain in energy startups. Some are are interesting. But some are sketchy.” Another panelist at a recent blockchain energy conference noted: "We're currently working with Atari, but we need to be using Playstation 4 to make most [blockchain for energy use cases] work at scale.” An investor panelist put it another way [paraphrase]: “Blockchain is today where the Kardashians were in 2008. When their name is on something, it can print money. But then smart people ask ‘Why? What businesses do they really have? Maybe a clothing line, a home video business (get it?), and a few others?’ But then you realize there is a genius marketing mastermind behind it all. The hype is, in fact, part of the cause for success.” Lastly, all hail innovation. Seriously. This is how it works: First, divergence. Second, convergence. However, we’re very far from the latter. 2. There are a bazillion use cases. And the energy world is 6-trillion-dollars big. Just in case you thought that 120 companies in the same emerging sector was a lot, think again. The Energy Web Foundation, co-led by our friends at the Rocky Mountain Institute, see over 200 potential uses cases for blockchain in energy. Even if only half of those scenarios prove to be real, that is still many, many niche markets ripe for multiple companies to do well in many geographies. Moreover, the energy industry is not a tiny pearl hiding in a small oyster. It’s more like an ocean full of 100-foot long blue whales, as plentiful as squirrels on a college campus. But seriously...no wine glass in hand...The energy market is one of the biggest industries on the planet, and it’s full of intermediaries that control the flow of electricity and money. This creates a huge playground for diverse and interoperable blockchains, distributed and trusted ecosystems of counterparties, and automated and smart contracting abilities.    3. ICOs are crushing equity investors. But that can (should?) not continue. In the broader universe of early-stage blockchain companies, ICOs are killing venture capital. I mean, like the Incredible Hulk vs. me in a boxing ring, or some such awful mismatch. However, the U.S. Securities and Exchange Commission is taking a pretty hard look at ICOs — in the past, present, and future. And let’s just say that their eyebrows are raised, you know, where one is raised higher than the other. While many ICOs have tried to avoid SEC oversight, when it walks like a duck and quacks like a duck, then...It’s a security. (If you don’t know what I mean, take a look at their guidance here.) All is not lost for conventional equity investors. Venture capital and corporate strategic investors bring value that can be far greater than capital alone. (The latter is the extent of the contribution from ICOs.) The other benefits of working with institutional equity investors include rich networks that can lead to partners and customers, insights on corporate governance based on lessons learned from dozens of past ventures, and deep sector expertise to allow for threat and opportunity recognition beyond what the core team might focus on while their heads are down building a company.  Capital Raised for Blockchain Companies: Q3 2016 to Q4 1017 Equity (blue) vs. ICOs (orange) Source: CBInsights, Tokendata  4. Blockchain is not just for nerds. It’s for the C-suite.

Some famous venture capitalists have said that they look for the next big investment opportunities by watching what scientists, engineers, and other smart folks are doing outside of work, perhaps late at night or on the weekends. Blockchain may have started out that way. But today, it’s a topic that rises up to, or comes down from, the highest level in organizations — the C-suite or the Board of Directors. Why is that? One guess is that they see blockchain as a disruptive innovation focused on challenging core competencies and going outside of the box to amplify corporate synergies, finding opportunities in AI, and gobbling up low-hanging fruit. Just kidding. I was trying to use as many meaningless buzzwords as possible in one sentence. But the reality is not too far off: The top level of management is charged with finding and responding to risks and opportunities that lurk further out, beyond the blocking and tackling of tactical business execution, metaphorically crouching behind a dumpster to surprise the marathon runner in mile 20. Wrap up, Part 1: What are some things that investors love about blockchain? Blockchain-based energy companies can be attractive because...

Wrap up, Part 2: What are some attributes that investors hate...ur...worry about blockchain-based energy ventures? Investments in blockchain-based energy companies can be challenged because...

Conclusion: Is there one? OK, so like many emerging sectors for investment, there is plenty of risk and reward. But as they say, “Sitting on the sidelines is no way to win a game.” (Can you tell that it’s almost March Madness. I grew up in Kentucky and am a professor at Duke and UNC, so go blue!) As IBM put it in a recent Tweet, “We do not know where #blockchain will go, but there is a need to jump on board!” Let’s be clear about one thing. It really could have been you.

You knew about cryptocurrency way earlier than your friends. You could explain blockchain to your grandmother in less than 60 seconds. But you did not pull the trigger. Some hint of disbelief that something so newfangled and profoundly nerdy could not take over our collective financial imagination. So, here you are today with a severe case of FOMO, watching cryptocurrency values skyrocket (and plummet and skyrocket again), and your 20/20 hindsight dreams of overnight millions squashed. We are all feeling it, though funny enough, the ones that are feeling it the most are probably the ones that did invest and are riding that roller coaster up, down, up, up, down, up. Why didn’t I buy more!?!? $1,000 dollars invested in Bitcoin in 2013 would be over $300,000 today (though this could easily spike or plunge 25% just while I am writing this piece). The agony! As of this writing, Bitcoin had lost more than 60% of its value since its peak at over $19,000 in late December. Heed the crash and avoid Bitcoin like the plague, or buy low as smart investors do during an overcorrection? Again, the agony! An unintended consequence of the fervor around Bitcoin, as well as some other popular cryptocurrencies like Ether and Ripple, is the new public debate about the potential of blockchain to disrupt (!) industries other than just the financial sector. Any industry that is founded on the flow of information and money qualifies, so that’s basically everything. But is blockchain a panacea, destined to democratize data and money, all the while disintermediating the entrenched intermediaries that dominate the global economy? Of course, there are camps firmly planted on both sides of that debate. I am not here to stake my flag on one side or the other. Rather, I aim to take a sober view of where blockchain may actually be the revolutionary technology that it is touted to be, and where it fails to live up the hype. Before we get started, there are any number of awesome explanations as to what blockchain is - see here (PwC) and here (IEEE) for two of my favorites. Here is my heroic attempt to distill blockchain to its bare bones essence:

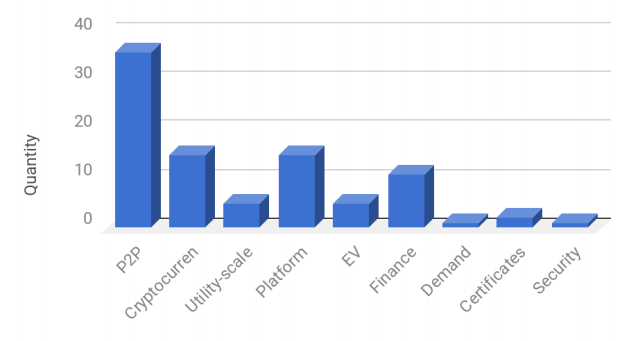

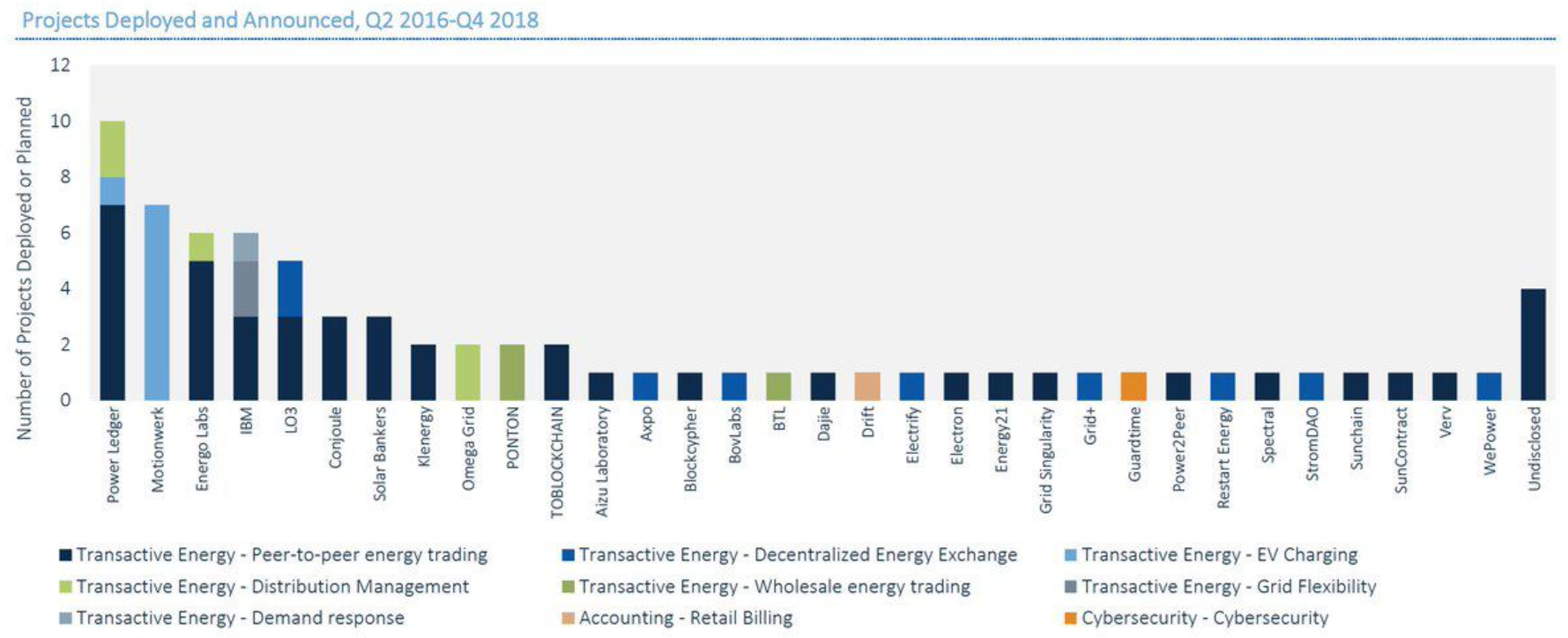

That sounds kind of revolutionary, so what am I missing? At its core, blockchain is most suitable in contexts in which data transfer (communication) is challenging, trust and privacy is highly valued, and data security is paramount. Again, this sounds like virtually everything that takes place on the Internet. This comes to bear primarily in two places: (1) the increasing number of unwieldy, siloed data systems that are highly susceptible to cybersecurity issues (e.g., see here for the 17 biggest data breaches in the 21st century) and (2) markets that are hampered by unnecessary inefficiencies, limitations, and complexities due to costly intermediaries. Seen through this lens, the energy sector is an excellent test case to take a deeper look into potential applications and pitfalls of blockchain technology. Sounding the Emergency Horn for Energy Monopolies The electric grid is arguably the most impressive technological achievement in the modern world. At the very least, it is certainly one of the most impactful to our everyday lives. The extraordinary cost and complexity of the electric grid initially lent it to monopoly protection by governments seeking order and control over its development and management. The last several decades have seen the unraveling of the heavy regulation supporting electric utility monopolies in many areas of the world, which have given way to more competitive markets in which many different types of energy providers, generators, and other service providers vy for customers. This has opened the floodgates to a much more diverse set of actors engaging in energy transactions via the grid, yet antiquated regulation and entrenched utility interests still limit the ways in which producers and consumers can transact for power and energy-related services, especially micro-transactions. Blockchain applications in the energy sector are positioned squarely at the crossroads of deregulation and the empowerment the market participants (e.g., consumers, prosumers, generators, etc.). Consumers and producers can form a more direct relationship with each other using blockchain technology wherein smart contracts (very smart) are used to transact for power and other grid services. As direct procurement and contracting scales, the role of the electric utility may be relegated to managing the transmission and distribution infrastructure, which, in many markets, would be a significantly reduced role in the functioning of the market. (Gulp.) This simple example may naturally lead you to conclude that peer-to-peer (P2P) energy trading is the inevitable future for the energy sector. Imagine you have excess rooftop solar generation you would like to sell your neighbor across the street -- the blissful life of the prosumer. This fanciful scheme is actually being tested and enacted in a small number of demonstrations. However, for reasons that we will get into shortly, P2P energy trading is neither the most likely nor nearest-term viable application of blockchain technology. Where Blockchain Finds its Groove in the Energy Sector Let’s start with the good news. The ballyhooed explosion of cryptocurrencies, which has fueled the popularity of blockchain, is not the only game in the energy sector. There are a wide range of applications from energy trading (e.g., grid management, microgrids, wholesale and P2P trading) to asset management (e.g., data collection and processing) to renewable energy certificate tracking to mobile payments (e.g., electric vehicle charging), among many others. To say that there has been an explosion of emerging companies in this space in recent years would be an understatement. But how many companies have a legitimate product, and, importantly, a viable market application with willing [and ready] customers is an entirely different question. Most energy and blockchain companies still bask in rose-tinted fields of possibility, while precious few have deployed a commercial product beyond demonstration projects. Not to despair, we are still in the early stages. But neither does that mean that this process of innovation and experimentation will inevitably lead to a wholesale disruption (!) of the electricity sector. As with many prognostications (especially related to technological innovation), please take my ranking of energy + blockchain applications in order of their long-term viability and timing to market with the requisite grain of salt:

