|

Most investors we talk to are not investing in electric vehicles for a few reasons:

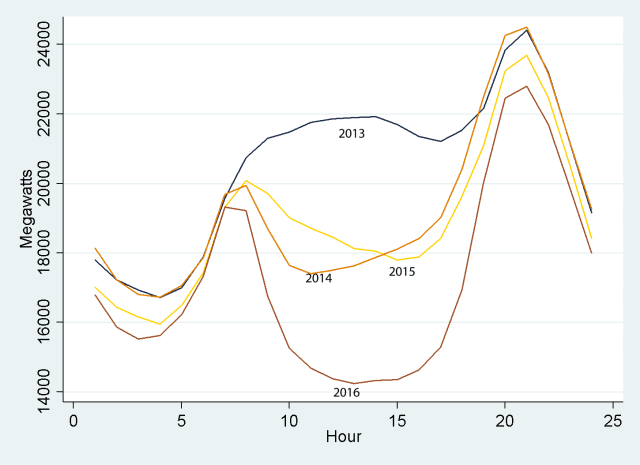

In this and our future market insight pieces, we’ll address these concerns. Yep, the EV market is tiny, but it will be mainstream in just a few years. The time to get smart on EVs and take action is now. The data below is from the good folks at Deutsche Bank. Note a 3x growth by 2020 and 5x growth by 2025.  Who’s winning the EV race? 1. Duh, it’s Tesla. 2. What? Tesla is not the only EV in the world? 3. The competition is global. Many investors have never heard of some leading EV car lines. Again, great stuff from the environmental NGO....uh...I mean, global investment giant Deutsche Bank. Kudos. Which ducks do you see?The California Independent System Operator (CAISO) can be commended for providing an accessible daily data dump on renewable usage across its system. With these data one can construct various “duck curves” for the grid’s daily net load profile, the shapes of which result from the rising penetration of a variable energy resources (VER) such as wind or solar. VERs exhibit four characteristics:

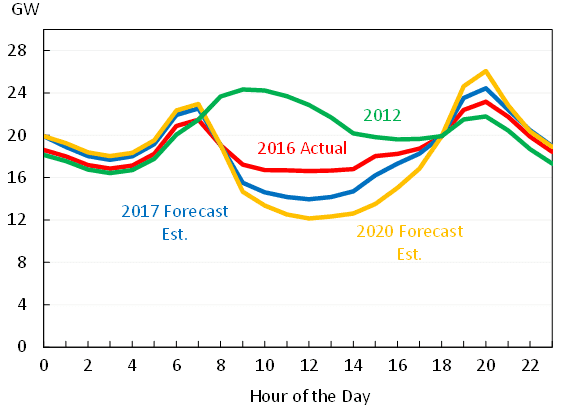

Duck curves are in essence the daily net load profiles after accounting for VER generation. They show the required remaining dispatchable energy required to ramp up or down to take up the solar and wind shortfall. As we see from the two examples below, duck curves can take on various forms, often depending on the scale range of the y-axis. 1st flock of ducks: Average net load profiles over seven days around March 31, over 2013-16.  Source: Blog post by Meredith Fowlie, “The Duck Has Landed” (5/2/16), using CAISO data. 2nd flock of ducks: Net load profiles for March 31 for 2012 and 2016. Forecasts for 2017 and 2020 were made in 2013.  Source: Council of Economic Advisors, The White House, “Incorporating Renewables into the Electric Grid: Expanding Opportunities for Smart Markets and Energy Storage,” Fig., 4 (June, 2016), using CAISO data.

Both sets of curves cover almost exactly the same sets of data, with the first emphasizing a more extreme story. The the stories are essentially the same -- net load after VERs bottoms during the day when solar is peaking, ramps up very quickly as solar generation drops off dramatically and evening usage rises, and then drops again as nighttime usage drops and wind picks up. The takeaways are two:

