|

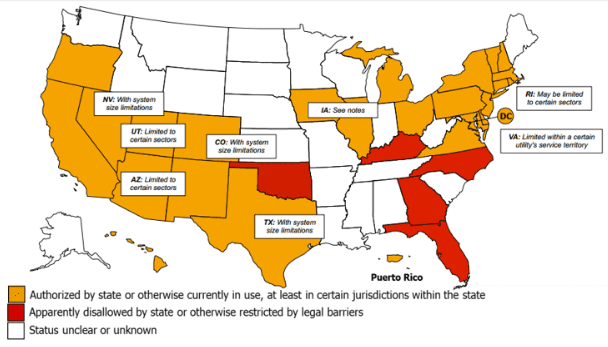

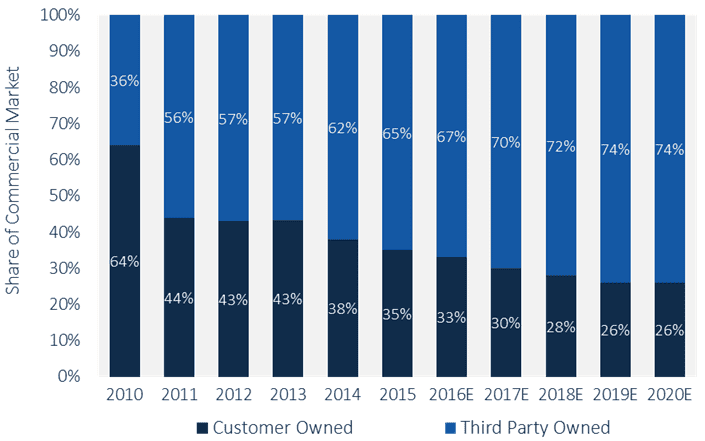

States Authorizing 3rd Party Power Purchase Agreements  (Source: DSIRE) First, the bad news: policy battles over 3rd party ownership of solar muddy the waters Just pile it on top of the other cadre of unenlightened policies that North Carolina is behind these days. Yes, North Carolina, my home state, is making headlines for another boneheaded public policy move, this time regarding the highly controversial topic of… solar! The NC Utility Commission (NCUC) recently upheld a law that prevents 3rd party ownership of solar projects. The case that brought the issue into the public limelight concerned a whopping 5.25 kW installation that the environmental advocacy group NC WARN had built to provide electricity to a local church. The two parties signed a 3-year PPA at a discounted rate, which, doing some quick math, might have provided around 23,000 kWh per year valued at around $4,000 or so for the life of the PPA based on prevailing rates. Well, Duke Energy was not having it! The biggest utility in the nation, valued at over $55 billion, opposed NCUC and beat down this encroachment on their business. And just to make an example out of NC WARN, they were slapped a $60,000 fine, which is around 15x more than the electricity that would have been sold in the PPA arrangement. Duke Energy is not entirely foolish to help combat the proliferation of 3rd party ownership, but their choice to do so goes against the countervailing inertia moving us into a more distributed energy future. Duke Energy will surely be fighting an uphill battle on this issues for years to come. North Carolina is not alone in this business of prohibiting 3rd party ownership of solar projects. The state stands in solidarity with Florida, Kentucky, and Oklahoma, which sounds like a NCAA Final Four (pause for sad memories of UNC’s recent loss). Unfortunately, that is where the commonalities stop, because, in the case of solar, competition (in this case with incumbent utilities) is prohibited. The game is rigged in favor of utilities with virtual, if not actual, monopoly power, something that supposedly goes against federal trust law. As a North Carolinian, it is with deep regret that I admit that South Carolina (!) recently passed legislation to allow for 3rd party ownership of solar projects. Georgia has done the same (although not accounted for in the map above). So, take heed, NCUC, your neighbors to the south are upstaging you on the transition to clean energy. Well done. Just add it to the list... On a positive note, 3rd party ownership trends are helping to unlock potential in the behind-the-meter corporate solar market Commercial PV Installations by Ownership Structure  (Source: GreenTech Media)