Check out SolarPlaza’s comprehensive guide to companies in the energy + blockchain space. The World Energy Council takes a different tack with their energy + blockchain use case taxonomy. While certainly extensive, I am relatively certain both of these excellent resources have missed some under-the-radar companies and sub-sectors that will emerge in the coming months and years. That said, it is no small task to track this rapidly evolving space. The bottom line is that blockchain may not be a panacea, but it certainly could be part of an enabling technological solution to drive the transition to a more distributed, digital, secure, and renewable electric grid. One of the more encouraging developments has been that blockchain has not only unleashed a wave of innovation at the startup level, but also inspired the formation of a number of non-profit consortia working in collaboration to support the energy + blockchain space. The Energy Web Foundation, HyperLedger, and Enerchain are among the most prominent efforts, each of which is backed by the who’s who of corporate behemoths. So, pick your favorite energy technical challenge (as if I had to even ask) and keep up with the rapid pace of progress. Energy-backed Cryptocurrency Beat Down As we started on this journey, I led with the remarkable explosion of interest and speculation in the cryptocurrency markets. To be clear, this is by no means limited to cryptocurrencies that you could recognize by name -- Bitcoin, Ether, Ripple, etc. Various market tracking websites list over 4,500 cryptocurrencies worth nearly $500B. To put that in perspective, the US Gross Domestic Product (GDP) is a bit over $18T, which means that the global cryptocurrency market is valued at over 5% of the US economy. (You can thank me later for that bit of cocktail chatter.) If you want to kill a couple of hours, take a look through some of the more esoteric cryptocurrencies, and your mind will be blown at the number of completely ridiculous schemes underpinning these financial instruments: Coins to gain VIP entrance to Las Vegas strip clubs to coins that allow you to buy objects in video games. This explosion of cryptocurrencies are a true testament to human ingenuity. At least one cryptocurrency plainly states that it is merely a means for guileless investors to give them money for nothing. Kudos for the honesty. In the energy space, there are a number of attempts to use cryptocurrencies or tokens as a medium of exchange for power and other energy services. The general proposition is that a coin or token is minted by a company, which confers upon the owner the right to some future consumptive good. A simple example would be a coin could be exchanged for X kWh of electricity generated by a solar farm. Sounds pretty simple and compelling, right? Upon deeper inspection, a number of key friction points become clear. First, these coins presuppose that an independent exchange functioning separate and apart from the existing energy markets can arise magically out the much lauded network effect. More consumers demanding, purchasing, utilizing, and trading coins, and more producers generating electricity in exchange for coins, selling those coins for other cryptocurrencies, and then monetizing those cryptocurrencies outside of the exchange. A producer generates electricity and exchanges the right to consume that electricity for a coin. That coin gets purchased with another more liquid cryptocurrency like Bitcoin or Ether, which can then be exchanged for a fiat currency like U.S. dollars that has exchange value for other goods and services in today’s economy. A consumer buys the coin with their Bitcoin, Ether, etc., and then can either consume the services underpinning the coin (e.g., electric power in many cases), hold it, or trade it to someone who places an even greater value on those services. Now, the real magic lies in believing that transacting for kWh’s of electricity in this exchange will be an overall better proposition for the producer. In other words, will the producer be able to generate more revenue with a similar or greater degree of predictability using some energy-backed coin or token compared to more conventional methods of either project finance using long-term power purchase agreements (PPAs) in the case of standalone renewable energy projects or net metering in the case of rooftop solar on homes? The answer is anyone’s guess. But there are certainly blockchain-based energy companies banking on producers flocking to alternative forms of project finance or market compensation. There is a part of this puzzle which simply does not make sense. Imagine you have the opportunity to make a wager based on the future value of a kWh of electricity. How bullish are you that kWhs in the future will be worth much more than they are today? History would indicate that electricity prices do not tend to skyrocket in value in well-functioning markets. In the renewable energy space, electricity prices have plummeted in recent years. So, why would someone invest in an energy-backed cryptocurrency if the ceiling is so low on the value of the kWs of electricity backing the coin or token? From the issuer perspective, part of the appeal of minting an energy-based cryptocurrency is that it is a means for producers to acquire other, more liquid cryptocurrencies which have seen extraordinary increases in value recently. This has had appeal with the growing speculative fervor surrounding Bitcoin, Ether, etc. without using any of your precious dollars. It is a classic arbitrage scenario for you economics nerds. Imagine, for instance, that you, the producer, generated one MWh of electricity, were granted some energy-backed coin, and exchanged it for 10 Ether on January 1, 2017. At the time, you got a great deal, as the value of the Ether that you received was around $80 ($0.08/kWh), better than what you could have gotten in the merchant markets or through a PPA or net metering agreement. You decided that it was not worth your while to exchange the Ether for dollars, and you just held onto it. Today, you looked at your digital wallet, and lo and behold, the 10 Ether that you received from the original one MWh that you sold is now worth over $8,000. In just over a year, you grew the value derived from that MWh by over 100x! What is not to like about that? But who knows what is going to happen with Ether (or any other cryptocurrency) over the next year? So how long can the dream last? For the consumer, there needs to be interest in directly consuming those kWh of electricity, but that will not likely cut it. In addition, the consumer will need to believe that the exchange value for the coin or token will have a future speculative value greater than the purchase price. That has been a relatively easy sell to date, but there may be a weakening of that foundation with the growing volatility in many cryptocurrency values in recent months. The bottom line is that many energy-related cryptocurrencies are, either directly or indirectly, betting on Bitcoin, Ether and the other dominant, liquid cryptocurrencies to continue this meteoric rise (and fall only to rise again) in value, which is driving this explosion of coins and tokens to get a piece of the action. Is that the basis of a healthy, functioning cryptocurrency exchange? Only time with tell... An Obligatory Word about Energy Consumption You energy conservationists out there may be exclaiming -- “But doesn’t blockchain use an exorbitant amount of energy to run?!” Not really, and certainly not for the use cases that we are talking about. The doomsayer prognostications of world energy consumption being dominated by blockchain largely revolve around a faulty extrapolation of energy consumption from Bitcoin mining. Even the NYTimes got in on the hyperbole, though CNBC had a more sanguine view. Not to slip down that slope, but the bottom line is that this is a symptom of an immature technology scaling exponentially. No right-minded person could have possibly anticipated the speculative fever that would envelope Bitcoin, which has fueled increasingly extravagant investments in energy intensive processing capacity to compete as a Bitcoin miner. This can and will be corrected over time, just like it has been for the Internet, which was consumed by similar criticisms during its early years. So, this is a bit overwhelming, yet how can I be among the smarter people in the room on energy + blockchain... With a healthy balance of enthusiasm and skepticism, it is well worth your time and effort to keep a tally on the energy + blockchain space. There will inevitably be a litany of failed companies, over-hyped experiments, and even a likely SEC regulatory backlash (see the SEC Chairman’s latest statement on cryptocurrencies and ICOs). Notwithstanding, there is literally no doubt in my mind the blockchain technology is here to stay, and will, in all likelihood, catalyze a lot of change in how energy is financed, produced, bought and sold. It will not change everything, and will certainly not do it overnight. Blockchain is in its toddler years. Stumbling about (think explosion of crypto-schemes, coins, tokens, etc.) and occasionally articulated a coherent word of phrase (think legitimate business value proposition). Over time, and with a lot of falling down and bumping heads (you can tell I have a young child), this little toddler will grow up into being a much more mature little person (even then with a lot of room to grow). Until then, just enjoy the ride (and heed the SEC when they say that things are about the change). Ah, to have a crystal ball and see this future play out.

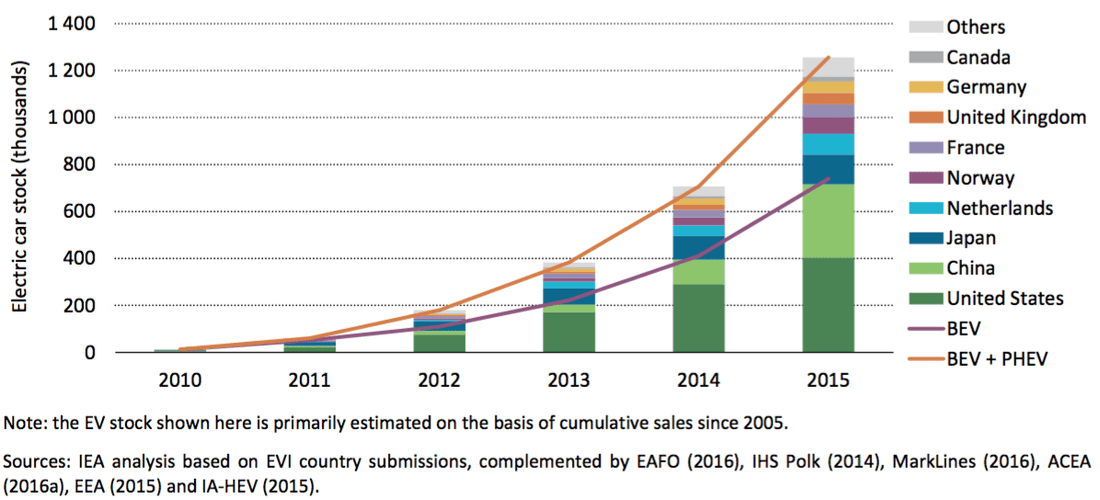

Or better yet, to be a character in the movie Back to the Future. Also about futuristic cars, I might add. (If you don’t know what I’m talking about, go ask a super “old person,” like a 41-year-old. Oh how my kiddos define “old.”) Maybe you care about future growth estimates for electric vehicles (EVs) because you stand to win… For example, EV manufacturers, utilities that can better monetize sunk costs in power generation assets during off-peak hours, battery makers, NGOs working to protect human health, or lithium and other precious metal supply chains. Or maybe you care because you’re industry stands to lose, at least initially… For example, major car manufacturers, government leaders concerned about falling revenues linked to gasoline taxes, utilities unable to manage peak power challenges, or...um...the oil industry. Whatever the motivation, one thing is for sure… There is no agreement on how, when, or if EVs will come to dominate the transportation sector. And importantly, the same metric used for these EV projections is often not the same. It could be “percentage of new sales” or “percentage of total vehicles on the road.” Even trickier is the fact that calculations from various sources do not use the same year for the end state. Some use 2030, others 2040, and...well...you get the idea. It’s almost intentionally confusing so as to prevent an apples-to-apples comparisons among different EV projections. So, here are five things to keep in mind regarding the “all over the map” nature of future EV growth. 1. Calculations for EV expansion continue to be revised upward (more favorably) No one is perfect, and all estimates of future EV growth are wrong. As such, credible sources for these data frequently offer updated projections. Consider the US Energy Information Administration (EIA). Almost everyone considers this to be an authoritative source on energy trends, though many agree they have been conservative when envisioning (or being blind to) renewable energy’s rapid recent growth. (See explanation from David Roberts at Vox.) The US EIA’s vision for EV sales three months ago is 2x higher than one year ago, and 10x higher than its estimates from ten years ago. 2. Estimates for EV penetration by 2020 vary by 11x, depending on the source Consider the range of EV adoption from these trusted sources:

It’s also worth stating the obvious: The disruptive nature of EVs is significant enough that non-transportation management consultancies and big banks like PwC, Deutsche Bank, Deloitte, and BCG are spending time making forecasts to win new business in the sector. #NotaTinyNiche (Yep, Millennial readers, I’m so hip that I just dropped a hashtag.) 3. Non-proponents of EV (Fitch Ratings, big oil executives) are taking notice of its potentially significant impacts It’s not uncommon to hear the term “death spiral” in reference to utilities who face increasingly tough competition when electricity from solar plus storage becomes cheaper than grid power. But those statements, sometimes deemed hyperbolic, tend to come from renewable energy proponents. Biased, one might say. This time, it is instead coming from Fitch Ratings, one of the big three credit ratings agencies. Bloomberg summarizes below the takeaway from Fitch’s October 2016 report, Disruptive Technology: Batteries: “Batteries have the potential to ‘tip the oil market from growth to contraction earlier than anticipated,’ according to Fitch. ‘The narrative of oil’s decline is well rehearsed -- and if it starts to play out there is a risk that capital will act long before” and in the worst case result in an ‘investor death spiral.’” (link) And despite very conservative EV projections from BP and OPEC (see below), many oil executives are aware of EV’s impacts on the sector, and are, in part, noting a decline in oil demand starting in the late 2020s or early 2030s. But note: Though there are still critics who believe the coming EV tidal wave is totally overblown. Here is a good counterpoint from the Financial Times. For a deeper dive into how oil and gas majors are increasing their investment in renewable energy, check out our other article: “Oil and gas companies’ and renewable energy: Passing fad or major trend?” Also, check out this graph that represents the 120 EV car models coming to market by 2020. All of these car manufacturers bets on EV can’t be wrong, right? (Tongue twister, I know.) 4. EV market share by 2040 varies by 13x, depending on the source As you can guess, the potential for errors increases as the length of time in the projection increases. So, how do projections for EV penetrations vary for 20 years in the future?