Ancillary services as regulation mileage A recent report from the Council of Economic Advisors at the White House goes deeper, looking at some ways of understanding the value of energy storage via the idea of regulation mileage. The concept measures the changes -- increases or decreases -- in power output that a grid operator requests from an electricity generation resource over a specific timeframe. It would stand to reason that regulation mileage, a proxy for the amount of ancillary services required, would be determined by several factors. The Council’s study looks at the total load, the amount of that load from VERs, the slopes of each of those load curves, and a series of effects that are specific to the hour of the day, day of the week, and week of the year that the electricity is generated. Among other results, and as expected, one of the clearest that appears is that the slopes of the load and VER generation have a lot to do with the services required. In other words, the faster the late-afternoon ramp up at the end of a sunny day, the more energy storage will be wanted. Valuing storage based on its ancillary benefits What are other approaches to valuing energy storage in these settings? The peer-reviewed journal Nature Energy recently carried the results of a new study on capturing the full benefits of energy storage in investments. Applying a techno-economic model, the authors of ”Limiting the public cost of stationary battery deployment by combining applications,” find that battery storage becomes more attractive as an investment as each storage facility offers more energy services. An article summary carries the message that energy storage apart from pumped hydro is, “still considered unattractive by investors on mainly two grounds: cost-competitiveness with other technologies and the absence of a commonly shared classification of electrical storage as a competitive or regulated activity -- that is, as an electricity generation asset or network component” (emphasis added). The drawn conclusions are that the best way to incorporate all of these benefits are to remove non-market barriers, a legacy of rules that were originally written for conventional generators. According to the summary, these “institutional and regulatory frameworks are key elements in the determination of the economic value of storage,” and “economic principles require new, enabling rules to be technology neutral, that is, not directed at the diffusion of storage or any other technology in particular.” The article calls for three such policy recommendations:

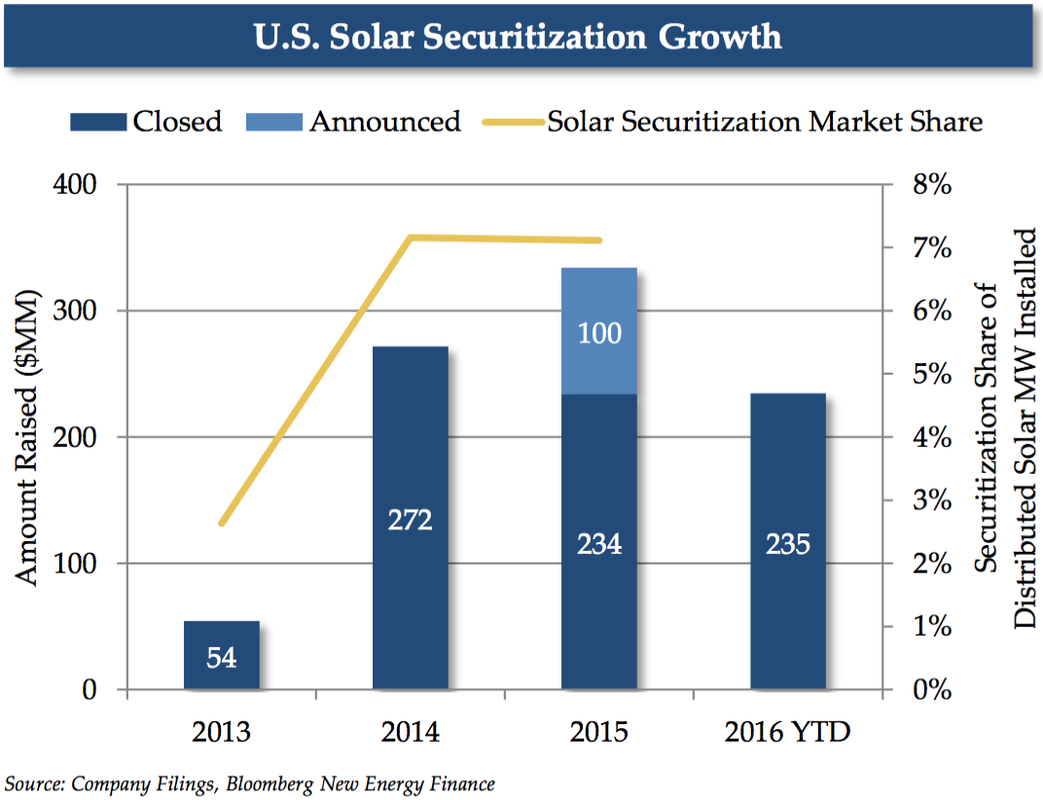

This policy neutrality from above is a point worth repeating. In revising public policies, the goal is not the promotion of energy storage out of any favoritism towards the technology. Rather, the point is to promote energy storage as an enabler for VERs such as solar and wind, which in turn leads to progress on an overall societal goal of reducing greenhouse gas emissions.  Solar securitization has been a popular theme at IronOak Energy, and for good reason. Access to gobs of low cost capital is every solar developer’s dream, along with, of course, limitless net metering (but what about Value of Solar?), a permanent ITC (debatable), and friendly utilities (now you know I am reaching - just kidding...kind of). As opposed to the other items on the solar developer wishlist, solar securitization is actually happening in real time. Pioneering companies like SolarCity and SunRun are paving the way with new securities offerings as we speak. The market is not huge, but has crested the $300M mark in 2015. This past January, SolarCity completed its first securitization of distributed solar loans, and achieved the industry’s first investment credit rating. Others will undoubtedly follow, if the way is clear. Back in June of 2015, we wrote about the idea of solar securitization finding more traction in the market. But, be careful what you wish for. While securitization may be the shiny new-ish finance toy for the solar industry, it is not a one-size-fits-all solution to finance (or refinance) projects. But be wary of the double-edged sword of solar securitization The solar industry rides on the shoulders of tax equity investors, at least until the ITC is phased out. As such, one must consider — how would securitization change the project finance equation? For one, securitization would expose tax equity investors to potential recapture of any unvested credits. Translation - backing a security with projects that do not utilize any tax equity will make the deal much simpler and more palatable. But who wants to leave money on the table? Luckily, the inverted lease was designed to tackle sticky tax equity issues like this and can be used to mitigate this recapture risk. As of 2014, SolarCity and SunRun started to create solar securities primarily of inverted lease arrangements. Problem solved. But that is not really the only issue that should concern project developers. The dark cloud hanging over solar securitization is that developers or third-party asset owners would have some of their upside undercut due to the fact that their equity in the underlying assets relies on retained value. Equity holders are always at the end of the cashflow line, but adding security holders to the mix places yet another claim on the project cashflows before equity holders get a piece of the pie. And that pie needs to be comprised of sweet, high-grade offtakers. As we all witnessed in the mortgage-backed security debacle, bundling lots of disparate (even toxic!) assets into a nicely packaged security may doop the market for a while, but it will come back to bite you. The same holds for solar-backed securities. Which means that not every residential or C+I solar project is going to pass muster as a security-grade product. This is one of the reasons that the initial transaction costs for creating a security are substantially higher than essentially any other project finance mechanism. High transaction costs along with the additional cost burden of compliance reporting can start to eat into that delectable low cost of capital, unless you have your ducks in the row. Some seriously good reasons to dip your toes into the securitization pool The first thing that you probably said when trying to sound smart about investing was “diversification.” I’ll wager the second thing you said (and you really had no idea what this meant) was “liquidity.” Diversification and liquidity are two of the primary ingredients in the low cost of capital cake mix. Diversification because high concentrations in terms of geography, offtakers, operations, and policy attract those pesky risk premiums that increase the cost of capital. Liquidity because it is the lubricant that allows markets to function and buyers and sellers to repeatedly engage in transactions. Add in a little sponsor bankruptcy risk mitigation and some public credit ratings to the mix and you have the makings of a very enticing offering to gargantuan fixed income institutional investor class. And what do institutional investors like more than anything? You guessed, boring standardization. All those legal and accounting fees that allow you to create boring, standardized securities also unlocks a velocity and scale of financing that could leave traditional project financing in the dust. Institutional investors have been invited to table, but will they dine? As we know, institutional investors have a big appetite, which, in the case of solar, has meant that they can only find the requisite scale in bigger utility-scale deals. Securitization could hold the key to allowing smaller residential and C+I projects to access lower cost capital from institutional investors. This issue of scale is a big one though. Securities of the size that would attract institutional investors have been few and far between. The question of the day is who can follow SolarCity and SunRun’s lead to bring the solar securitization market out of the hundreds of millions and into the billions. Related data points:

Further reading:

(Source: IEA) The International Energy Agency must love the Stanley Cup Playoffs because their recently published Global EV Outlook was full of hockey sticks! The hockey stick graph, you may recall, was popularized as a key piece of evidence supporting the existence of climate change. Rest assured, there will be no debate of climate change here. I am a deep believer in the appropriate use of sports metaphors to describe complex phenomena. The greenhouse gas emissions hockey stick graph tells about as simple a story as can be told about climate change. The hockey stick is a pithy way of showing how a creeping linear trend jumps into an exponential growth (or decay) phase. Our minds are wary of things that change exponentially. They are just not normal. That is because from one time period to the next, your worldview, let’s call it your umwelt, is dramatically different. Yet, as history shows, this Law of Accelerating Returns holds to key to understanding technological progress over the course of history. We see hockey sticks everywhere now. Some, we should get excited about like renewable energy deployment. Others, we might be wary of like the growth of the economy. Some indicate a phase shift, as in the case of the transition to renewable energy. Others might indicate a boom-and-bust cycle, with exponential growth followed by precipitous declines. The trick is understanding the underlying drivers of change. So, about EVs. Not long ago, EVs were very rare, too expensive, and only the most ostentatious environmentalist among your friends was even considering buying one. Skip ahead five years, and all of sudden, your umwelt has changed. The Law of Accelerating Returns has been hard at work. Now, you are starting to see EVs everywhere you look, EV charging stations are taking up the best parking spots, and your neighbor down the street likes to park their EV in the driveway to show it off while it charges. And this is just the beginning.  (Source: IEA)

