|

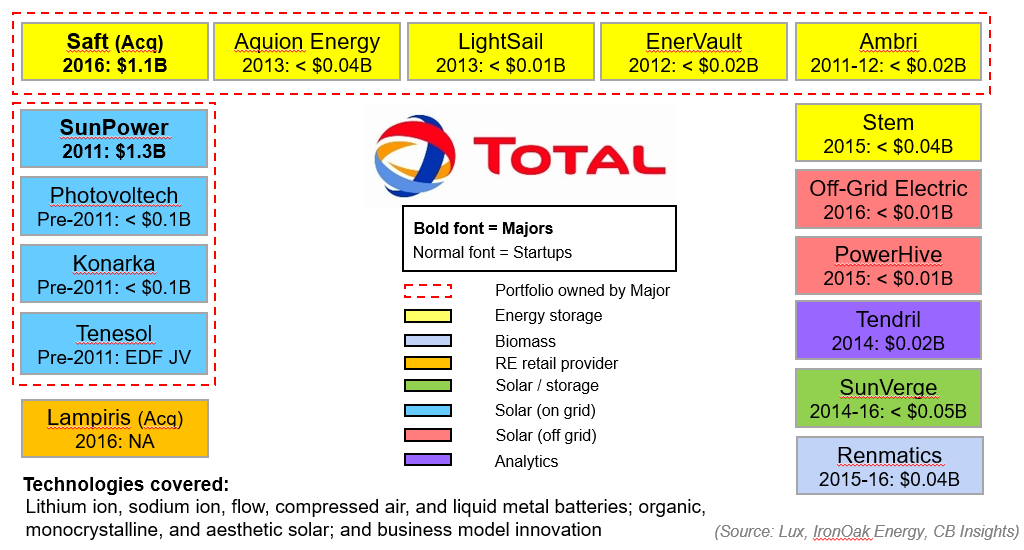

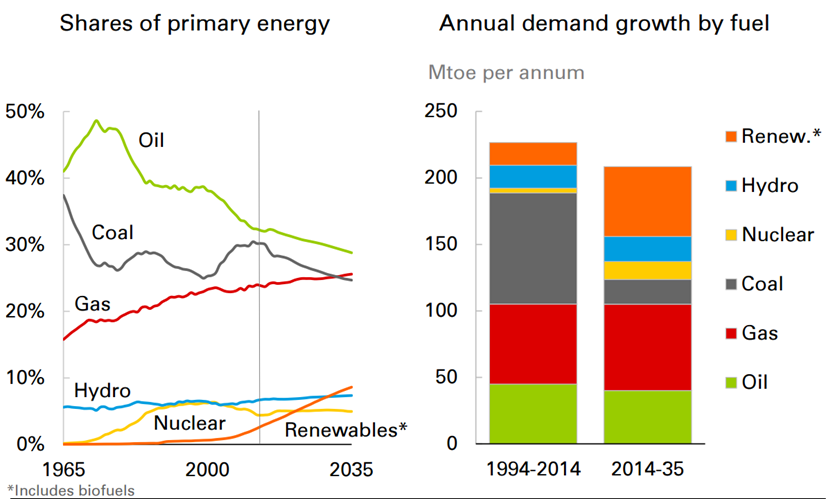

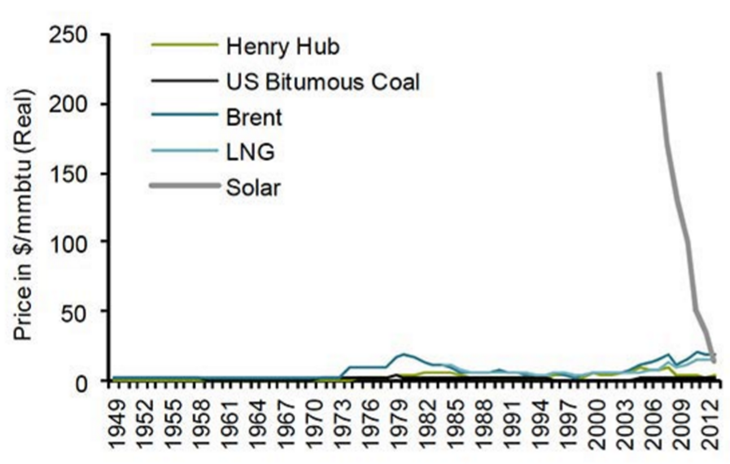

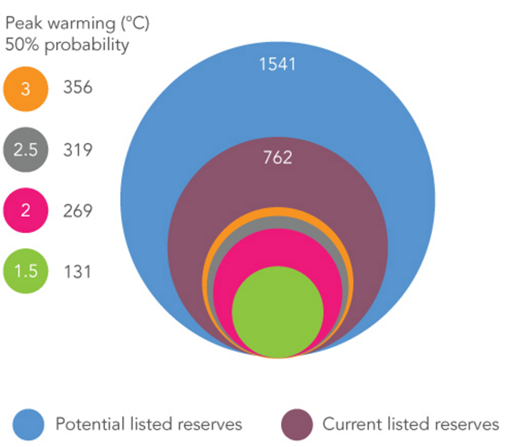

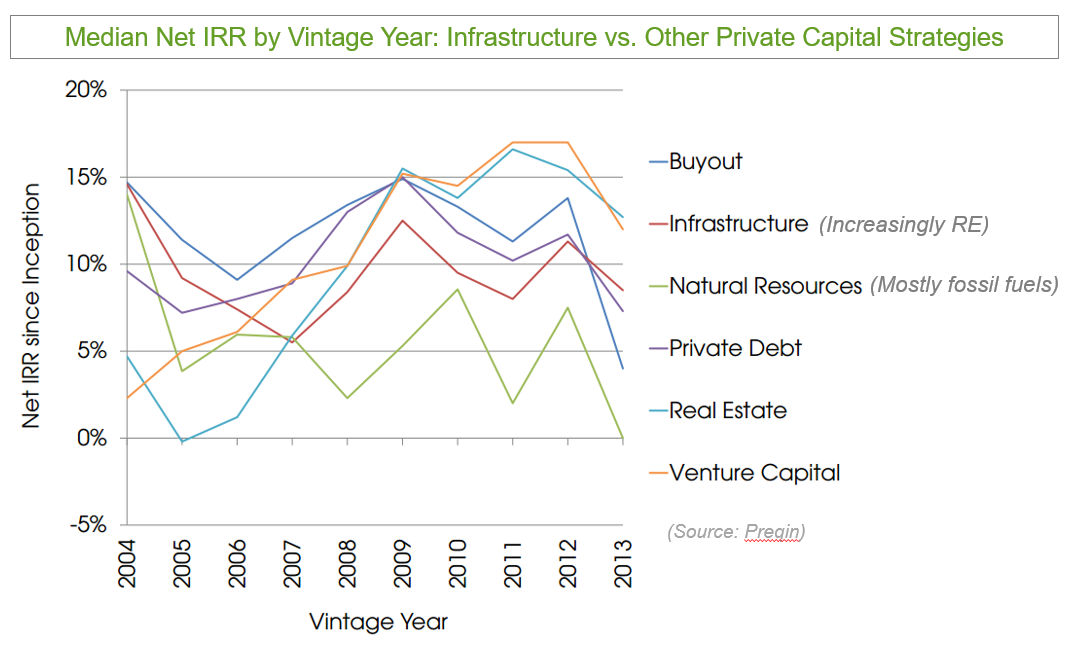

8/30/2016 Major Oil and Gas Companies’ Growing Interest in Renewable Energy Investments: Passing Fad or Major Trend?Read Now You may remember BP’s attempt to rebrand as “Beyond Petroleum” years ago. Perhaps sincere, or maybe a public relations game, it did not last long. One thing for sure: It bred some real clean energy innovators, some of whom we at IronOak Energy work with today in their new ventures. The question is this: Are today’s headlines about fossil fuel majors investing in renewable energy any different? As I prepared to deliver a webcast to 75 global energy investors on this topic, many of our investment colleagues were doubtful. But I do think that things have changed. I’ll try to illustrate why I think this is the case (and hopefully I won’t look back in five years with my tail between my legs). Consider the leading conventional energy company in this new paradigm: Total, the French energy giant. Below is a figure which illustrates most of Total’s alternative energy investments, whether direct or indirect.  Source: Lux, CB Insights, IronOak Energy But their clean energy play doesn’t stop there. Consider these additional facts from 2015: They committed to investing $500M in renewable energy per year going forward. They invested $225M to convert an unprofitable oil refinery into a biofuel plant. Why are oil and gas giants moving to more clean energy? 1. Granola-eating, Birkenstock-wearing They have become a bunch of long-haired hippies. Nope, not true. I'm just seeing if you’re paying attention. 2. FOMO? If you’re not a Millennial, let me clarify. This is not a curse word. Instead, it stands for Fear of Missing Out. The global energy mix is projected to change, and they don’t want to miss out on high-growth opportunities. See the graphs below.  