And how about projections for EVs as a percentage of all new car sales?

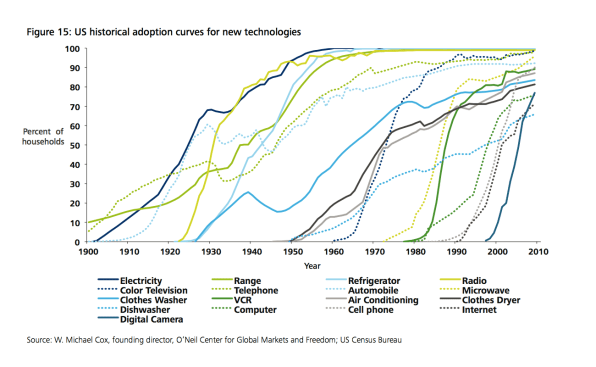

Are you confused yet? Yep, me, too. But that can be the sign of a sector that presents opportunities for above-market returns. 5. Adoption of new technologies has historically happened quicker than common sense would suggest Consider the microwave, dishwasher, cell phones, refrigerator, internet, VCRs, or computers. They are not perfect comparables to a vehicle, but suspend disbelief for just a second. These technologies often went from zero to 80%+ market penetration within about 25 years after their initial 1% market adoption (i.e., roughly where EVs are today). This graph shows these trends well. Here are some assumptions you could use to create your own simple spreadsheet:

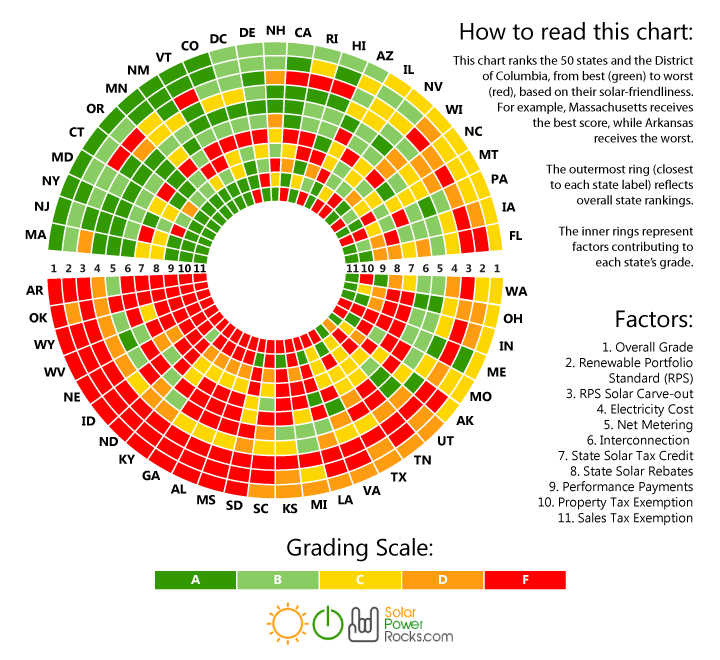

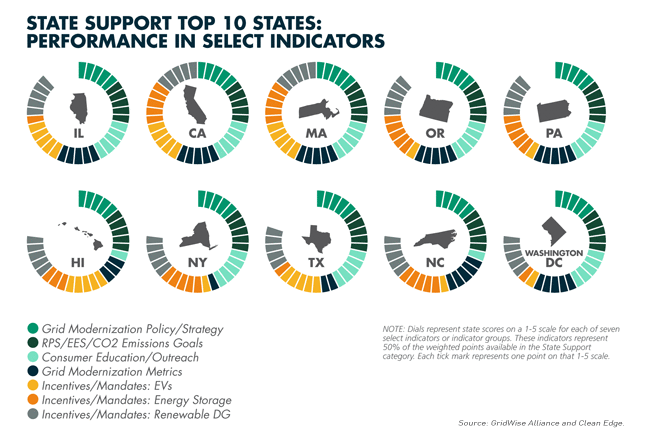

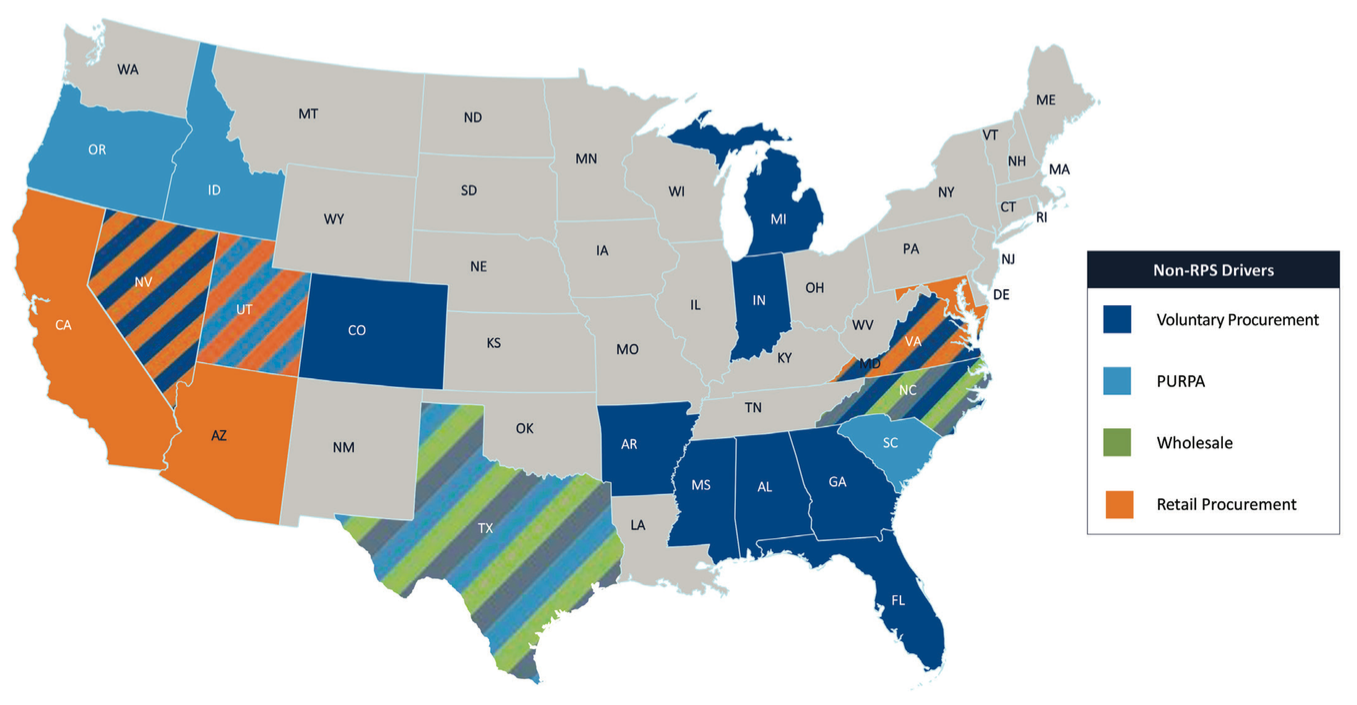

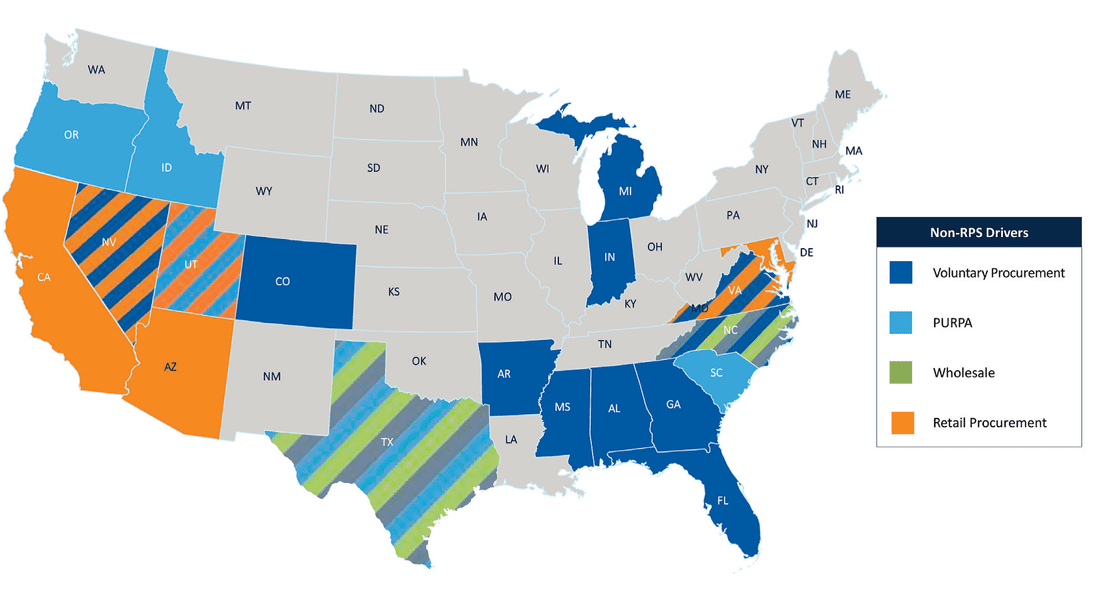

Potential results:

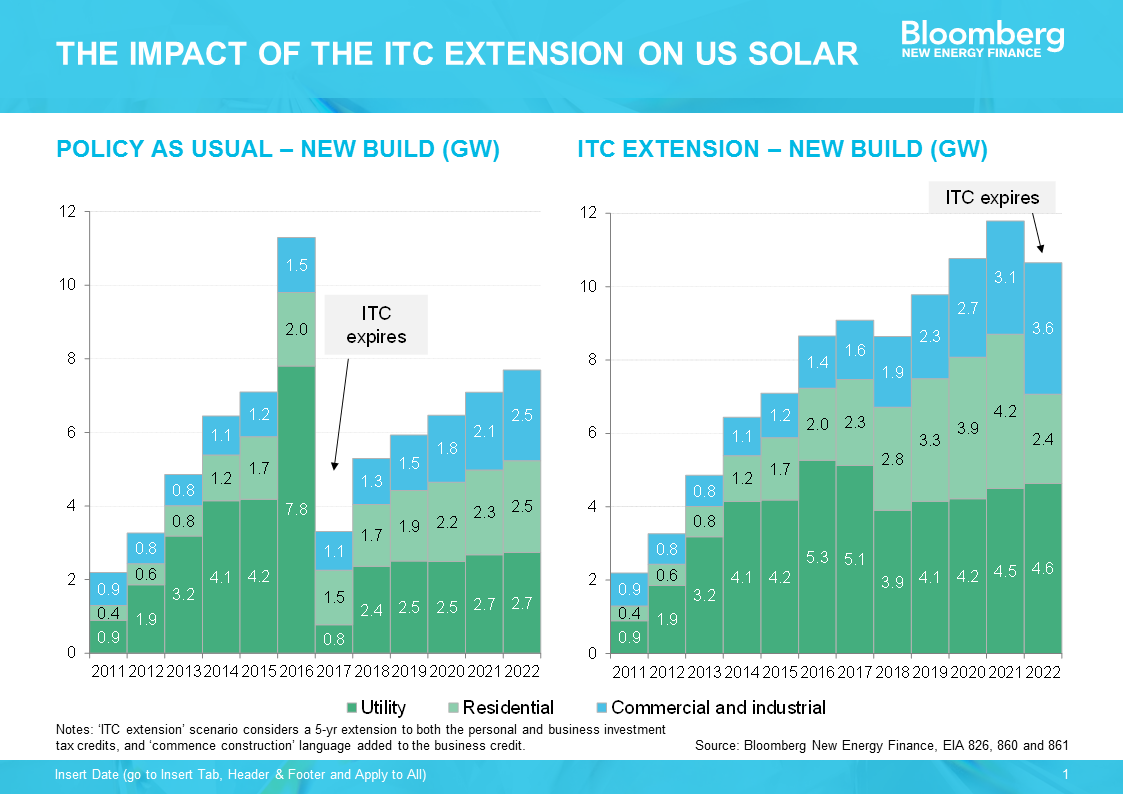

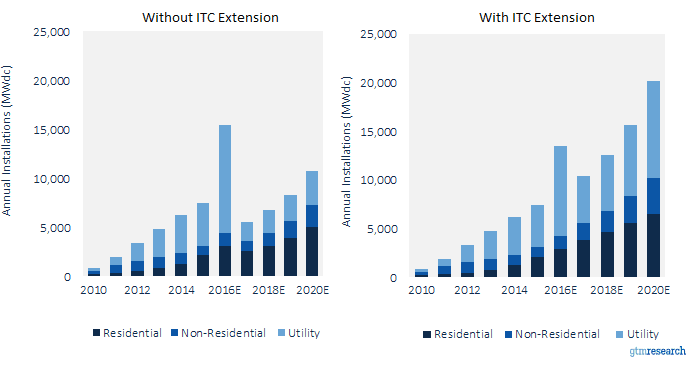

-- In conclusion When it comes to predicting the future role of EVs in the transportation or energy sector, no one is right. However, it’s a little bit like deer hunting with a bazooka. (Bear with me...I’m born and raised in the South.) It doesn’t require the precision of a bow and arrow, so odds are you’re going to be putting some free range meat in your freezer after that trip to the great outdoors. Translation: Abundant opportunities exist for entrepreneurs, large corporates, and investors in the EV market in the short and long term. As the Chairman of Bloomberg New Energy Finance noted recently, with 100+ EV models on the road within three years, EVs will make internal combustion vehicles look old fashioned. 1. Have no delusions about policy risk -- it exists, but it is not unique to the solar market It is not an uncommon stance for private equity investors to claim that they will not enter markets with “policy risk.” Being someone trained in economics, this statement comes across as somewhat strange, bordering on naive. Markets are policy constructs. There remains some secular ideal of a free market without government or policy intervention. While this may exist out in the far reaches of less formal economies, it is wholly inapplicable to electricity markers. The policy landscape defines the contours of where and what kind of solar development can take place and where capital can be deployed with the reasonable expectation that it can meet investor hurdle rates. Ignore policy at your own peril. The most enterprising investors are constantly searching for ways to anticipate markets movements largely through the lens of policy. That said, if there is anything that will put a damper on sustained investment activity, it is policy uncertainty. And that pertains to everything from state-level mandates to utility-level interconnection practices to local land use planning. While it is relatively easy to have a clear view of the state-level policy, it requires much more on-the-ground knowledge of utilities, permitting agencies, and landowners to really discern where the most productive spaces to invest are. 2. The states rights debate emerges in the electricity market It is easy to assume that the biggest energy-related issue at stake at the federal level is the Clean Power Plan. Of course, whether the CPP makes it through the Trump administration’s grinder is a matter of no small importance, but let’s just say the odds are not in its favor. It’s a shame, as the CPP was never really given a chance to shine (pun intended). There is a larger structural issue at stake concerning federal vs. state jurisdiction. States used to control most of the electricity market regulation, but has started to cede authority to FERC as the electric grid has become more regionalized, interstate electricity markets have formed, and and transmission development issues have cropped up. Yet again, the age-old story of federal vs. state rights comes to bear its head. States have lead the charge with RPS mandates, various compensation schemes for distributed resources such as RECs, implementation of PURPA, and a host of competitive policy issues. And, as any clever investor or developer knows, this has created a remarkably vibrant but fragmented investment landscape for solar in the U.S. FERC is left to argue over who is responsible for creating a coherent picture of this vast mosaic of policy approaches. Left to their own devices, states will forge ahead with their own plans and policies. But that will not necessarily suffice when trying to address regional and national resource adequacy, generation mix, and transmission concerns. Keep an eye out for more rulings on how the energy transition will be governed and regulated at the federal and state level. Especially for states that are behind the curve, so to speak, it will be really impactful on how utilities are regulated and where new emerging markets for solar development and investment emerge.  (Source: SolarPowerRocks.com) 3. Grid modernization is essential (and cool sounding), but it’s still going to be a bumpy road The New York REV program gets a lot of love, but don’t forget about California, Massachusetts, and Maryland, among others. Each is whipping up a unique secret sauce to address a docket of issues surrounding utility structures and incentives and the integration of distributed energy resources (DERs). At a high level, efforts such as these will ease the path to higher penetrations of renewables, a long-standing (and perhaps specious) contention of renewable opponents and skeptics. More importantly, these policy initiatives aim to create a more cooperative and predictable environment for developers to build projects and investors to deploy capital in the solar sector. Developers are always interested in more (low cost and patient) capital and high quality pipeline. But, increasing their Christmas wish lists include more certainty and predictability in navigating the increasingly gnarly regulatory landscape. If there is any simple heuristic for forecasting new solar markets, it is where grid modernization processes are underway. If it only were so simple. Where modernization makes developers and investors a little uneasy is how new DER compensation schemes are going to change the value of their development assets and operational projects. From a technical standpoint, it makes all the sense in the world to treat DER according to the value it contributes to the grid. By no means is this easy or straightforward, but there is some logic to doing it. But it is an entirely different matter to get investors comfortable with underwriting projects with significantly different revenue streams. Underwriting solar projects is something that the industry has become quite adept at, and there will be some reluctance in adapting to entirely new structures. If this comes to pass, and we are no longer in a solar world dominated by simple PPAs, then the most enterprising investors will need to lead the charge on how to finance these projects.  (Source: Clean Edge) 4. PURPA has been a cornerstone in the solar market, but watch out for potential attacks. The Federal Public Utility Regulatory Act, otherwise known by the attractive sounding acronym PURPA, far preceded the solar industry as we know it today. Dating back to 1978, this policy lay relatively dormant for many years before becoming a key driver of growth in small utility-scale markets in many states. North Carolina can attribute its high ranking in terms of operating solar capacity - #3 as of 2015 - in great part due to PURPA projects, also known as qualified facilities (QFs). For years, this had been perhaps the best example of a market with low policy risk because the law mandates that utilities purchase electricity from small-scale generators at (or close to) their avoided costs. Developers could count on relatively predictable PPA rates and terms for their projects, which smoothed the way for scaling development and investment quickly. Many very successful developers got their start in these markets, and many investors could deploy large amounts of capital into portfolios of essentially identical projects, thereby reducing transaction and financing costs. But recently, many utilities in many states -- here’s to you North Carolina, Montana, Utah, and Oregon, among others -- have made efforts to slow activity in the PURPA market. Before you get your hackles up, let’s pause for second to consider how woefully unprepared many utilities were for the onslaught of QF development activity once solar costs dropped low enough to have projects pencil for investors. It is not altogether unreasonable that the PURPA market be reconsidered, as it might not be serving the purpose for which it was originally intended. That said, the disruptive tactics being used by utilities to cool the PURPA market have created a contentious environment. The risk and uncertainty surrounding the future of this market has undermined years of effort and investment on the part of developers and investors.  (Source: GreenTech Media) 5. Is solar ready to wean its from the ITC? The time might be sooner than you think. Lest you thought that I was going to skip over perhaps the most important incentive in the solar industry, here are my two cents on the ITC. First of all, weren’t we just here? I recall at the end of 2015 all the consternation over whether the ITC would be extended beyond 2016. We poured over what-if scenarios like the one from BNEF below. We were all in store for a blitz to the ITC finish line at the end of 2016, and, lo and behold, Congress passed an extension just before holidays. That led to some interesting dynamics in 2016, as some solar development that was slated for 2016 ended up being pushed into the future. But, all in all, the solar industry thrived in 2016, and business-as-usual was the expectation through the early 2020s. Given the proliferation of fossil fuel industry proponents and climate skeptics entering the new administration touting the “all of the above” energy strategy as their cornerstone approach, it does call to question whether the ITC is as safe as we thought it was just a short time ago. On the one hand, the solar industry has, with notable success, achieved bipartisan support from the bluest to the reddest states. Solar job creation is an unadulteratedly positive story that few can dispute. On the other hand, there are many Republicans that would love to cut government subsidies of all kinds, regardless of the public good that they might provide. Moreover, there is some momentum behind the idea of a large tax reform, which might lead to a reconsideration of the ITC, among many other tax-related subsidies. Is the solar industry strong enough to survive without the ITC? Clearly, yes. But not everyone, and not all markets. There are many investors who would not lament the elimination of tax equity from the capital stack. But make no mistake, it would be a rude awakening to abruptly end the ITC. I would not put my money on that happening. The cost is modest and there is a sunset clause already in the policy to limit long-term government liabilities. But I cannot, in good faith, make any strong predictions, so be prepared for anything.  (Source: BNEF)