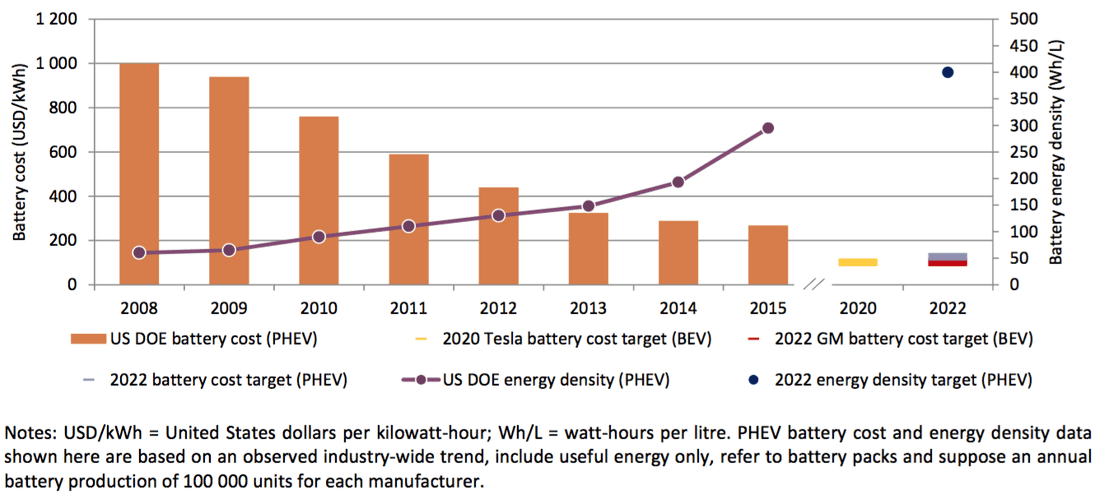

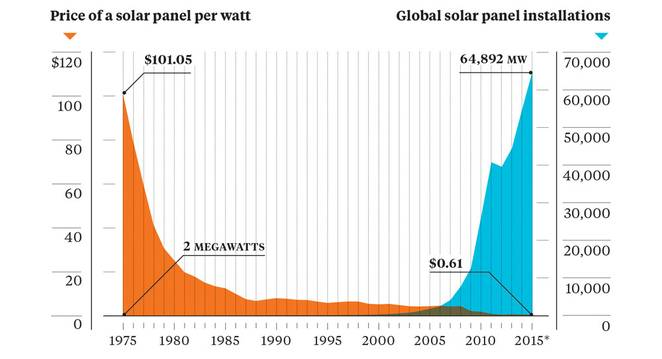

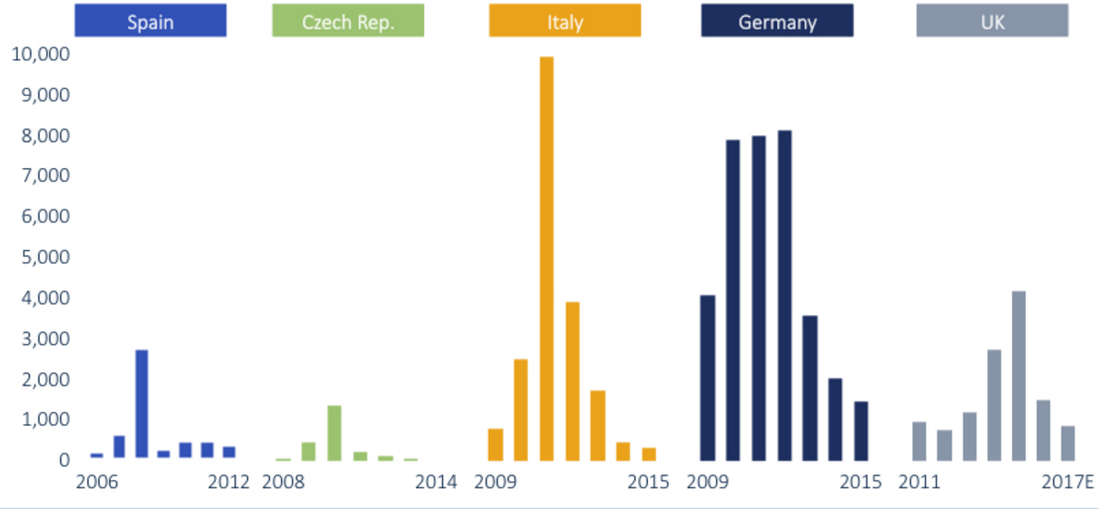

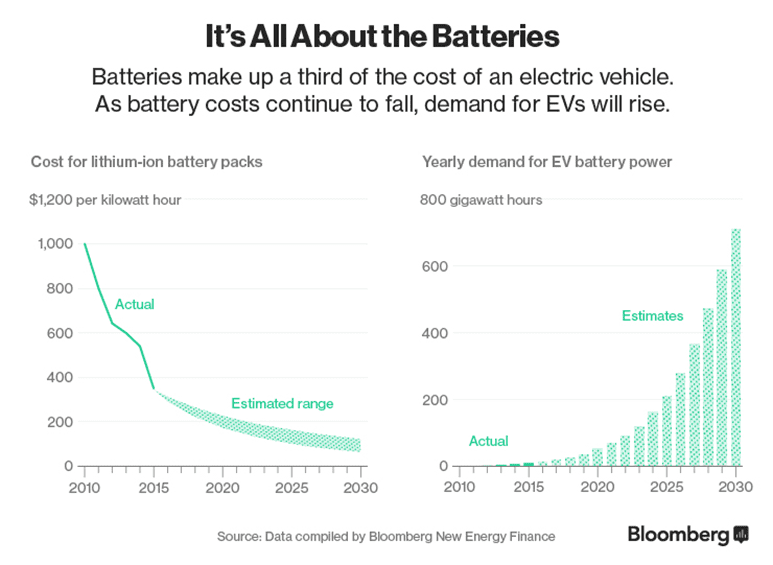

What changed? Well, largely it was a story of rapid technological innovation leading to dramatic cost reductions. The most important of these is with the battery, of course. As batteries make up around ⅓ of the cost of an EV, the increases in energy density coupled with the reduction in battery cost have started to bring EV costs down from the stratosphere. And not to dismiss, also helped alleviate the all-important “range anxiety.” We Americans do have a pastime of hitting the open (or congested) road without a worry until the next gas station. If battery technology continues its march of progress, look out for the Law of Accelerating Returns to come into full force in the EV sector. Feed In Tariff (FIT) programs have been the lynchpin of solar growth, but is it time to move on?  Source: Earth Policy Institute/Bloomberg Feed-in tariff (FIT) programs were designed to entice new entrants into the solar market during a time of learning and experimentation. Initially, they were designed as value-based instruments in which compensation was tied to various external benefits, such as avoided externalities (fancy term for coal plant pollution). But this model was a bit pie-in-the-sky, and left a lot of uncertainty and unpredictability on the table for investors and developers to navigate. The resulting high project financing costs ended up being a major deterrent to the type of catalytic growth that was hoped for. The real magic of the feed-in-tariff was unlocked when there was a shift to cost-based instruments, wherein a solar developer would get compensated for the costs of development plus some reasonable rate of return. The fixed-rate, long-term guarantee of cash flows was music to investors’ ears, and the solar market was off to the races all across the EU, China, India, and South Africa. Interestingly, no North American country has instituted a FIT program to date, and rather have opted for more circuitous policies such as Renewable Portfolio Standards. We now have a solid track record by which to evaluate the successes (and failures) of FIT programs around the world. On the surface, much of the success of solar markets worldwide is attributed to FIT programs. But there is a creeping concern that this success will not last much longer. FIT programs solved one problem by creating stable, long-term cash flows for solar projects, which could be underwritten and financed by savvy investors. This accelerated adoption and experimentation with different technologies and business models, but more importantly it sped up learning (decreases in costs due to experience or scale). In solving this market