|

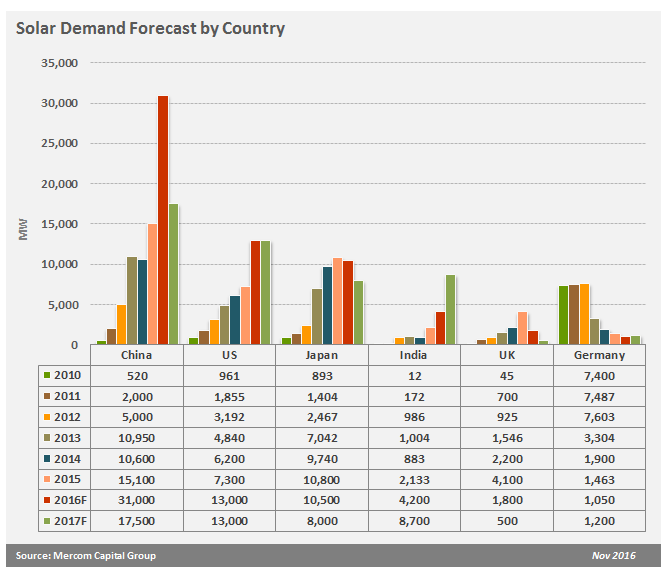

1. Growth in global solar development has not stalled, despite the 8% decline projected for 2017 Global solar development is projected to grow a remarkable 48% compared to 2015, reaching 76 GW installed by the end of 2016, according to Mercon Capital Group. We in the U.S. cannot claim all of the credit. It appears as though record-level solar development in China is largely responsible for this growth. But when you look at 2017, investors start to become very wary. Exponential growth from 2.6 GW to 76 GW in 10 years (40% CAGR), followed by a projected 8% decline in 2017! What gives? Well, again the story is about China, which is expecting a steep decline as a result of anticipated tariff cuts and reduced national targets following the solar module oversupply that fueled the 2016 growth. In the U.S, we are expected to stay steady after a 70% spike in solar development in 2016. But let’s not sleep on Japan (still a vibrant market) and India (emerging as a real contender).  (Source: Solar Industry Magazine) 2. Don’t get too concerned about fluctuating solar stock prices -- remember the long game Public markets are fickle. And remember stocks are valued (theoretically) in terms of future projected cash flows. Which means it is all about expectations. Right now, many investors feel there is a bear market lurking around the corner, and the SunEdison debacle has done little to assuage the public’s concern about the solar industry. The big name market barometers are sending signals to be very worried about the long-term prospects of the solar industry. SunPower (SPWR), First Solar (FLSR), and Canadian Solar (CSIQ) are all taking a nosedive. Yieldcos -- Pattern Energy (PEGI), 8point3 Energy Partners (CAFD), and the much beleaguered Terraform Power (TERP) -- are also all trending down after a comeback from last summer’s downturn. Two things are dragging down stock prices - persistent low module costs putting a downward pressure on revenues and over-leverage eroding cash flows. Only the companies with the financial agility to continue to generate positive cash flows will weather the price wars, but the solar industry as a whole with weather this period successfully.   (Source: Google Finance) 3. 83 companies committed to 100% renewable, but just wait for the prosumer revolution According to RE100, some of the largest corporations in the world are aiming to get to 100% renewables. Some of the usual suspects are from the tech world -- Apple, Facebook, Google. But you might be surprised to find old school corporate behemoths such as WalMart, Nike, Johnson & Johnson, Proctor & Gamble, and the Tata group have joined the ranks, as well. Now, all of that will not be solar, but a lot of it will. Solar affords the corporate investor a lot more flexibility in the project size and location, lower basis risk, and better synchronicity with peak demand. Corporate power purchasing grew to 3.23 GW in 2015 (Source: RMI), and is only expected to grow more, especially as virtual net metering and community solar policies allow for more off-site solar solutions. Watch out for some of these companies to cross into the ranks of “prosumers,” companies that both produce and consume energy. Apple recently filed for licenses in California, Oregon, and Nevada to sell its excess electricity directly to consumers (Source: HBR). This really could be a gamechanger. 4. Solar investors flock south to Latin America, even as returns head in the same direction It is not headline news that Latin America is becoming an attractive area for investment in solar. The region is expected to grow at an annual rate of 40% through 2021 after all, with Mexico, Chile, and Argentina leading the charge. Amid the many interesting facets of solar development and investment in Latin America -- transmission constraints, locational variability in price, currency and credit risk, new renewable energy mandates and policies, etc. -- the real braintickler is how are all of the auctions going to play out over time. Auctions have consistently returned remarkably low prices - $45/MWh in Mexico, $29/MWh in Chile, and $59/MWh in Argentina. With falling solar module prices, there is some room for developers to deliver projects that can meet investor hurdle rates at those prices. But the competition is tough, and some investors have grown wary of playing the auction game. All the while, do not forget about Central America and the Caribbean. El Salvador and Honduras, among others, are paving the way for solar expansion with a range of promising utility-scale projects.  (Sources: GTM) 5. Community solar is the real anti-establishment energy choice Even though SunRun wants you to think that “roof-top solar is the anti-establishment energy choice” (Source: GTM), it is not a choice available to nearly half of all U.S. households. Enter community solar, the renewable energy choice for the masses, including the often forgotten low- to medium-income households. The benefits to offtakers are obvious -- access to clean, reliable electricity from solar farms built at a much lower cost than their roof-top solar siblings ($2.00-$2.50/W vs. $3.00-$3.50/W). And based on a simple savings-to-investment ratio, 35-48 states are attractive locations for community solar. No wonder NREL projects that community solar will make up half the distributed generation market by 2020 (Source: NREL). Once investors can get comfortable underwriting the somewhat unique risks of community solar projects, there will likely be a fairly attractive risk-return profile and a largely untapped market if and where policy falls in line.  (Source: DOE Office of Energy Efficiency & Renewable Energy)

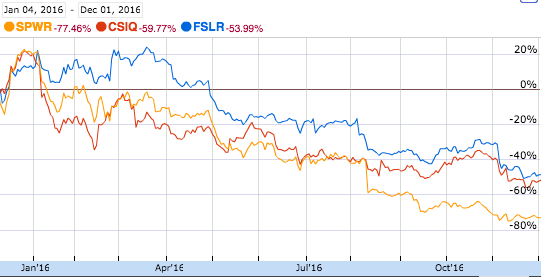

Postscript. Elephant in the room -- No one knows what the Trump era holds for solar Policy support at the federal level, most notably the ITC, has been essential in accelerating the growth and maturation of the solar industry. The ITC appears safe for the moment, but may end up on the chopping block in a larger tax reform bill. Nobody knows. What we do know is that the solar industry is here to stay, federal incentives or not. The value propositions for solar -- clean and affordable source of electricity, economic development and job creation, and attractive investment opportunities -- are not going to change. There may be bumps in the road if the federal government attempts to resuscitate the coal industry at the expense of support for renewables, but the industry will navigate them and move on. Coal's downward spiral is unlikely to be something that Trump can avert despite his grandiose promises (Source: Yale Environment 360). I’ll leave you with one heartening statistic - there are more clean energy jobs in the state of Ohio than there are coal industry jobs in the entire U.S. (Source: Renewable Energy World). If President-elect Trump holds to his promise to focus on job creation, the answer should be clear for all to see. Comments are closed.

|

sign up for ironoak's NewsletterSent about twice per month, these 3-minute digests include bullets on:

Renewable energy | Cleantech & mobility | Finance & entrepreneurship | Attempts at humor (what?) author

Photo by Patrick Fore on Unsplash

|

© 2009-2022 IronOak Energy Capital, LLC | (888) 249-3013