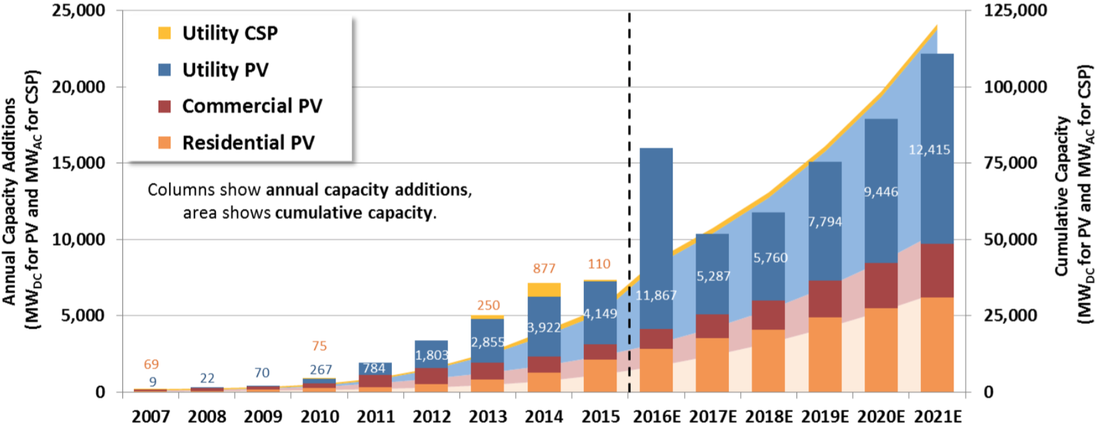

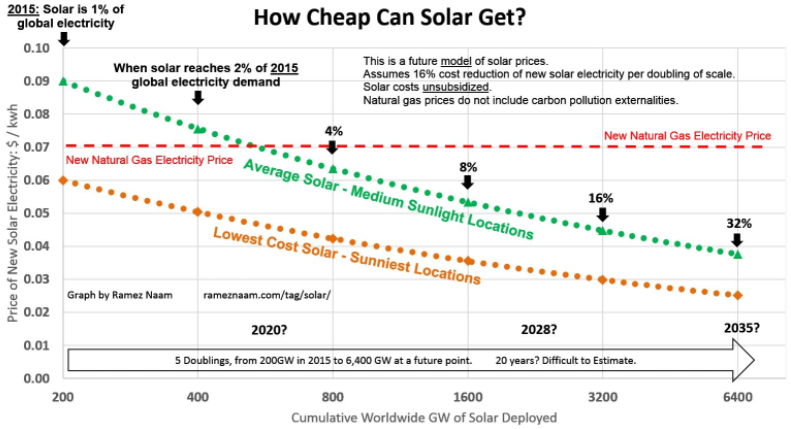

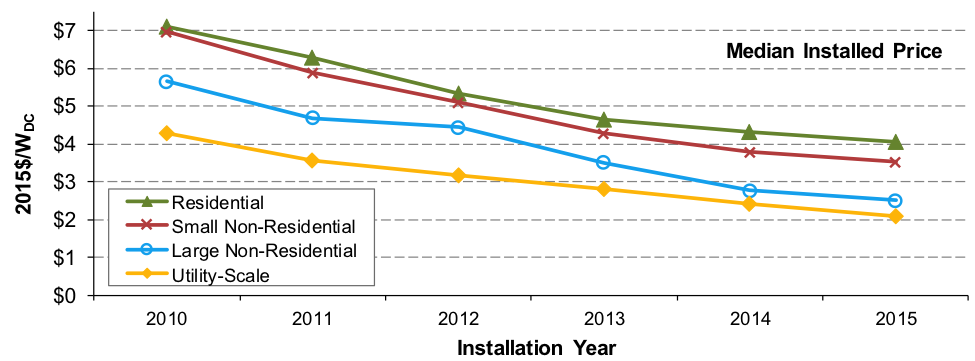

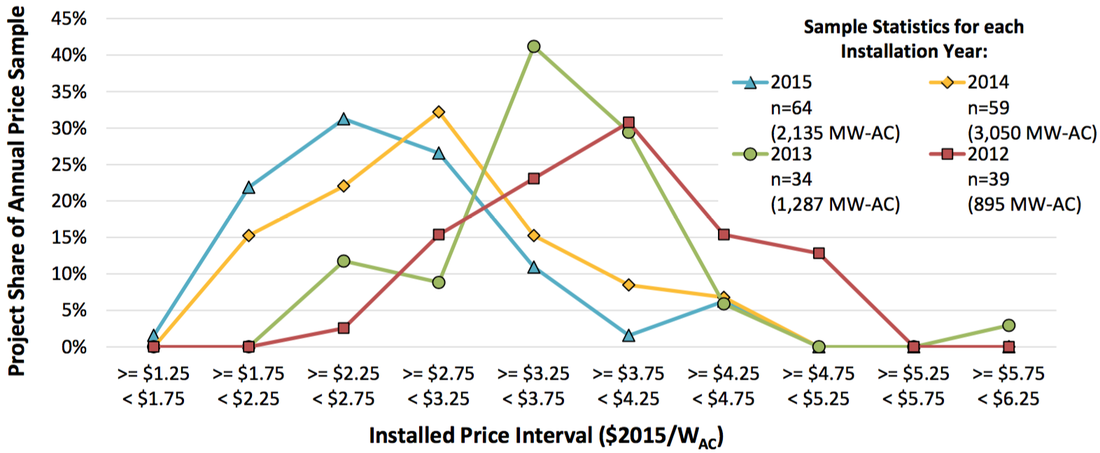

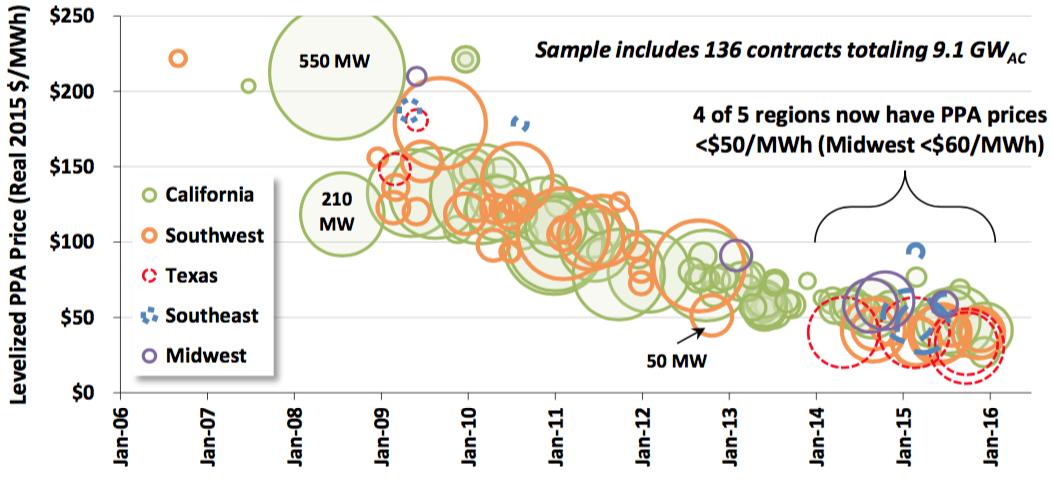

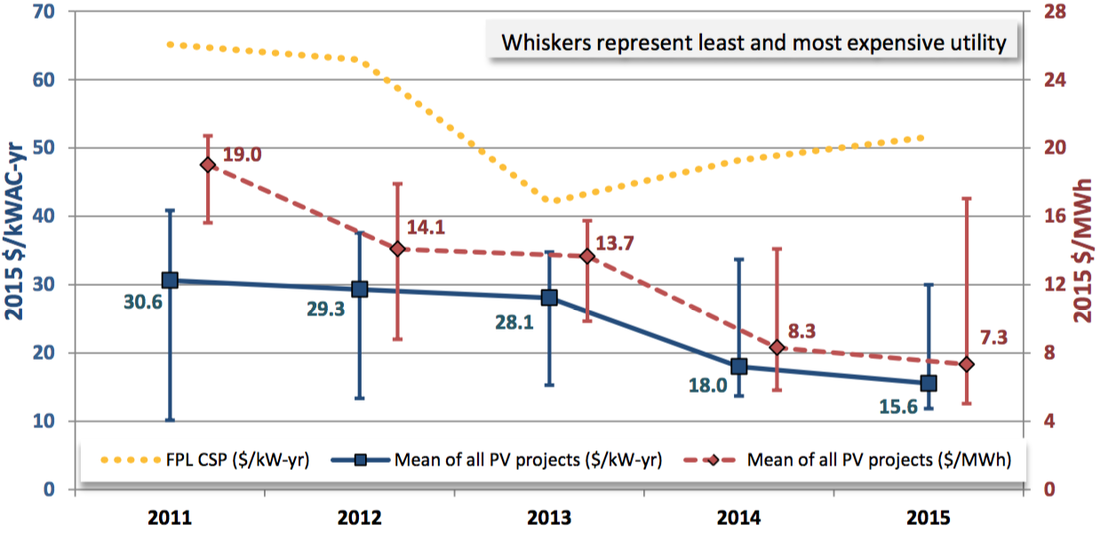

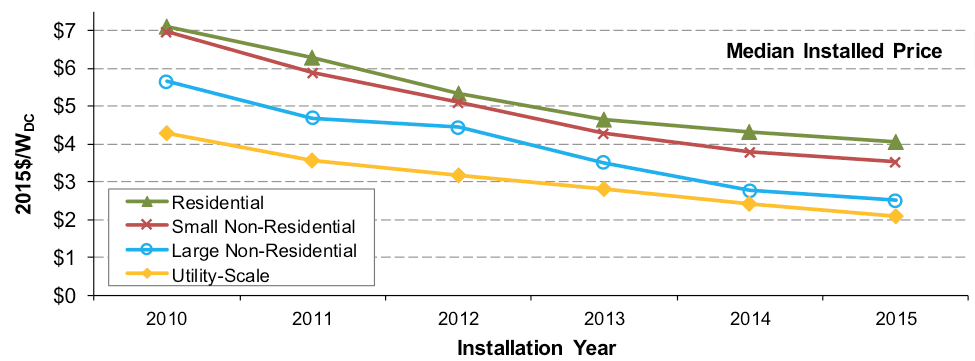

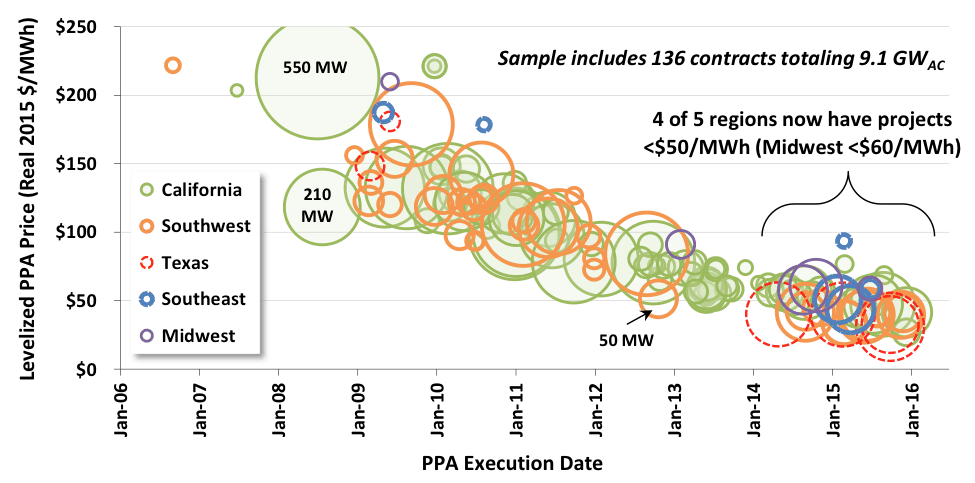

1. Growth in solar is pushing costs down the virtuous path of technological learning If you consume any media or analysis on the solar market, you have undoubtedly seen many graphs like the one below. That sweet exponential curve has driven much shift in investor attitudes about and activity in solar. It is likely a relief that you are no longer a pariah when you bring up solar at investor conferences. Solar has been one of the fastest growing sources of electricity (along with wind and natural gas) since 2010.  (Source: GTM / SEIA Solar Market Insight Reports, LBNL Database) But the real beauty in the growth of the solar market has to do with technological learning, or the predictable cost decreases that result from increasing “experience” with the technology. Most technologies exhibit the pattern displayed below. Growth in the development (or usage) of a technology unlocks a hidden treasure trove of reductions in cost, which further fuels the positive feedback loop generating more development growth. And so the march goes on. The graph below shows the reduction in the price of solar electricity, which is one measure of cost. We are going to dive into some others. The brain tickler is what the rate of cost reductions will be moving into the future. Even though solar has experienced an unexpectedly rapid reduction in costs, many predict this trend will not abate for some time.  (Source: Ramez Naam) 2. Just because solar build costs are cheapest in utility-scale does not mean that is where the best risk-adjusted returns are The undiscerning investor may jump to conclusions - utility-scale solar must be the best bang for the buck because it is the cheapest. But you would be only partially right (and sometimes mostly wrong). While utility-scale solar is now consistently being installed for less than $2.00/W, this is the market where we are seeing the lowest per kWh revenues, as utilities are getting a bit less generous with their PPA terms (more on that later). But the projects are big and relatively standardized, so the investment profile is still attractive to many investors. Commercial (here referred to as non-residential) solar is a tantalizing market in that it can present an attractive investment profile, but often with some funky (e.g., heterogeneous) risk characteristics. You can find some appealing portfolios of projects above the 500 kW threshold, but there are a whole suite of idiosyncratic risks associated with the offtaker, EPC, etc. Only the brave (and smart) are wading into vast expanse of untapped opportunity in commercial solar, and with some considerable success. Watch out for the leading actors in the space.  (Source: Scientific American) 3. Averages are useless - smart investors think in terms of distributions It is all too easy to think of solar as a monolithic industry, but that would be missing the story beneath the headlines. Distributions are the key to understanding market trends, and identifying areas ripe with opportunity. The graph below tells a story of market convergence. Most projects are achieving similar build cost performance over time. If you are presented with a project with all-in build costs above $3.00/W, then you either have a particularly challenging project, or a particularly challenged builder. Pick your poison. This convergence also means there is more a general sense of how to benchmark a project, and hold EPCs accountable to the standards being set by their peers.  (Source: LBNL) Disclaimer: the sunniest places are not necessarily the best markets for solar. That largely is a policy driven issue, which will be a topic of another post. But sun (or insolation if you want to sound clever) can be very useful. The real takeaway from understanding geographic distributions is that capacity factors (e.g., the underlying technology performance of generating electricity) places some bookends around what sort of revenues and costs a project can support to hit your hurdle rates. The Northeast needs a bunch of incentives to have projects pencil for investors. Less so the case in sunny California or the Southwest. Developers are often inclined to slightly (or aggressively) inflate the performance of their projects. This is an easy area to push back if you have the right data at your fingertips. Remember solar negotiations 101: Don’t take the developer’s project valuation at face value.  (Source: LBNL) 4. Return compression and the southern PPA migration It is often headline news when a new record low PPA rate is achieved. This is great for offtakers and utilities, but can be a source of deep consternation for investors seeking market rate returns. What is the enterprising investor to do? Utility-scale PPAs are now consistently below the $50-$60/MWh threshold, which is remarkable considering that just a decade ago, PPAs were 5x those rates. But this means that an investor that wants to compete in this market needs deep pockets and a low cost of capital. If when you look in the mirror, that is not you, then it is time for a gut check. Translation - you need to take some perceived (?) market risk. If you want to wade into a different area of the PPA pool, that means tapping to the aforementioned commercial (often referred to as C&I) market, or exploring more nascent markets such as community solar. You may be able to attract better PPAs, but they will be offset by higher per Watt build costs, O&M costs, and a different risk profile. This means a different underwriting and due diligence process that can cascade into high transaction costs for the unprepared. Choose your battles.  (Source: LBNL) 5. Don’t forget that solar projects are long-term operating assets. Investors should be riding the downward trend in OpEx to boost returns, especially on the back-end. One unmitigated piece of good news for investors is that O&M costs are also trending downward, now below $15/kW-yr. These often underappreciated components of any project cost profile are a key to unlocking longer-term value. Many investors often neglect to put the time and effort needed to manage OpEx costs to optimize returns, especially on the back-end of an asset’s lifespan. If you pay more attention in structuring asset management, O&M, insurance, and other OpEx contracts, the ROI will be, let’s just say, highly justified. O&M Costs  (Source: LBNL)