catalyst problem in the short term, governments left the door open in the long-term for gaming the system if and when solar prices (really LCOE) started to dip well under the FIT rates. And that is precisely what has started to happen. The bull rush to obtain legacy FIT program rates once technology costs plummeted has fueled a massive boom in solar. On the the surface, this seems like a great problem to have. More solar! But, this is a case of too much too soon, and governments are responding by pulling back on their FIT programs and leaving a wake of solar developers scrambling to make their projects pencil.  Source: GTM Research The European renewable miracle has been taking some nasty hits lately. Even the energy transition darling, Germany, has not been immune to the pervasive bust cycle that is spreading across the continent. What changed so quickly, you may ask? Well, it is the classic story of a good thing gone bad. The FIT programs that accelerated solar adoption so quickly in years past are now becoming the victim of their own success. Where they erred was in making the terms so enticing for so long that they ended up overheating the solar market. There is a delicate balance between creating an incentive to attract risk-taking early adopters and reducing or retracting the incentive once the economics of the market support broad participation. Or, in other words, they just let too many players at the table, and this time, the cards were stacked against the house. Governments underestimated the speed at which solar prices would fall, which left them in the undesirable position of having already committed to paying well above market prices. It was boom times for the solar industry, but it could not last. The graphs above look like tulip mania (if this reference eludes you, please read for some amazing dinner table chatter) for crying out loud. Germany had three years of putting over 8 GW online. Italy spiked in 2011 with nearly 10 GW of solar, only to plummet to under half of that in the following year. The UK has witnessed a remarkable growth in solar, only to cut the FIT program by 65% in one fell swoop. Similar patterns were seen in many other EU countries. And let’s not forget Japan, whose boom-bust cycle dwarfs those of all of the ill-fated EU countries already mentioned. Japan is still in the top 3 globally in terms of annual solar capacity installed, but is headed for a protracted decline in solar over the years to come, again due to an over-aggressive FIT program. But FIT programs are so simple and elegant. What alternatives exist, you may ask?  Source: GTM Research Letting go of a good thing is hard, especially for an industry like solar that may suffer from a tinge of PTSD from the head-spinning boom-bust cycles of the past decades.