Source: BP 3. Costs Solar and wind costs are much more competitive today. Consider the two large solar farm contracts at 2.9 c/kWh in Chile and the Middle East. See graph below.  Source: BNEF Source: Bernstein Research, CIA, EIA, World Bank 4. Global policy The Paris Accord showed 197 countries agreeing to significant greenhouse gas reduction goals. If their forecasts by the International Energy Agency are correct, $16.5T of low-carbon finance is needed to achieve the goals laid out in Paris. 5. Stranded assets Experts at the London School of Economics, Citi, and Carbon Tracker suggest that 60-80% of assets held by publicly listed conventional energy companies may be “unburnable” if the world is to stay below the 2 degrees Celsius target. Citi’s estimate is that $100T of oil, gas, and coal reserves may fall into this category. Yikes. (See graph below. Compare the smaller pink circle to the larger purple or blue circles. Units are GtCO2.)  Source: Carbon Tracker, Grantham Research Institute, LSE 6. Growing interest in infrastructure The World Economic Forum estimates a $1T/year gap between global infrastructure needs and what limited government budgets can afford. This spells a big need for private capital to fill this gap. This combined with the current low-yield environment has led to growing investor interest in the global infrastructure market with an aggregate $3.7T/year need. Investors are seeing the attractive risk-reward fundamentals of infrastructure investment, in which renewable energy represented 55% of all deals in 2015. See the graph below highlighting the relative attractiveness of infrastructure investments.  And by the way, I’m just getting started. We haven’t even talked about clean energy investments by other oil majors.