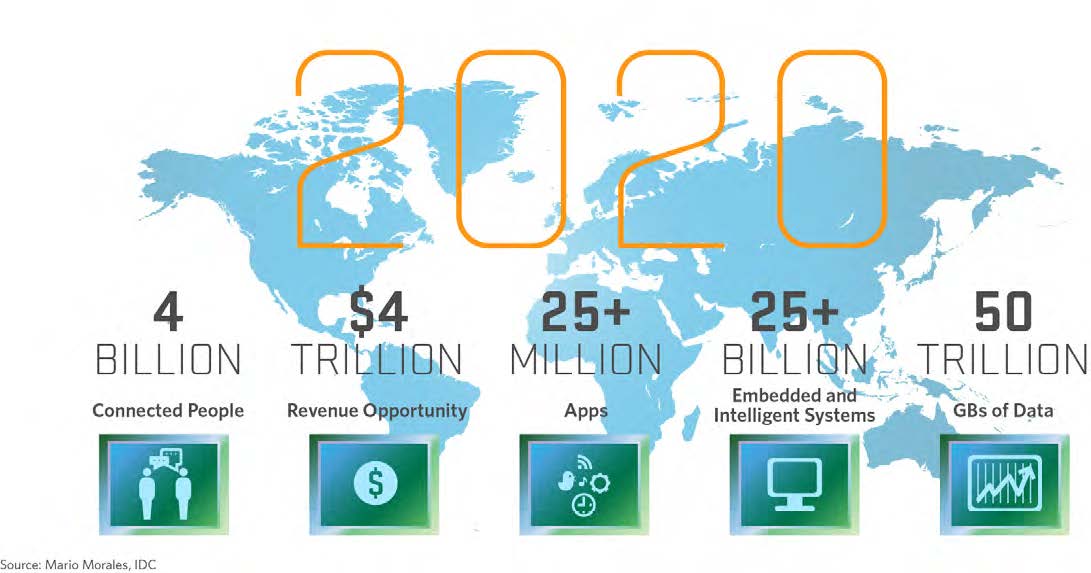

You may have heard of phrases such as “The Internet of Things” (IoT) or the “Smart Grid.” Both terms are defined differently by many people. According to IBM, the IoT refers to the “digitization of the physical world.” According to the U.S. Department of Energy, the smart grid can be defined as “a [new] class of technology to bring utility electricity delivery systems into the 21st century, using computer-based remote control and automation.” The investment opportunities in improving the intelligence of our electricity generation, transmission, and generation system can be summed up by a joke reserved only for energy geeks (like me). It goes like this: “If Thomas Edison were alive today, and you showed him a smart phone, he would be blown away by the innovation. In contrast, if you showed him how we produce and distribute electricity, he would say, ‘Oh yeah, I recognize that.’” As an example of the scale we are talking about, estimates suggest that the U.S. alone needs to invest US$2.1T by 2035 to upgrade its electrical grid and integrate the massive surge in renewable energy and the need for greater resilience. (International Energy Agency, 2016) As an example of what is coming, consider analyst predictions that the number of internet-connected devices globally will grow from approximately 13 billion in 2015 to almost 39 billion in 2020. (Juniper Research, 2015) Or consider the scale of the opportunity in the infographic below.  Source: Mario Marales, IDC Considerations for infrastructure investors:

The Chief Technology Officer of Tesla, J.B. Straubel, stated recently that it doesn’t make sense for electric vehicles to send electricity back to the grid. In the same remarks, he also noted the following:

What the CTO is criticizing — vehicle-to-grid or V2G -- is essentially distributed energy storage on wheels. The function It takes advantage of unused EV battery storage capacity to allow for power sales back to the grid, either by draining some power when the vehicles are not in use or reducing the vehicle charging rates. At a basic level, V2G has three requirements:

Vehicle-to-Grid Schematic  Source: Jim Motavalli, The Azimuth Project The EV technology and services company AC Propulsion, a V2G proponent, outlines the potential benefits of V2G as related to grid services: peak power sales, spinning reserves, base load power, peak power (either as a form of direct load control or to reduce demand charges), and reactive power.

In turn, the EV owners get paid for the energy services provided. But aren’t all of these benefits just the same as those for storage, but in EV form? The figure above seems very similar to one that would be drawn for fixed batteries. The challenges of V2GSeveral hurdles would have to be crossed in the current market and policy environment for V2G to be commercially viable. Among the not-so-attractive characteristics of V2G:

V2G Lite -- Commercial Fleet Applications The first of those challenges above could potentially be met with a market-derived refund incentive, though it is unclear how many EV owners would be willing to own a car with a shorter lifespan in exchange. Alternatively, EV battery manufacturers could design future batteries for more frequent power cycling, but that would require a major and disruptive shift from the current design parameters that do not take V2G into account. The second challenge would seem to be one of public policy, and conceivably overcome if stakeholders from the EV space were united in pushing for V2G (which they’re not). The third challenge might be addressed with commercial EV fleets. In this “V2G Lite” scenario, a fleet owner -- who with the help of data analytics has a good sense of the driving patterns of the fleet -- would be able to sign a power supply contract with a utility that guarantees a certain amount of EV battery capacity at different times during the day. Fleet contracts could be bundled, so risk is spread and utilities only have to deal with a few intermediaries when relying on this stored power source. Even if a fleet was designed to spend most of the day on the road and most of the night charging, there could still be some battery capacity free at certain times, available to be used by (and sold to) the grid. Along these lines, Nissan is notably optimistic about V2G’s horizons, and has been so since last spring when it announced cooperation on V2G efforts with Endesa, a subsidiary of the Italian energy multinational Enel. Now the automaker is working with Enel and the Californian V2G services provider Nuvve to install a commercial V2G hub in Copenhagen, Denmark. The 100 kW project is admittedly small, with 10 Enel 10 kW V2G charging units paired with 10 Nissan EV vans and a Nuvve platform to coordinate when idle vehicles can send energy back to the national grid on demand. V2G Strong -- V2G for Everyone? Or, what might be good for the public isn’t necessarily good for Tesla A group of EV researchers at the University of Delaware is at the leading edge of EV research and those advocating for full V2G penetration. In one study the numbers and justification for a full V2G push are impressive: if we put 20 million light duty V2G EVs on the road (just 10% of the current total U.S. fleet), and conservatively assume a peak power rating of 50 Kw for the cars, we could have a combined power capacity equivalent to the entire U.S. Electric grid. Paired with renewables, the V2G EV fleet would bring game-changing results for CO2 emissions and other transportation sector pollution. The EV future is being built now, with new cars, new charging stations, and new rules and practices. As this new EV built environment grows and develops, integrating V2G capabilities may just add an additional layer of complexity to the overall project, without a certain return. But if we were to make a major push for V2G capabilities to be integrated at the ground level, the benefits for society and the planet could be large. Does every solar project have to be big? Many solar investors’ intuition rests easy when they see the graph below. It fits into the elegant framework of “economies of scale.” The bigger the project, the lower unit cost of installation. The smaller the project, more cost-inefficient. Going big is part and parcel with cost efficiency, or so the saying goes.  (Source: Lawrence Berkeley National Laboratory) But be careful, this is precisely the rationale used to advocate that utility-scale solar is the only form of solar in which we, as a society, should be investing. Heck, Warren Buffett believes so, and that guy never makes a bad bet (at least publicly). Why produce electricity from projects that can be built at $4/MW on top of a house, when you can generate those same electrons from a larger project that can be built for half the cost? It is a compelling argument, I must admit. But it suffers from the same “big infrastructure” fallacy that is currently hamstringing our legacy centralized energy system. Build BIG projects for cheap on a per MW basis. Big is cheap and efficient. But, as any good economist knows, external costs can cause headaches (and asthma, skin cancer… you get my drift). Utility-scale projects have gotten a free ride See, BIG projects are cheap, in part, because they burden society with costs not borne by the projects themselves. What costs you might say -- only the never-ending litany of transmission and distribution expenditures. Billions of dollars of deferred T&D expenditures hang like a dark cloud over electric sector. And who is paying for those? Not the project owner, that is for sure. Yes, there are interconnection costs, but let’s be real, they hardly cover it. That is not to say that there is not, in fact, a significant need for big projects. But only to a certain extent. Why only build projects that necessitate that we continue to invest so heavily and T&D infrastructure? Small can be beautiful (and efficient), too. Yes, we should invest in more high voltage DC transmission. But, why not minimize the need for such costly investments by building smaller C&I and residential projects? They may be more costly on paper, but at the scale of the whole grid, they may actually be introduce some much needed cost-cutting. Thus, it is the prospect of avoided T&D costs that gives any credence to the claim that smaller-scale projects can be both both prudent and cost-efficient. Avoided costs is a common concept in utility-scale generation, but, for some reason, this logic is not applied to smaller-scale projects. It is not because they don’t make sense, it is because utilities are uncomfortable with power producers that they do not control. Investors start to take notice of smaller-scale solar Now, from the perspective of an investor looking to be a long-term project owner, things get interesting. The graph below show the slow march down the path of PPA price decline.  (Source: Lawrence Berkeley National Laboratory)