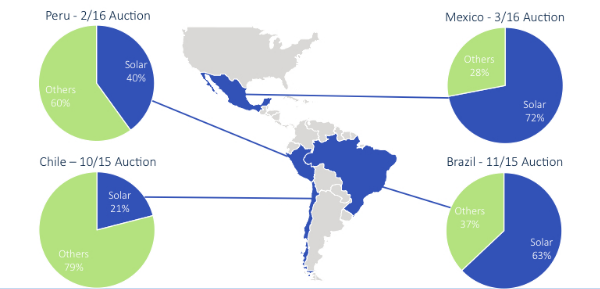

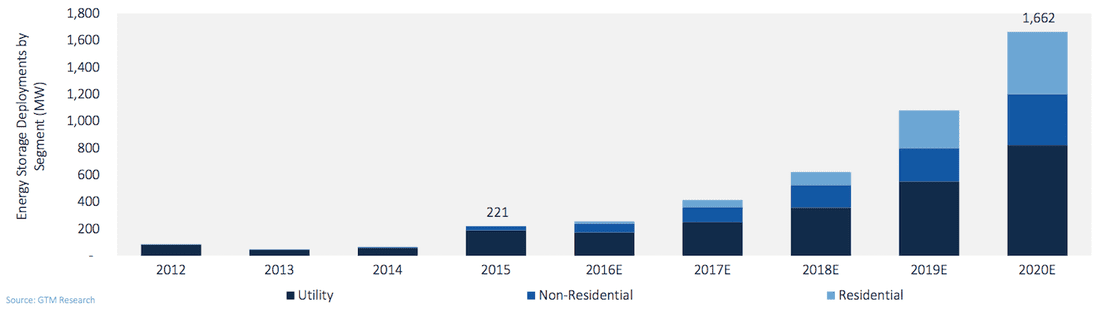

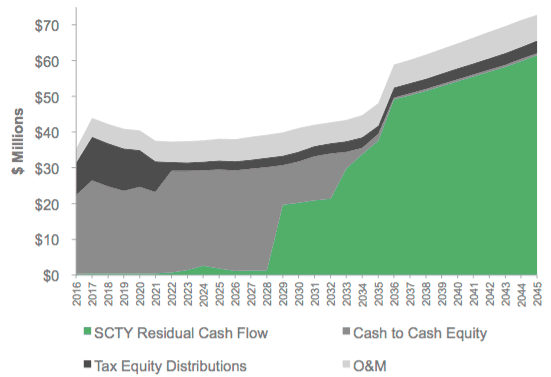

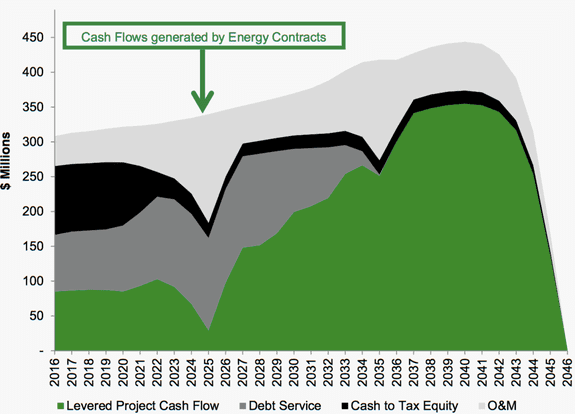

After all, with the FIT structure solar did not necessarily have to directly compete with other generation technologies. A decade ago, that was just fine because solar would not have been competitive. Solar needed an incubation period to slide down the learning curve to lower, more competitive prices and meaningful deployment scale. Now that solar can tout itself as being one of the most cost effective electric generation technologies out there, there needs to be an increasing willingness to actually compete in markets with other generation technologies. Latin America has started to buck the FIT model in favor of an auction process in which solar competes with other generation technologies, both from independent power producers and incumbent utilities. This has helped feed a boom in Latin American solar, as it turns out that solar can beat out nearly all other generation technologies on a pure LCOE basis. Nearly three quarters of new capacity additions in Mexico will come from solar, easily more than 1 GW. Brazil is in the same league. And various EU countries and India are also doubling down on auctions. But, auctions are not a panacea. We have all seen auctions in the movies, and the meme of the irrationally exuberant bidder going well beyond their true willingness (or ability) to pay in order to secure the prize. While we all hope that power producers are somewhat more measured and rational in their approach to bidding in these markets, there remains the possibility that competing in auctions may drive prices down quickly to unsustainable (even unprofitable) levels. In fact, some early evidence in the auction tea leaves is that even these markets can overheat as bidders aggressively pursue market share. On the one hand, it may be good for business in the short-run, and auctions may effectively accelerate learning and cost reductions. But, on the other hand, auctions run wild may undermine the long-term viability of the ecosystem of power producers feverishly competing to keep up with the Joneses to survive. Exuberant bidding to support short-term growth is not a phenomenon that should feel altogether unfamiliar, as it is precisely what drove SunEdison to bankruptcy. Further reading: As Feed-In Tariffs Wane, Auctions Are Enabling the Next Wave of Solar Cost ImprovementsFeed-in Tariff: A policy tool for encouraging the deployment of renewable energy technologiesInnovative Feed-in Tariff Policy Designs that Limit Policy Costs A Policymaker’s Guide to Feed-in Tariff Policy DesignFeed-in Tariff Policy: Design, Implementation, and RPS Policy Interactions Annual U.S. Energy Storage Deployments, 2012-2020E  Can somebody throw the energy storage industry a bone? It is a little known fact that the investment tax credit (ITC) was a key catalyst for the emergence of solar as an essential component of the future electric grid. Well, not really. That statement borders on platitudinous. It should be no surprise, then, that the energy storage industry is angling for similar treatment by the almighty tax deities at the IRS. Energy storage, after all, is touted as being a key enabler of high levels of renewable energy penetration. Handcuffing energy storage will only undermine the grid integration of solar and wind down the line. So, can the energy storage industry get a bone here? Yes, it is a relatively nascent industry (at least in battery technology) undergoing a rapid period of technological learning and experimentation. But out of the frey, we are starting to see some dominant technologies and applications emerge within functional markets. While lithium ion batteries are the current industry darling, there are many other viable storage technologies including stored hydropower, which still dominates the energy storage field overall. In the periphery, there are a host of other storage technologies incubating in R&D facilities, start-up companies, and corporate technology giants. Perhaps in response to the eventuality of energy storage becoming a key component of the electric grid, the IRS threw the energy storage industry a bone, but it came with some strings attached. Energy storage already qualifies for the ITC, right? Yes and no. Yes, energy storage already qualifies for the ITC, but no, it is does not qualify under all circumstances. Energy storage that is powered by solar or wind qualifies for the ITC, though with some caveats related to the extent to which grid electricity is also used to charge the energy storage system. This is where