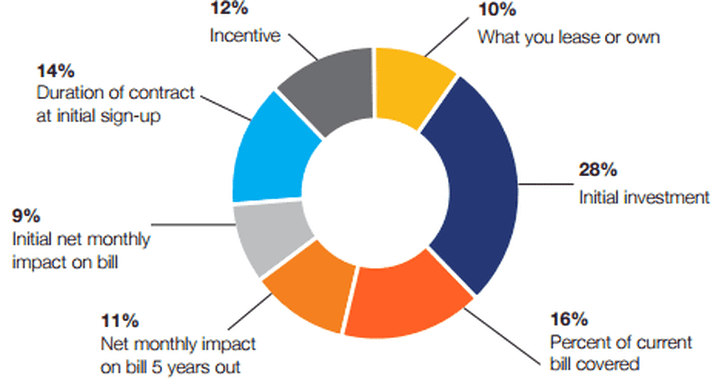

With all of the pushback on 3rd party ownership of solar in certain states, one has to consider what might happen if this was allowed. Well, one thing is for certain - corporations would be buying into solar, and likely in a big way. This is, after all, the situation that we see in states that allow 3rd parties to sell electricity from solar projects to corporations. As solar has become more competitive with prevailing retail electricity rates, corporations have started to see locking in stable electricity prices from solar as a complete OpEx no-brainer. Though a handful of corporations opt for the direct ownership and financing approach, the vast majority are seeking 3rd party owners to provide them with solar solutions. And those trends are expected to continue, as shown in the projections above. I go into further detail on this topic in a previous blog. So, what is to like and dislike about this arrangement? One the one hand, 3rd party ownership does fundamentally decentralize the electricity provision business, especially as behind-the-meter applications become more reliable and cost-effective. That is seen as a threat to incumbent utilities who have historically been the end-all-be-all of power provision. Setting aside utility concerns for revenue loss, the real question is whether utilities can meet the needs of large offtakers looking for distributed power solutions. The answer is yes and no, depending on the utility. It seems like 3rd party solar ownership is here to stay, so what’s the catch? This gap in the market opened the door for an explosion of independent power producers, offering a staggering array of behind-the-meter solutions to customers. Some of these we have come to know well - SolarCity, SunRun, Vivint, etc. But there are many others vying for a place near the top of the pecking order. So, what of the risk of working with these solar companies? It really boils down to counterparty risk. Two parties really have to believe that each other will continue to exist as solvent enterprises for decades to come. Not a trivial proposition from the standpoint of a corporation analyzing the evolution of the solar industry, perhaps for the first time. Clearly, the ongoing tumult of the growing solar industry (aaahh SunEdison chuuu) brings to light the sometimes ugly process of picking winners and losers. It would not be unreasonable to assume that the landscape of solar companies out there will continue to change for some years to come. So, why should you sign a decades-long PPA with a company that may not continue to exist for the next five years? That is the question of the moment. But if the data are any indication, corporations are becoming increasingly comfortable with signing long-term PPAs with 3rd party solar power producers, not to mention homeowners. So, back to the original story, what are the NCUC and Duke Energy, in a classic “tail wagging the dog” relationship, so worried about? It might be the “adapt or die” mantra that has been reverberating around the industry since the collapse of several European utility titans. But rather than adapting, they are digging in their heels on an issue that 46 other states in the U.S. have already come to an agreement on. If there is anything that we can agree about the future, it is that change will be ever present. 4/30/2016 It’s the offtaker, stupid! What we should have known from the start about community solarRead Now What’s new? As many have predicted, community solar continues its nationwide growth. We previously discussed the fourteen states that have adopted specific enabling legislation for community solar. With the growth in business potential, more and more states are working to adopt or revise policies to accommodate this new model for distributed energy generation. According to the NC Clean Technology Center, in Q1 2016, seven states have considered, amended or clarified rules governing community solar programs; and in states that are slow to respond, utilities are taking the lead, submitting proposals for community solar programs without a specific enabling legislative framework in place. According to SEPA’s recently released report, “Community Solar: Program Design Models,” there were 68 active programs in 23 states in the summer of 2015, with many more programs being planned. Geographic Distribution of Community Solar Projects  (Source: SEPA) In New York, EnterSolar started construction of the first community solar project in the state. Relatively small in terms of capacity (less than 1 MW), the project is developed under New York’s first phase for community solar development that limits development to areas with the highest grid locational benefits and to low-income communities. This month New York enters the second phase of the program that allows for full implementation of net metered community solar projects across the state. Many developers are already working hard to secure development contracts, and even the city of New York has introduced a municipal plan to promote community solar developments within city neighborhoods. What’s wrong? Nothing is wrong with community solar. On the contrary, we think that community solar is awesome. However, despite its great potential to unlock solar energy to more than half of electric consumers in the U.S., and although it is gaining traction nationwide, development rates for community solar are nevertheless 20% lower than expected. Even in states that have addressed management structure and regulatory uncertainty concerns projects are still not springing up as one would have expected. So what is it? Why aren’t we seeing more community solar projects? It’s the offtaker, stupid! The reality on the ground is that developers and utilities are still struggling with selling community solar to customers. Relatively complex in structure and less known than other models of distributed solar generation, community solar is a hard sale. Customers are wary of entering into unfamiliar financial adventures involving multiple parties, especially when the transaction involves an upfront investment as is the case with most community solar schemes. Part of the challenge lies with the fact that customer attitudes to community solar vary. While some programs are fully subscribed and thriving, others are underachieving. Many have tried to identify the winning set of program features that makes a community solar project appealing, but because regulatory frameworks, transaction structure, and management schemes vary greatly from one project to another, identifying best practices from existing projects has proved to be an elusive task. However, a recent study conducted by Pacific Consulting Group, might have finally revealed the answer to the question of what makes a community solar project successful. Taking a creative approach to solving a persistent problem, PCG focused on customers instead of projects. PCG conducted a market survey among potential offtakers in eight community solar states, asking respondents questions aimed at identifying how market acceptance of community solar changes with project features. Unsurprisingly, the number one factor in customer acceptance is initial investment; projects that do not include an initial investment or require only a small upfront investment are highly valued. The second is percentage of electricity bill to be covered by the investment; the lower the percentage of the bill covered, the less attractive is the project. Together, the two attributes account for 20% of total importance. Other interesting findings are that customers value savings five years out as more important than immediate savings (suggesting that customers are not intimidated by the long-term commitment associated with community solar), customers are largely indifferent to what they lease or own, and are not persuaded by incentives other than the potential payback (e.g., late fee forgiveness). Relative Importance of Seven Program Attribute on the Decision to Adopt Community Solar  (Sources: PCG; SEPA)

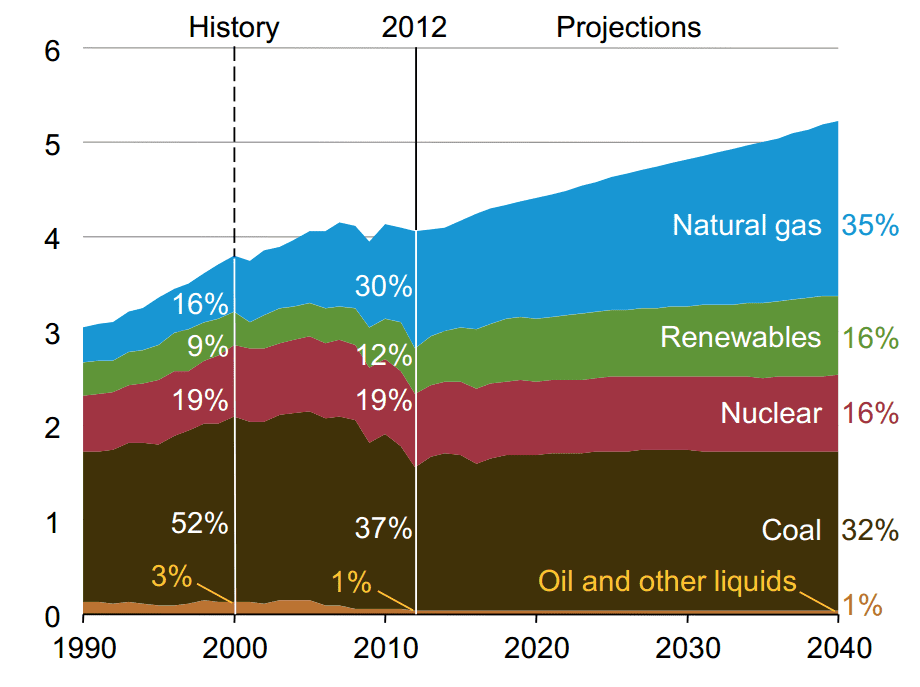

The study also measured customer responsiveness to marketing approaches and revealed interesting trends among communities. The most important findings are that messages emphasizing customer ownership and individual economic gains resonate better than messages emphasizing conservation or “green” considerations. Utilities, nonprofits, and solar organizations enjoy better credibility and therefore have better prospects in influencing potential customers than other entities or individuals (indicating the value of business partnerships). Also, personal messages targeting individual customers are more effective than mass media (with a message on the utility bill being the most effective form of customer engagement). All I want is peace of mind Understanding how to approach customers and how to tailor transactions in a manner that is appealing to potential offtakers is very important for the continued growth of community solar, but it is not enough. Even after we have addressed project features, payout structure, and marketing strategies, we still need to find an entity that will manage the project once it is operational, and long-term management of multi-party endeavors is costly. Some states have tried to address this concern by introducing an intermediary special purpose entity responsible for aggregating membership interests and managing the relationship with the local utility. But the question of cost and management remained largely unanswered, at least until now. Responding to market needs, community solar management firms are emerging. Firms like Clean Energy Collective offer management platforms that ease operations, reduce costs, and give offtakers, investors, and utilities exactly what they need - peace of mind. If you were to form your opinions on renewable energy from Energy Information Agency (EIA) reports and datasets, you might be under the illusion that we are reaching a peak in distributed solar and wind development, among other non-hydro renewables. For those less familiar, EIA provides a robust dataset of energy consumption and costs going back to 1960 in many cases, which they supplement with forward-looking projections to 2040 in their Annual Energy Outlook. Though they are considered a non-partisan research branch of the U.S. government, their data seems to represent a particularly pessimistic, and at times downright false, perspective on what is happening with renewable energy development.  (Source: Cleantechnica)

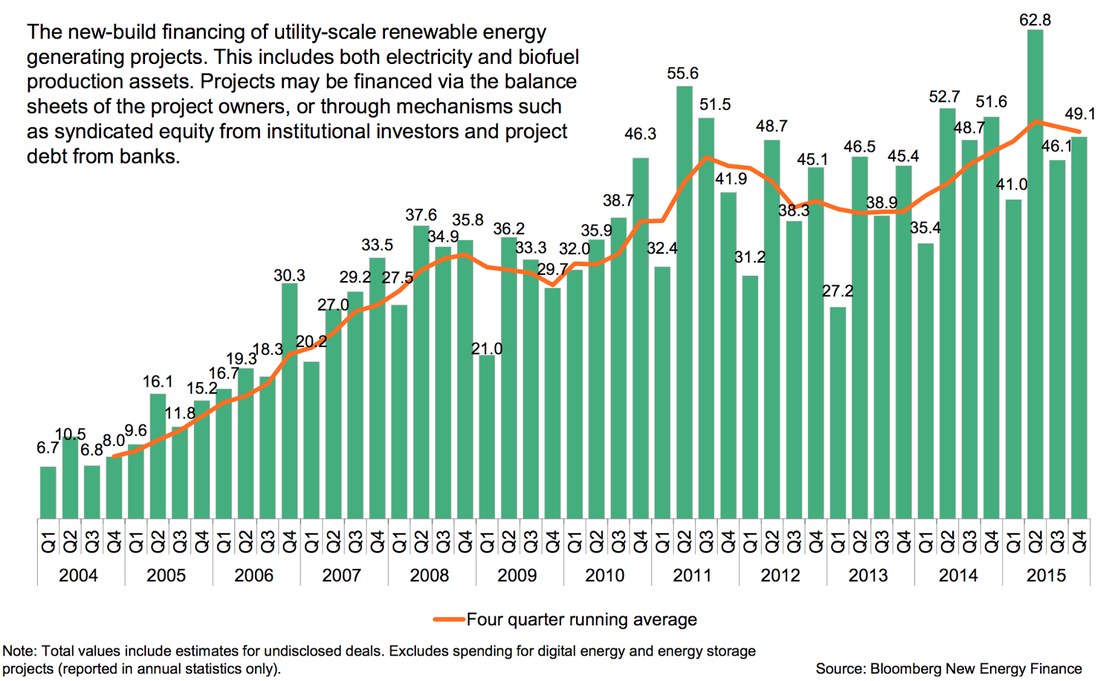

EIA bearish on renewables, despite reality on the ground Digging into the numbers, the EIA forecasts a bleak period of next to no growth in non-hydro renewables until nearly 2030. In fact, projections to 2040 have renewables at only 16% of the U.S. energy portfolio (currently at 12%), while natural gas continues to grow and even coal only decreases marginally. So, for the next 24 years, the EIA would have us believe that we should get prepared for...very incremental shifts from the present day status quo. Not nearly the renewable energy transition that we would hope for. Now, on the one hand, the U.S. electricity generation stock is absolutely massive, and the inertial pull of path dependency and legacy infrastructure investments will anchor the electric grid for decades to come. This general sentiment likely colors the views of the EIA. But the plain fact of the matter is that this supposition is being undermined left and right by the remarkable growth in distributed generation development, growth that has been consistently, bordering on intentionally, dismissed in the EIA’s future projections. EIA bullish on coal, again despite reality on the ground Why does the EIA remain bullish on coal, an industry that is undergoing a massive contraction with few new plants scheduled to come on line and many more being taken off? On the other side of the coin, why does the EIA remain so tepid about acknowledging the clear shift in the energy market towards cheap, clean distributed energy? The answer is anyone’s speculation, and there has been a long-running and healthy debate captured nicely here. Many concerns revolve around the lagged cost and price information that the EIA promulgates, which perhaps indicates the workings of a slow government bureaucracy. But is that really an excuse, when there are abundant publicly available datasets that detail distributed energy development and economics from the ground up? More important than diagnosing this systemic bias is the fact that EIA projections are used to inform U.S. government policy. Many are working to combat the anchoring effect of EIA (see here and here), and there is growing awareness that the EIA does not have the final word on what is happening in the dynamic energy industry. Forecasting the future of energy may be a fool’s errand, but let’s hold EIA to a higher standard Energy forecasts are as plentiful as they are wrong. It is not surprising that the EIA, like many other agencies and research groups gazing into our energy future, has not hit the mark on their forecasts. What is more worrying is that even their data on our current energy system is misrepresentative of the reality on the ground. At risk of being a bit blasphemous, let’s suppose that scientists are not always objective, which if you assume is the case with the EIA, then you have to start wondering what is the agenda behind presenting such a skewed picture in their datasets and reports. Perhaps it is benign neglect of the changing energy landscape beneath their feet, or maybe it is that the movement towards distributed renewables poses more of a threat to the status quo than many believe. Fortunately, there is some evidence that the EIA may finally be ready to come clean (pun intended) on their energy forecasts, but until they do let us continue to cast a skeptical eye on what the EIA has to say about the transition to renewable energy. Institutional investors have been reluctant to invest in solar, until now Perceived risks have long dissuaded institutional investors from venturing too deep into solar investments. Fortunately, perceptions can change. Whereas once the solar industry was hampered by the perception that technology was risky, markets were untested, and policy uncertain, now the solar industry is increasingly seen as a low-risk infrastructure investment that is increasingly enticing for the less risk tolerant institutional investors out there. Asset Financing for New-Build Renewable Energy Assets ($B)  To be sure, the solar investment space is pulling in interest from institutional investors, but it is also being pushed out of many fixed income and treasury investments due to the extended period of low interest rates.

