|

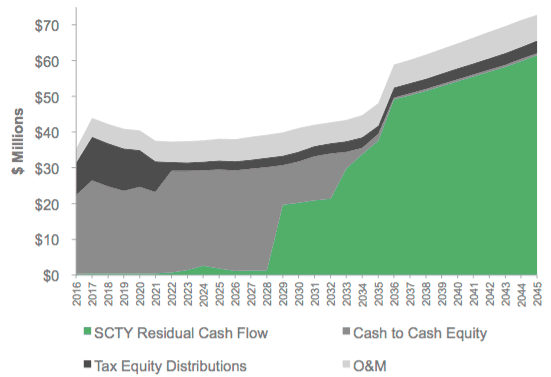

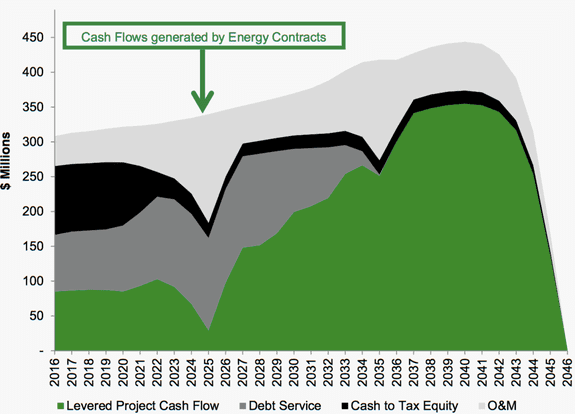

SolarCity Residual Cash Flows  (Source: SolarCity) SolarCity is still the prettiest girl at the dance SolarCity is without a doubt the most trend-setting solar finance company on the planet. They are a vertically-integrated, distributed solar superpower that seems to grab newsworthy headlines on a weekly, sometimes even daily basis. On April 6th, SolarCity announced a $150 million non-recourse financing facility with Credit Suisse to support the deployment of new commercial PV and energy storage assets. The very next day, the company announced a tax equity closing of $188 million from Bank of America Merrill Lynch for residential solar deployment. At first glance, that amount of activity could worry investors that SolarCity is pursuing too many verticals in parallel without focusing efforts on the most profitable segments. This type of investor sentiment is currently relevant considering that the mainstream explanation for SunEdison’s bankruptcy is simply that the company took on too much debt while drinking water from several different fire hoses. I would argue that SolarCity is similarly extended in terms of asset classes, but they have been consistently more savvy than SunEdison in regards to monetization. Unlike SunEdison, SolarCity has maintained a focus on creative financial engineering that produces near-term cash flows to sustain the upfront capital outlays required by today’s solar finance institutions. John Hancock to the rescue? On May 4th, SolarCity completed a $227 million “cash equity” financing with John Hancock Financial for approximately 200 MW of operating solar projects. This transaction serves as the most recent example of SolarCity monetizing the underlying cash flows associated with the company’s long-term power purchase agreements with individual off-takers. Unlike the two transactions in April, John Hancock’s injection is not a critical component of the capital stack to initially finance the development and construction of solar projects. This cash equity transaction is regarding solar assets already in operation, across three segments (residential, commercial, industrial), and spread between 18 U.S. states. Within this portfolio, the average FICO score for residential customers is 744, and most of the commercial off-takers are national retailers. News flash: large institutional investor is attracted to diversified portfolio with virtually no risks. Which begs the question, why did SolarCity take a discount on future cash flows and sell now? Just like every other solar company in the 3rd party ownership space, SolarCity is bleeding cash due to the high customer acquisition costs and needs to display short-term revenue to keep shareholders confident in the company’s long-term value proposition as a distributed power provider. See here for a current perspective of the 3rd party ownership climate in the U.S. Despite the success of matching low-risk solar PPA payments with an institution that is all too familiar with generic annuities, SolarCity now has some longer term expense considerations to overcome. They are still responsible for the O&M expenses related to servicing the 200 MW of assets, and they’re responsible for expenses related to decommissioning the PV systems if the PPA term is not extended. As part of the cash equity transaction, SolarCity retains the rights to 99% of the post-PPA cash flows, but it's anyone’s guess how likely it is that post-PPA revenue streams will be realized. Although this transaction structure is new and newsworthy, it’s just another tool in the solar finance industry’s toolbox to monetize future cash flows. SolarCity Cash Flows  (Source: SolarCity)

The jury is still out on whether solar and securitization are a match made in heaven Asset-backed securities have a negative connotation to the layperson, to say the least. But there’s no denying that securitization can play an important role in increasing investor access to specific asset classes, as well as raising affordable sources of financing in capital intensive industries, like solar energy. The key word here is affordable. SolarCity has now sold six tranches of solar-backed securities over the last 30 months, including $49 million on March 1st when the weighted interest rate was almost two percentage points higher than a sale just 12 months earlier. The rise in SolarCity’s cost of capital is troublesome and may cause the company to abandon the new strategy and seek out alternative forms of financing. It’s clear that the 'SunEdison effect’ is having a real impact on investor comfort with the reliability of long-term solar contracts, despite the incredibly low default rates experienced by SolarCity (and others) to date. As long as default rates remain very low and companies continue to drive down the cost of customer acquisition, the opportunity to sell the underlying cash flows of solar projects will remain for both public and private developers. Comments are closed.

|

sign up for ironoak's NewsletterSent about twice per month, these 3-minute digests include bullets on:

Renewable energy | Cleantech & mobility | Finance & entrepreneurship | Attempts at humor (what?) author

Photo by Patrick Fore on Unsplash

|

© 2009-2022 IronOak Energy Capital, LLC | (888) 249-3013