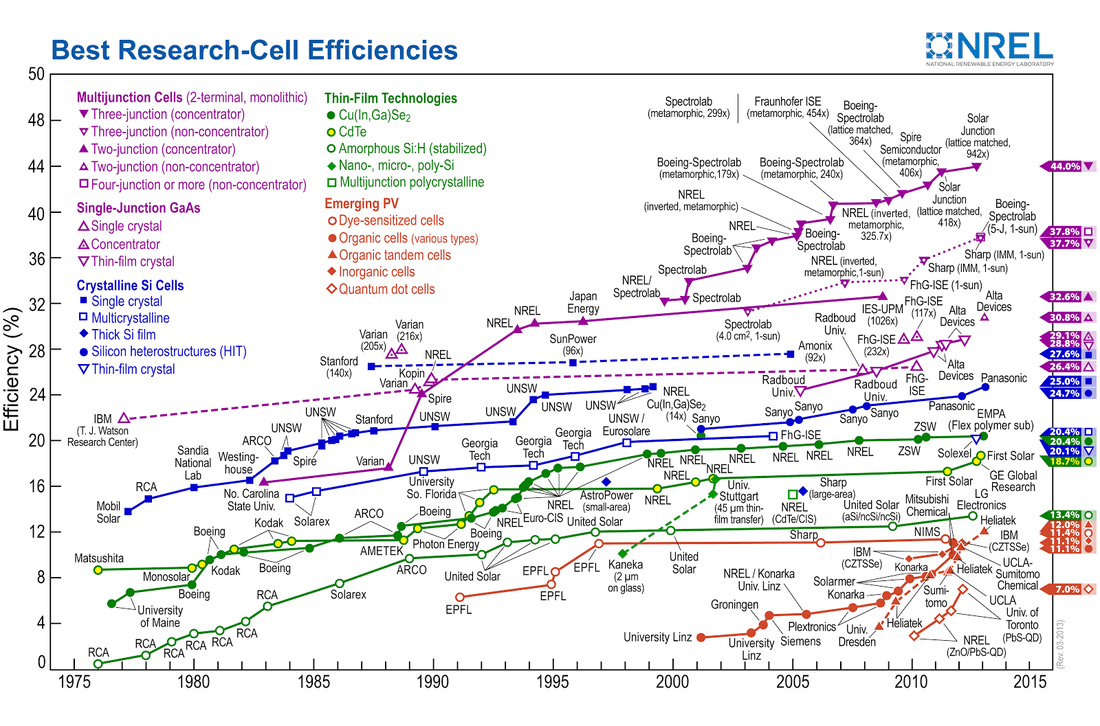

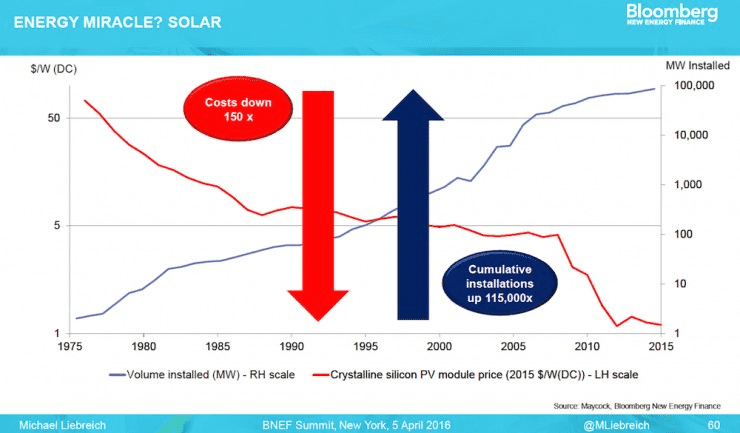

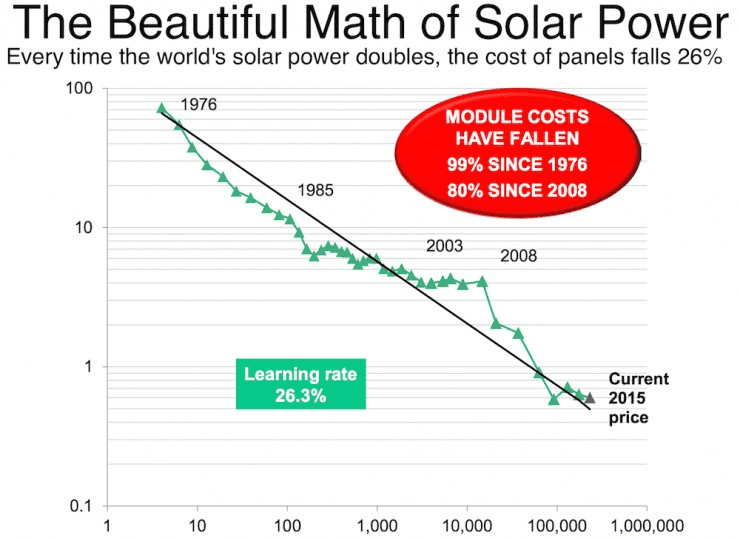

On the one hand, great - solar power is getting cheaper, and fast! On the other, there is a palpable sense that there is large-scale suppression of investors returns taking place. Fair enough. Once a market matures, actual or perceived technological risk reduces, and returns should decrease. But that does not stop investors from feeling the squeeze. And that squeeze is happening particularly in the utility-scale market. In part because utilities have a lot of negotiating power in many markets, PPA prices are plummeting, some creeping below the $0.04/kWh threshold. There is still value to be had, but the pressure to find good deals has encouraged (ahem… forced) investors to look back into the C&I market for the returns they seek. This is great from the standpoint of increasing access to capital for a market segment which historically has been more difficult to finance. Less standardized and smaller projects, diverse off-takers, many without credit ratings, and less financially robust developers have all hampered the expansion of C&I solar. But, now the suppression of utility-scale solar returns has led investors to start poking around the sleeping giant of C&I solar. Many C&I off-takers have the ability and willingness to pay much higher PPA rates than utilities. Translation = sweet returns. And, there are a LOT of them. If you are lucky enough to find them in places like Nevada where many large-scale C&I customers have been summarily pissed off by the antagonistic treatment by the utilities commission, then you could make some big waves. And, as C&I developers have become more sophisticated, projects are trending towards more consistency, bankability, and less risk. So, keep a lookout as the C&I solar market starts to find that sweet spot in the classic risk vs. return story. Small can be beautiful in the solar market. You’ve seen many headlines touting “record new solar panel efficiency.” We get excited seeing those, too. But they don’t matter. Alright, that was shock value. Let me explain. First, take a gander at the mind-numbing chart from the US National Renewable Energy Lab (NREL) below. This is one of my favorite figures in the whole world. Now, please memorize it -- there will be a quiz later. (Or so I tell my corporate and military executive students. They laugh at my false threats.) What does this figure say to you?  Three potential takeaways: 1. There are way more types of solar panels than you thought, right? 2. Solar panel efficiencies have improved considerably between 1975 and 2015. Duh. 3. The guys doing the stuff in red font should get new jobs given their low efficiency. (Not really. Those are super cheap organic polymer-based solar cells. Their future will come one day.) OK. Now forget that graph. Look at these two more important charts from Bloomberg.  Do you see any relationship between these the red and blue lines? (I hope you do.) Cost falls. Solar installations go up. And now for the next chart.  Yes, you are reading that right. A 99% drop in solar panel prices since 1976.

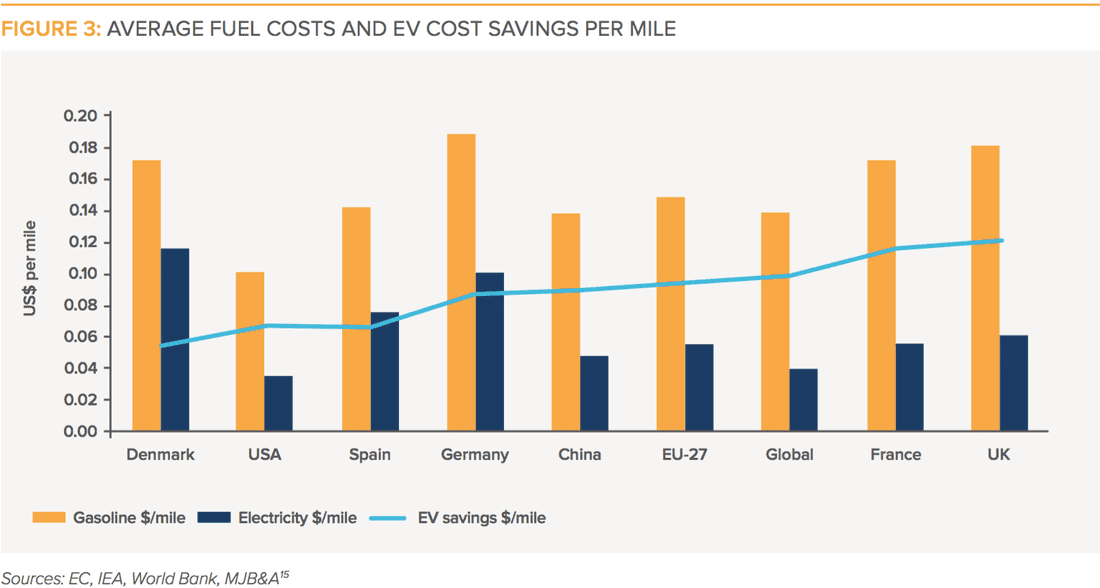

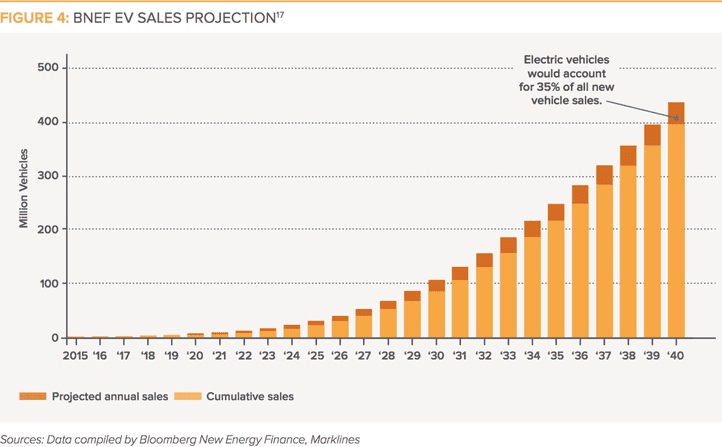

I know, I know. I hear the devil’s advocate: But doesn’t greater volume of solar installations drive down costs? Yep, but the opposite is more true. Cost drives volume. China got in the manufacturing game just as the recession of 2008 hit and EU solar demand fell off. Solar panel prices fell faster and haven’t really stopped, resulting in an 80% drop prices in the last 8 years. For more data and graphs about solar's falling costs and coming world domination (insert dramatic music), see energy rockstar Joe Romm's piece "You’ll Never Believe How Cheap New Solar Power Is." In case you fear that my ponytail is getting in the way of my PhD and love of private equity (insert humor), and that I'm being too kind to solar, consider this projection from Bloomberg: By 2040, global investment in solar will total $3.4 trillion, while fossil fuels and new nuclear will only receive $2.1 trillion and $1.1 trillion, respectively. One word: Yikes. So what? The next time you hear a sales pitch about panel efficiency, praise them for their ingenuity. They are real wizards. But just keep asking: What is the resulting $/kwh and Internal Rate of Return of the solar project? Efficiency is the finger point at the moon. Please go after the moon.  (Source: RMI Electric Vehicles as Distributed Energy Resources) Where are you, rational car buyers? The myth of the rational economic man lurks around the issue of electric vehicles (EVs). See, rationality is something to which many learned folks aspire, but it turns out to be a mirage. Yes, we stumble towards it in a thirsty stupor, dreaming of drinking up its cool, clean sensibility. But, we never get there. It always remains a misty illusion just out of reach. The rationality dilemma with EVs is pretty simple. Let’s make it clear -- EV purchasers are no more rational than EV skeptics. EV purchasers will look at the graph above, and say -- ha! -- I am saving money on a per mile basis compared to all of your fools with internal combustion engine (ICE) cars. They are not wrong, but neither are they entirely right. EV skeptics will look at the graph above and say -- ha! -- you are being duped into assuming this is an apples-to-apples comparison. Again, they are right, but that is not the whole picture, either. Why you are going to lose the “EVs are cheaper over the long haul” debateIt boils down to this. Yes, electricity is a great source of energy, and it is cheaper on a per mile basis than gasoline (even the highly subsidized gasoline that we enjoy, and abuse, in the US). But electricity is electrons, difficult to contain, eager to be used immediately. Gas is a portable, energy dense liquid fuel that affords the owner of this magical worker unsurpassed flexibility in how and when to use it. Ironically, in certain places electricity and gas are made of the same stuff -- oil. I am looking at you, Curacao and Gibraltar, where 100% of electricity is generated from oil! So the real calculation about EVs is more complex because the services that you gain from gas and electricity are not interchangeable. What value do you place on your American right to cruise the highways to your heart’s delight? If the answer is high, then the comparatively lower cost of an EV-mile is meaningless. Your peace of mind in hitting the road without a worry in the world as to how your next mile will be fueled is, in economic terms, infinite. It trumps all other concerns. The term of art for this is “range anxiety.” What value do you place on cheap, clean transportation within a relatively small driving radius? If the answer is high, then the EV vs. ICE cost comparison is how your explain to your beloved significant other why you just purchased a car that cannot comfortably drive the family to visit your in-laws. Oh, and by the way, the sticker price was a little steeper than that conventional car you had agreed to purchase. But really, the EV question is even more complicated than that And that is just the tip of the iceberg. There are many other factors -- your comfort with rapidly improving battery technology, your assumption that EV charger networks will continue to expand, your belief that manufacturers will not bail on EVs in the future, etc. -- that ultimately weigh heavily on any rational calculation justifying or dismissing the idea of purchasing an EV. Dilemmas breed a “let’s wait and see” attitude, how boring Which brings me to the last point. I grant you permission to purchase (or lease) an EV (or PHEV if just want to dip your toes). Don’t feel like you have to explain yourself to your neighbors (though this tactic will not work with your significant other). After all, why did they buy that Honda Odyssey? Was it on a purely rational, benefit-cost maximizing basis? No, they wanted something comfortable and reliable for the family, period. They just wanted it, just like you just want an EV. And let’s be real, you want it because it is cool, wave-of-the-future technology. Because it allows you to avoid ever patronizing another neerdowell, franchised Exxonmobil (or BP, or Shell, or fill-in-the-blank) gas station. Or maybe you just like getting all the best EV charger parking spots. It doesn’t matter - embrace the irrationality. Be an early(ish) adopter. Get onboard, because EVs are where we are headed, like it or not. Queue EV hockey stick graph.   (Source: GreenTech Media)