Now that those “risk-free” assets are now also return-free, investors are anxious to explore investments with stable and predictable yields, ideally that generate free cash flows. As solar performs more like an infrastructure investment, with contracted cash flows, predictable technology, and a very long runway of future demand, interest from institutional investors is piquing. The question is - can solar meet the scale and risk-return profiles that institutional investors require? Can clean energy projects match the capital and risk profiles to entice investment? There are many ways that institutional investors may want to increase their allocation in clean energy - green bonds, low-carbon investment funds, etc. — but here I am going to focus on direct investments in projects. Over the last decade, the solar industry has expanded into a highly diffused ecosystem comprised of a large range of developers, EPCs, OEMs (though many fewer of these), and financiers. On the financing side, the availability of debt and tax equity has been a key driver of where and what type of projects could be built, and sponsor equity providers have come in as the final layer of the capital stack. Many solar projects with stable cash flows for 15-20 years and limited construction risk can yield returns of 10% or more, which easily beats the returns that can be achieved in the bond market. To really catch the eye of an institutional investor, portfolio sizes need to be in the $100s of millions, ideally yielding unlevered returns of 8% or more. Though large scale projects and bigger portfolios of projects have started to come through the pipeline, it is still difficult for a single developer to create an investment opportunity of the scale and risk profile that serves the needs of institutional investors. Even when these investment opportunities exist, institutional investors are wary of direct investments that expose them to illiquidity or diversification risk. Because of this, much of institutional investment to date has been in providing debt restructuring or acquiring an equity stake in operating assets, as most investors do not want to take on development risk. This is changing, but this mismatch remains an obstacle for moving beyond opportunistic engagement with institutional investors. As a result, some funds specializing in clean energy and low carbon infrastructure investment have emerged to act as stewards of institutional dollars. But will this be enough to really jumpstart institutional investment into solar projects? Asset-backed securities hold the key to bringing institutional investors on board In reality, institutional funds are not going to become big players until a market emerges that can bundle clean energy projects into securities and match institutional investor appetite. And given the predictable cash flows generated by solar projects with long-term PPAs interconnected in stable markets, these projects may actually lend themselves well to forming relatively low-risk, transparent, cash-generating securities. The key here boils down to risk mitigation. When a portfolio of solar project cash flows are pooled into one fund, that fund serves to protect the investor from the developer/sponsor’s corporate risk, which allows for standardized securities to be issued against the capital in that pool. Then, investors have a tradable security through which to commit capital to solar infrastructure investment. If these securities are well received in the market, they can create a virtuous cycle of demand-pull for the underlying asset, in this case solar. Beware: this virtuous cycle also occurred for the housing industry in response to mortgage-backed securities, so this positive feedback can have distortionary impacts on the market as well. At least presently, the solar industry does not seem to invite the same overzealous market speculation that threw the housing industry into a downward spiral. So, are we seeing the emergence of clean energy-backed securities to help leverage institutional investor capital? To some degree, the answer is yes. We can see this primarily in the rise of the green bond market. Bonds as a debt instrument, generate a contracted cash flow, which can back a security. The global green bond market grew to over $40B in 2015, a portion of which was asset-backed securities used to finance aggregate portfolios of smaller debt facilities into institutional investor-sized offerings. But there is a lot of work to do on expanding clean energy finance beyond the bond market. So, keep a lookout for innovations in solar securitization, as it holds the key to attracting institutional investors. Related data points:

Further reading:

|

sign up for ironoak's NewsletterSent about twice per month, these 3-minute digests include bullets on:

Renewable energy | Cleantech & mobility | Finance & entrepreneurship | Attempts at humor (what?) author

Photo by Patrick Fore on Unsplash

|

© 2009-2022 IronOak Energy Capital, LLC | (888) 249-3013