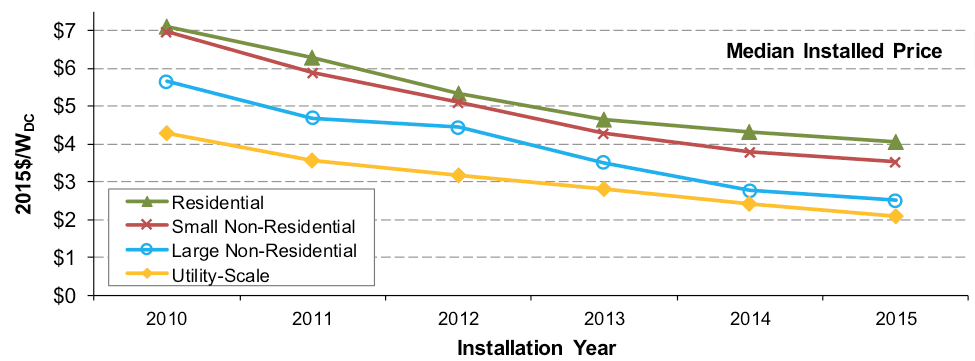

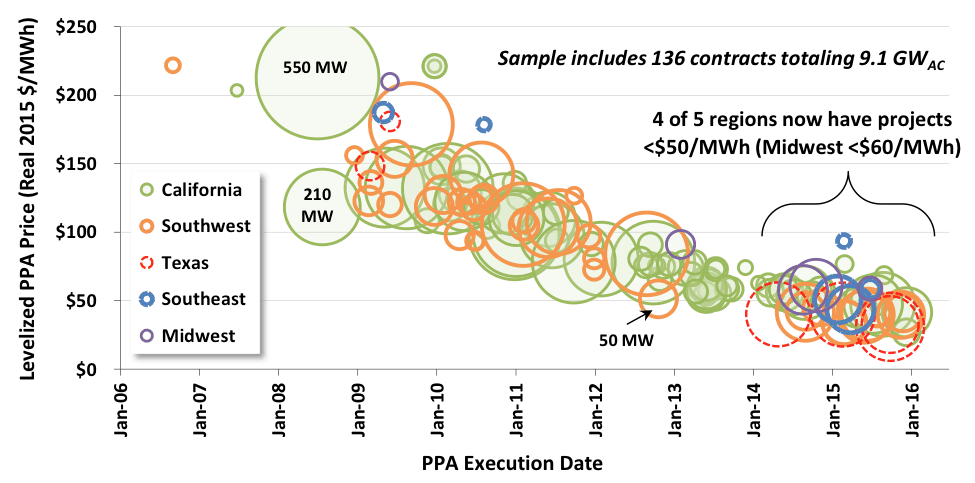

With between $5B and $30B in cash on hand, how will they diversify going forward? Surely not all to renewable energy, but probably a greater allocation than in years past. Does every solar project have to be big? Many solar investors’ intuition rests easy when they see the graph below. It fits into the elegant framework of “economies of scale.” The bigger the project, the lower unit cost of installation. The smaller the project, more cost-inefficient. Going big is part and parcel with cost efficiency, or so the saying goes.  (Source: Lawrence Berkeley National Laboratory) But be careful, this is precisely the rationale used to advocate that utility-scale solar is the only form of solar in which we, as a society, should be investing. Heck, Warren Buffett believes so, and that guy never makes a bad bet (at least publicly). Why produce electricity from projects that can be built at $4/MW on top of a house, when you can generate those same electrons from a larger project that can be built for half the cost? It is a compelling argument, I must admit. But it suffers from the same “big infrastructure” fallacy that is currently hamstringing our legacy centralized energy system. Build BIG projects for cheap on a per MW basis. Big is cheap and efficient. But, as any good economist knows, external costs can cause headaches (and asthma, skin cancer… you get my drift). Utility-scale projects have gotten a free ride See, BIG projects are cheap, in part, because they burden society with costs not borne by the projects themselves. What costs you might say -- only the never-ending litany of transmission and distribution expenditures. Billions of dollars of deferred T&D expenditures hang like a dark cloud over electric sector. And who is paying for those? Not the project owner, that is for sure. Yes, there are interconnection costs, but let’s be real, they hardly cover it. That is not to say that there is not, in fact, a significant need for big projects. But only to a certain extent. Why only build projects that necessitate that we continue to invest so heavily and T&D infrastructure? Small can be beautiful (and efficient), too. Yes, we should invest in more high voltage DC transmission. But, why not minimize the need for such costly investments by building smaller C&I and residential projects? They may be more costly on paper, but at the scale of the whole grid, they may actually be introduce some much needed cost-cutting. Thus, it is the prospect of avoided T&D costs that gives any credence to the claim that smaller-scale projects can be both both prudent and cost-efficient. Avoided costs is a common concept in utility-scale generation, but, for some reason, this logic is not applied to smaller-scale projects. It is not because they don’t make sense, it is because utilities are uncomfortable with power producers that they do not control. Investors start to take notice of smaller-scale solar Now, from the perspective of an investor looking to be a long-term project owner, things get interesting. The graph below show the slow march down the path of PPA price decline.  (Source: Lawrence Berkeley National Laboratory)