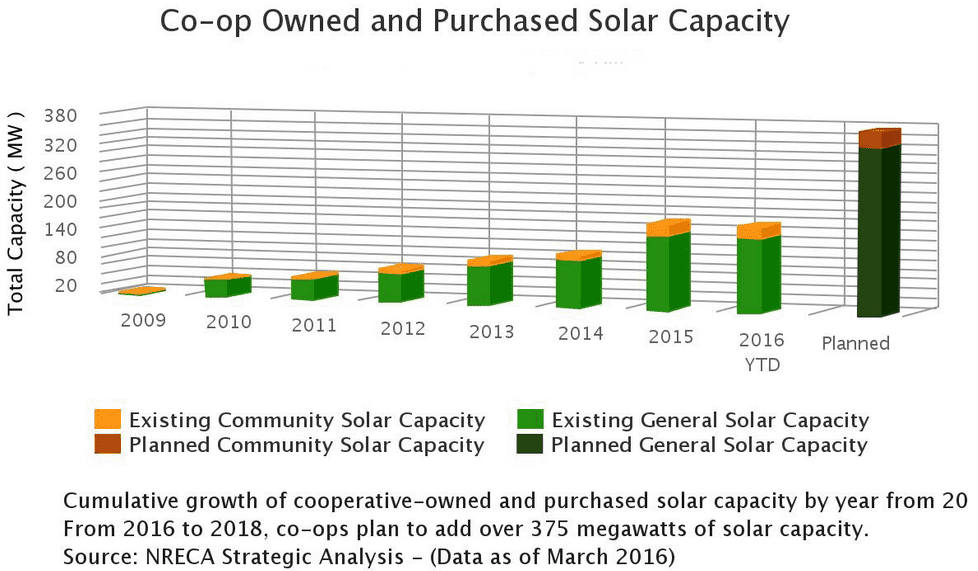

Co-ops and munis finally get a spot at the clean energy table In the energy industry, utilities have long run the show. The transition to clean energy is undercutting utilities’ historical dominance of how electricity generation, transmission, and distribution occurs. Distribution cooperatives and small municipal utilities have long ridden on the shoulders of these giants, working through contracts that typically stipulate that they must purchase nearly all of their electricity from generation and transmission (G&T) providers. In most contracts, a whopping 5% has been the limit placed on their self-generation, rendering these smaller players [almost] powerless in determining their own energy future. There is some poetic justice in having the small folks granted a spot at the distributed clean energy table. As electric cooperatives and municipal utilities were severely handicapped in their ability to procure their own electricity, they have only dabbled in contracts with independent power producers (IPPs) and other clean energy generators. This came to a head with probably the most unsuspecting sounding cooperative you could think of, the Delta-Montrose Electric Authority (DMEA). As a member-owned, rural electric cooperative based out of southwest Colorado, it is not hard to imagine that the time would come when they would want to be afforded the right to procure their electricity from whoever they please. In an act of magnanimity that perhaps surprised many, the Federal Energy Regulatory Commission (FERC) ruled in favor of DMEA in their case against Tri-State, another cooperative that provides generation and transmission services to 44 distribution co-ops across five states. In short, the ruling lifted the limit on DMEA’s ability to procure electricity from renewable qualified facilities (QFs). The loophole, of sorts, lies in the fact that the Public Utility Regulatory Policies Act of 1978 mandates that utilities must purchase electricity from QF projects. The de facto interpretation of PURPA, for oh the last 38 years, has been that larger-scale utilities and G&T providers would be sole purchaser of electricity from QF projects. DMEA, in a moment of true inspiration, said “to hell with that,” and managed to supersede their contract with Tri-State by asserting that they are themselves a utility, and should be afforded the same rights. This move did not ingratiate DMEA to Tri-State, to say the least, and Tri-State attempted to impose an exit fee on DMEA, which FERC summarily rejected. Message received. Renewables on the grid will no longer be a unilateral decision. Co-ops & Community Solar = Match Made in Heaven It is not hyperbole to claim that this is a game-changer for the nation’s 905 electric co-ops and 835 municipal utilities who woke up following this FERC ruling to a new world of opportunity. How fitting. Co-ops and munis were probably on the leading edge of support for renewables, and now they have license to act on their values, rather than be subjected to energy procurement decisions out of their influence. And that is a very good thing. In fact, it is 987 TWh/yr of a good thing, which if you do the math, implies that the potential market for co-op/muni renewables approaches 400 GW. Many co-ops and other smaller utilities are structured in ways that are much more conducive to serving the public good. Often they are publicly or member-owned, or at the very least not publicly traded, which makes them more intimately connected to their customers and ratepayers than the larger utilities and G&T providers that dominate much of the electric power procurement space. Moreover, they are more likely the engage in novel project types like community solar. There is some cosmic symmetry in enabling co-ops/munis to sponsor community solar projects. It makes so much sense. It seems ludicrous that this was ever challenging to execute at a meaningful scale for many co-ops. According to RMI, the market for community-scale solar projects ranging between 500 kW and 5 MW of capacity each could exceed 10 GW by 2020. Wake-up Call for the Generation and Transmission Providers An ancillary benefit of this new arrangement is that community solar projects may now be easily integrated into the local distribution system, therein avoiding many costly infrastructure upgrades. Translation: electric distribution co-ops/munis may be able to purchase power directly from QF projects at a lower cost than what they are currently charged by their G&T providers. Memo to G&T providers. This also means that they will be reducing their reliance on your services and undercutting your revenues, unless you can evolve together into helping to co-create a clean energy future. Now, there are limits to be sure. Electric distribution co-ops/munis have only been afforded the right to negotiate PPAs (and not just based on avoided costs, as in the past) with QF projects in their territory. Not a bad deal, but it does not make them an autonomous entity. Co-ops/munis still have to balance their energy supply, which can only be done through grid management in the transmission and generation system. So, there may be some building tension in the marriage between electric distribution co-ops and their larger G&T brethren. No one wants to see the G&T providers go extinct. In fact, they are still a critical species in the electric grid ecosystem. But, the challenge will be in better collaborating and coordinating with their member co-op/muni friends. This is not a reach. And there is no better time than now. Look for inspiration? Well, look no further than RMI’s Shine Initiative, an innovative program aimed at helping accelerate solar procurement in the community-scale market. Which ducks do you see?The California Independent System Operator (CAISO) can be commended for providing an accessible daily data dump on renewable usage across its system. With these data one can construct various “duck curves” for the grid’s daily net load profile, the shapes of which result from the rising penetration of a variable energy resources (VER) such as wind or solar. VERs exhibit four characteristics:

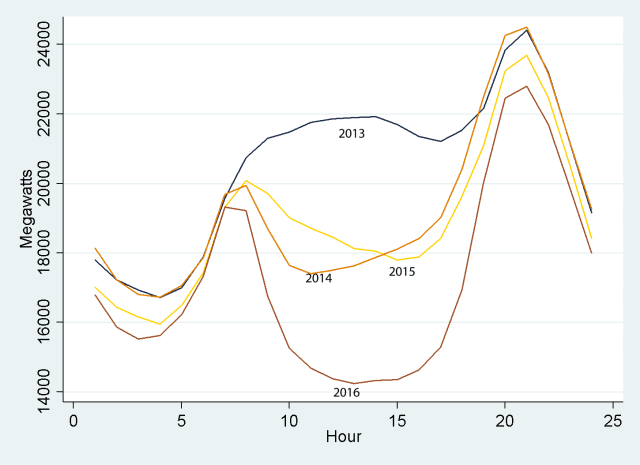

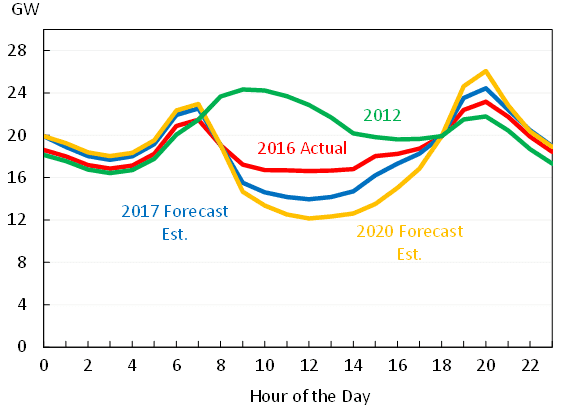

Duck curves are in essence the daily net load profiles after accounting for VER generation. They show the required remaining dispatchable energy required to ramp up or down to take up the solar and wind shortfall. As we see from the two examples below, duck curves can take on various forms, often depending on the scale range of the y-axis. 1st flock of ducks: Average net load profiles over seven days around March 31, over 2013-16.  Source: Blog post by Meredith Fowlie, “The Duck Has Landed” (5/2/16), using CAISO data. 2nd flock of ducks: Net load profiles for March 31 for 2012 and 2016. Forecasts for 2017 and 2020 were made in 2013.  Source: Council of Economic Advisors, The White House, “Incorporating Renewables into the Electric Grid: Expanding Opportunities for Smart Markets and Energy Storage,” Fig., 4 (June, 2016), using CAISO data.

Both sets of curves cover almost exactly the same sets of data, with the first emphasizing a more extreme story. The the stories are essentially the same -- net load after VERs bottoms during the day when solar is peaking, ramps up very quickly as solar generation drops off dramatically and evening usage rises, and then drops again as nighttime usage drops and wind picks up. The takeaways are two:

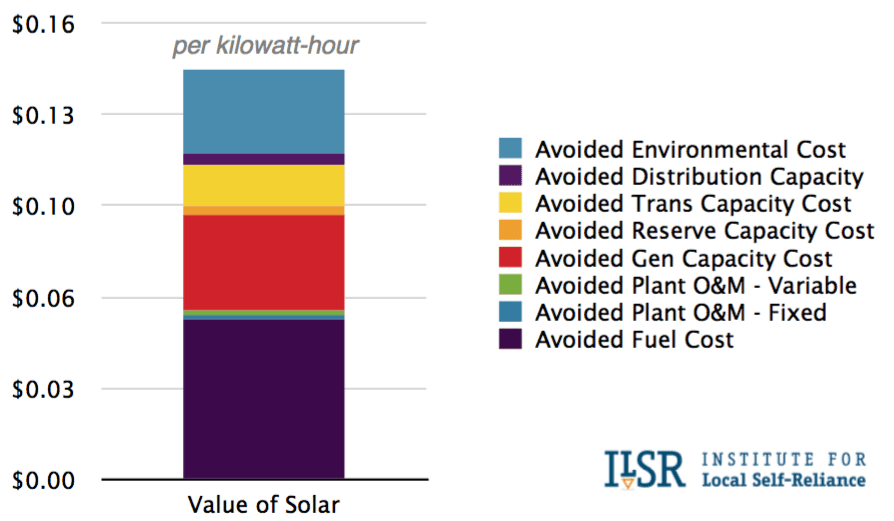

Ancillary services as regulation mileage A recent report from the Council of Economic Advisors at the White House goes deeper, looking at some ways of understanding the value of energy storage via the idea of regulation mileage. The concept measures the changes -- increases or decreases -- in power output that a grid operator requests from an electricity generation resource over a specific timeframe. It would stand to reason that regulation mileage, a proxy for the amount of ancillary services required, would be determined by several factors. The Council’s study looks at the total load, the amount of that load from VERs, the slopes of each of those load curves, and a series of effects that are specific to the hour of the day, day of the week, and week of the year that the electricity is generated. Among other results, and as expected, one of the clearest that appears is that the slopes of the load and VER generation have a lot to do with the services required. In other words, the faster the late-afternoon ramp up at the end of a sunny day, the more energy storage will be wanted. Valuing storage based on its ancillary benefits What are other approaches to valuing energy storage in these settings? The peer-reviewed journal Nature Energy recently carried the results of a new study on capturing the full benefits of energy storage in investments. Applying a techno-economic model, the authors of ”Limiting the public cost of stationary battery deployment by combining applications,” find that battery storage becomes more attractive as an investment as each storage facility offers more energy services. An article summary carries the message that energy storage apart from pumped hydro is, “still considered unattractive by investors on mainly two grounds: cost-competitiveness with other technologies and the absence of a commonly shared classification of electrical storage as a competitive or regulated activity -- that is, as an electricity generation asset or network component” (emphasis added). The drawn conclusions are that the best way to incorporate all of these benefits are to remove non-market barriers, a legacy of rules that were originally written for conventional generators. According to the summary, these “institutional and regulatory frameworks are key elements in the determination of the economic value of storage,” and “economic principles require new, enabling rules to be technology neutral, that is, not directed at the diffusion of storage or any other technology in particular.” The article calls for three such policy recommendations: