|

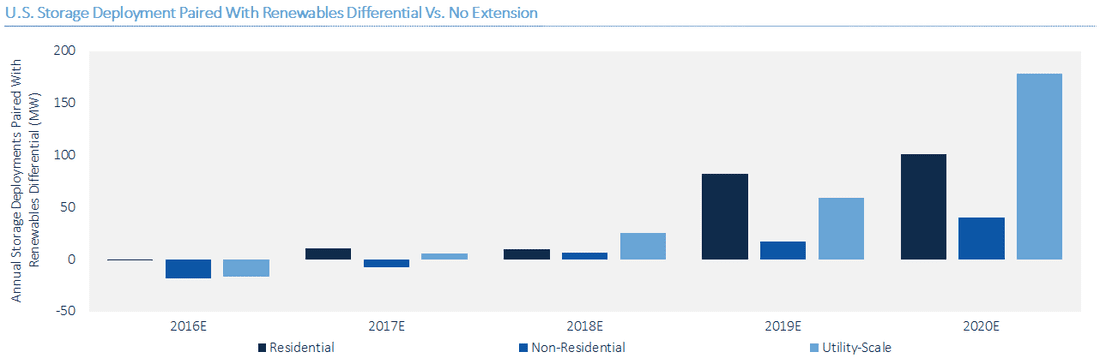

Congress is again considering an energy storage investment tax credit The proposed H.R.5350, known in short form as the “Energy Storage Act of 2016,” seeks “To amend the Internal Revenue Code of 1986 to provide for an energy investment credit for energy storage property connected to the grid, and for other purposes.” Sponsored by Silicon Valley’s Congressman Mike Honda (D-CA), the bill has bipartisan co-sponsorship from Reps. Tom Reed (R-NY), Chris Gibson (R-NY), and Mark Takano (D-CA). As reported, it also has the full support of the Energy Storage Association: “The bipartisan Energy Storage Act of 2016 would unlock competitive access to investment in a more resilient and efficient modern electrical grid by expanding the investment tax credit (ITC) to include all types of advanced energy storage,” according to ESA Executive Director Matt Roberts. We’ve seen public support for energy storage tried before at the national level, such as with last year’s push to pass a national storage mandate. The current initiative builds on earlier efforts for a storage ITC. For example, in 2013 Sen. Ron Wyden (D-OR) proposed a bill that would have granted a 20% tax credit for systems above 1 MW/1 MWh and a 30% credit for smaller 1 kW/5 kWh systems. A potential $2 billion for energy storage The details are as follows. A 30% investment tax credit is allowed for any “qualified energy storage property” (see below). Two billion dollars would be set aside in total credits for the life of the proposed program, with any single storage project capped at $40 million. As a side note, under these constraints it makes sense to assume that energy storage project developers would be incentivized to keep total project size under a $133 million price tag. What qualifies? At a first reading there does not appear to be a capacity size requirement for any large project, as long as it is used for one of the following purposes: 1) peak demand management; 2) deferral or substitution of investments in generation, transmission, or distribution; 3) backup for variable generation; 4) transmission or distribution grid reliability; 5) end-user energy consumption management; or 6) disconnection of load from the main grid. All energy storage technologies are also covered, including mechanical, electrical, thermal, and electrostatic. Small residential storage would qualify as well, if installed at primary residences and used for peak energy reduction for primarily onsite consumption. These systems must have a 5 kWh capacity and the ability to deliver 1 kW of electricity over 4 hours. What doesn’t qualify? In general, non-residential energy storage that is designed primarily for on-site consumption does not qualify, unless it exceeds a 5KWh energy capacity and the ability to discharge 1 KW for 5 hours. Special exceptions are given to both pumped hydro and compressed air storage -- these projects must begin construction and operation within set timeframes or risk losing the credit. Supporting storage? Two points to consider The first point to consider is that -- to the extent to which energy storage is paired with renewables -- it may be under-supplied in the current market and deserving of public support. A study that was released in-press last week in Applied Energy from researchers at the University of East Anglia is garnering a lot of attention. In the article, “The value of arbitrage for energy storage: Evidence from European electricity markets,” researchers simulate the arbitrage value of price-taker pumped hydro and compressed air energy storage under different market characteristics and across a portfolio of energy trading strategies. Not surprisingly, decisions can be made to maximize these values across different conditions. More significant was a summary conclusion: “Government subsidies should be used to encourage investment in energy storage systems if renewable power is to be fully integrated into the sector…” The second point is that a separate energy storage ITC is not the only pathway to support energy storage. Some storage is in fact already eligible for the solar ITC as long as it follows strict rules about explicit pairing with and charging from solar power generation sources. As seen below, we already know that energy storage is expected to receive a huge boost from the extended ITC for solar, whether or not it takes advantage of this limited opportunity under the solar ITC. U.S. Storage Deployment Paired with Renewables Differential vs. No Extension  (Source: Greentech Media)

The current IRS rules on storage eligibility under the solar ITC have been described as “ambiguous.” In February, the IRS issued a request for comments on this issue, with observers hoping for further clarification in future letters. Regarding the eligibility of storage, the required pairing with renewables was seen as necessary in order to avoid subsidizing storage that was existing merely to arbitrage with the grid, rather than serving as a support for renewables. Conceivably the IRS could decide to expand storage eligibility under the existing solar ITC, but this seems like a case of trying to fit a new effort (storage) under a policy for which it was not designed (solar power promotion). The good news is that the new proposed energy storage ITC excludes subsidizing projects that exist merely for arbitrage. Allocation of the credits across projects would be determined by the DOE, to choose those that maximize the following metrics: reliability or economic benefit, integration of renewable resources on the grid, or efficiency of grid operations. H.R. 5350 is just beginning its path from bill to law, but the possibility is there for an energy storage ITC to complement the existing solar ITC. Comments are closed.

|

sign up for ironoak's NewsletterSent about twice per month, these 3-minute digests include bullets on:

Renewable energy | Cleantech & mobility | Finance & entrepreneurship | Attempts at humor (what?) author

Photo by Patrick Fore on Unsplash

|

© 2009-2022 IronOak Energy Capital, LLC | (888) 249-3013