On the one hand, great - solar power is getting cheaper, and fast! On the other, there is a palpable sense that there is large-scale suppression of investors returns taking place. Fair enough. Once a market matures, actual or perceived technological risk reduces, and returns should decrease. But that does not stop investors from feeling the squeeze. And that squeeze is happening particularly in the utility-scale market. In part because utilities have a lot of negotiating power in many markets, PPA prices are plummeting, some creeping below the $0.04/kWh threshold. There is still value to be had, but the pressure to find good deals has encouraged (ahem… forced) investors to look back into the C&I market for the returns they seek. This is great from the standpoint of increasing access to capital for a market segment which historically has been more difficult to finance. Less standardized and smaller projects, diverse off-takers, many without credit ratings, and less financially robust developers have all hampered the expansion of C&I solar. But, now the suppression of utility-scale solar returns has led investors to start poking around the sleeping giant of C&I solar. Many C&I off-takers have the ability and willingness to pay much higher PPA rates than utilities. Translation = sweet returns. And, there are a LOT of them. If you are lucky enough to find them in places like Nevada where many large-scale C&I customers have been summarily pissed off by the antagonistic treatment by the utilities commission, then you could make some big waves. And, as C&I developers have become more sophisticated, projects are trending towards more consistency, bankability, and less risk. So, keep a lookout as the C&I solar market starts to find that sweet spot in the classic risk vs. return story. Small can be beautiful in the solar market. Projections are a fool’s game, but they are also unavoidable if you happen to care about infrastructure finance and policy. Why? Because investors are keen on timing the market, and economists and policy experts want to know when and how to intervene in the market. Understanding the dynamics of technology costs versus willingness to pay is central to both. Even with marked growth in the energy storage sector, the assumption is that the real boom awaits further cost reductions. Everyone is projecting those reductions. Here we dig into "why" and "where" those reductions may come from.  Source: Ramez Naam We are all familiar with the proliferation of cost projections out there, much like the one shown above. Lots of reputable establishments produce these projections, with many clever approaches to thinking about technological progress (e.g., stuff getting cheaper and better).

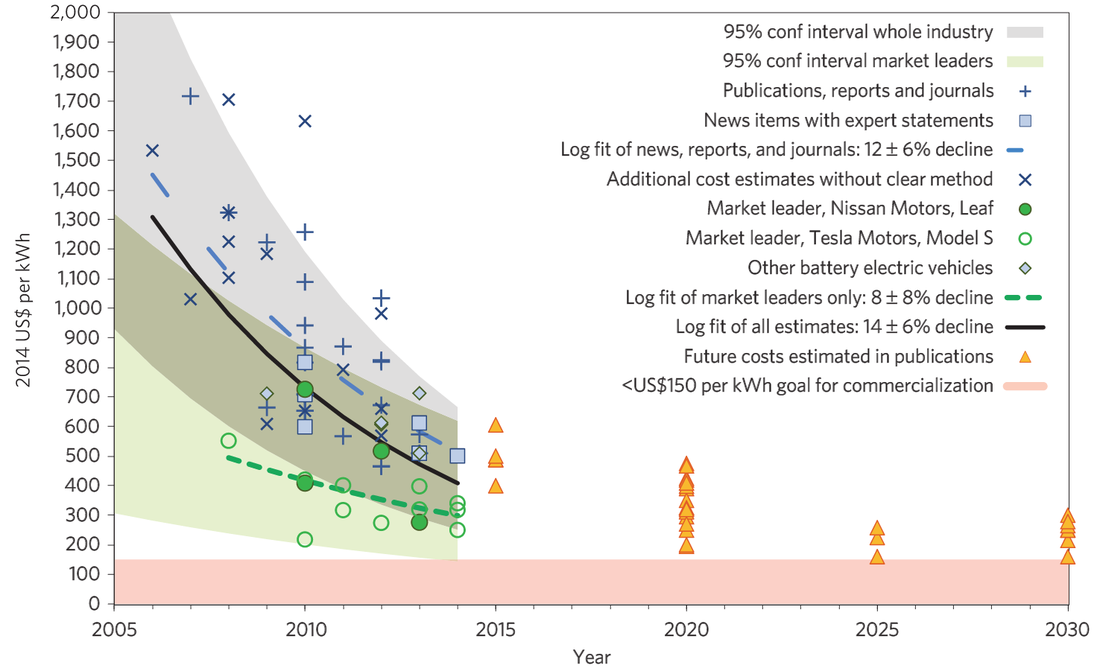

They all tend to take a similar shape, gently downward sloping cost reductions to that special place of widespread commercial adoption. This is the hallowed “no-brainer” zone which solar now enjoys in many locales. There is nothing inherently wrong with this blanket approach to understanding the trajectory of an industry. In fact, I have spent many years of my professional life developing nifty statistical projections and models. After all of that time and effort, it is clear to me that (1) projections are all inherently wrong, though at times useful and (2) projections obscure the more important question of “why.” It is the second point that I want to dig into here. I often encounter the question - “What does the future hold for the energy storage industry?” Often, the response I hear has something to do with projections - X% growth over the next five years, X units of installed capacity, etc. Rarely do I hear any mention of the underlying driver of why this growth is happening. There is just a secular belief in progress, and the only real question is how fast. Here is where things get interesting with energy storage. Unlike solar, energy storage is an remarkably heterogeneous technology with applications that span a wide variety of industries. Yes, solar can be big or small, installed at a residence, commercial building, or as a grid-connected farm. There is some variety, but it all boils down to producing electricity for an off-taker. Technological progress — solar getting cheaper and more efficient — has been driven by ramping up installations across the spectrum of solar applications. “Learning by doing” it is called. The more solar we built, the cheaper it became. Energy storage, on the other hand, has drivers across sectors. There is a boom of interest in residential storage, but not to be outdone by interest in the C&I sector for behind-the-meter storage. Utility-scale storage lurks in the corner, and may ultimately be a larger driver of industry growth when the right market mechanisms are in place. But the 800-pound gorilla in the room are electric vehicles. The explosion of interest in EVs — lead by Tesla, Chevy, Nissan, Volkswagen, and others — is building up pressure for cost reductions in battery technology. If and when battery costs drop below the $200-$300/kWh threshold, it may unleash a flood of consumer adoption. This would be fuel to the flame of that virtuous cycle of adoption driving further cost reductions, which, in turn, would drive even more widespread adoption. My hunch is that growth in EVs will be a more powerful initial key driver in pushing down energy storage costs for building- or grid-level applications. The simple fact of the matter is that EVs can scale faster, thereby spurring much-needed “learning by doing.” So, it may behoove you to keep an eye outside of the normal places to understand the “why” behind the reductions we are witnessing (and hope to witness) in energy storage technology. Nobody likes paying more than they should. And my dad is a CPA, so this is definitely true for me, too. But this barrier is not unique to renewable electricity. The same expectation is true for most non-luxury goods and services. Yet I still hear the objections everywhere -- from sophisticated investors to family friends -- that solar and wind are too expensive. Is that still true? Yes, but increasingly no. OK, to be clear, most of the data says no, but as you know, perception is reality. This lingering misperception is also being observed by other energy leaders, including the Director of Sustainability and Cleantech at Schneider Electric in recent a Greentech Media article about Scheider’s New Energy Opportunities (NEO) Network. Consider the graph below from Clean Edge, which is based on data from the US Lawrence Berkeley National Laboratory. The levelized costs for solar electricity (LCOE) has fallen from 22.5 c/kwh to less than 5 c/kwh. That’s a roughly 78% drop in price over the last 10 years. But unless an investor or corporate executive has regularly re-evaluated the business case for alternative energy, they might have missed these market changes.  It’s important to note that this refers to utility-scale solar, not rooftop solar. The latter has a higher LCOE (c/kwh), but it also competes with higher retail electricity rates. Additionally, Deutsche Bank estimates that unsubsidized rooftop solar is 30% cheaper than retail power prices in many countries. See their map below showing countries with substantial areas of grid parity. Finally, here’s another data-driven perspective from investment advisory firm, Lazard. The resolution is not great, so let me help you out. Here are some of the lowest LCOE values from highest to lowest:

Here’s a link to the full Lazard report, version 9.0.

If you like data and charts, you’re going to really enjoy this. Grab a big coffee and settle in for some quant goodness. And next time someone says that solar is too expensive, you can admit they are partially right. But then give them a little dose of 2016 data. |

sign up for ironoak's NewsletterSent about twice per month, these 3-minute digests include bullets on:

Renewable energy | Cleantech & mobility | Finance & entrepreneurship | Attempts at humor (what?) author

Photo by Patrick Fore on Unsplash

|

{kind=link}

© 2009-2022 IronOak Energy Capital, LLC | (888) 249-3013