things get a little tricky. Assume that you have an off-the-grid solar + storage facility (a grid defector!). Simple - the ITC applies, and you can get on with your homesteading. But for all grid-connected systems, there is an upper limit to how much charging your storage system can receive from the grid and still qualify for the ITC. That magic number happens to be 25%, meaning that a whopping 75% of energy storage charging needs to come from solar. That is just the minimum standard for qualifying for the ITC. The full ITC benefit is reduced in proportion to the amount of energy input coming from the grid, so anything less than an energy storage system charged by 100% solar will receive less than the full ITC benefit. Add to string the fact that solar + storage projects are benchmarked to the first year’s solar power output for the subsequent four years of the tax benefit, which means that any reduction in solar output will be penalized with a lower ITC benefit. And all of this was articulated in a private letter, which does technically establish a precedent, but is a somewhat opaque way to communicate what could be a substantial benefit to the energy storage industry. See here for a clever dive into the details of solar + storage. Stand-alone energy storage ready for an ITC vaccination It is clear that coupling solar (or wind) with energy storage is a good idea, and will be done with increasing frequency over time. It is also clear that energy storage will not and should not be relegated to the sidelines of the ITC prom waiting for some attention from the solar and wind dancers on the floor. In fact, it is imperative that energy storage be granted a clear and clean invitation to the ITC prom independent of their relationship to solar and wind, when and where appropriate. If the aim is to reduce barriers to more energy storage development providing flexibility and ancillary services to the grid, then there is a pretty obvious argument to be made about the need for a little ITC vaccine for stand-alone energy storage. Why a vaccination? Well, energy storage, like many emerging clean energy and smart grid technologies, could benefit from an inoculation against investor skepticism. There is no shortage of bullish projections about the future of energy storage, yet many project developers find themselves searching for capital. Even when they land upon a willing investor, their investment often comes with a heavy cost of capital penalty due to the perceived risks and uncertainties associated with energy storage projects. Not unjustified on the part of the savvy investor in search of those ever elusive risk-adjusted returns. But also not the formula for ramping up energy storage deployment, which, after all, is the key to sussing out technologies, business models, and financing structures. Learning, in other words, which is exactly what the ITC has been doing solar all of these years. Roping in stand-alone energy storage projects into the ITC framework could be just what can get investors over the hump of really going gangbusters on energy storage. SolarCity Residual Cash Flows  (Source: SolarCity) SolarCity is still the prettiest girl at the dance SolarCity is without a doubt the most trend-setting solar finance company on the planet. They are a vertically-integrated, distributed solar superpower that seems to grab newsworthy headlines on a weekly, sometimes even daily basis. On April 6th, SolarCity announced a $150 million non-recourse financing facility with Credit Suisse to support the deployment of new commercial PV and energy storage assets. The very next day, the company announced a tax equity closing of $188 million from Bank of America Merrill Lynch for residential solar deployment. At first glance, that amount of activity could worry investors that SolarCity is pursuing too many verticals in parallel without focusing efforts on the most profitable segments. This type of investor sentiment is currently relevant considering that the mainstream explanation for SunEdison’s bankruptcy is simply that the company took on too much debt while drinking water from several different fire hoses. I would argue that SolarCity is similarly extended in terms of asset classes, but they have been consistently more savvy than SunEdison in regards to monetization. Unlike SunEdison, SolarCity has maintained a focus on creative financial engineering that produces near-term cash flows to sustain the upfront capital outlays required by today’s solar finance institutions. John Hancock to the rescue? On May 4th, SolarCity completed a $227 million “cash equity” financing with John Hancock Financial for approximately 200 MW of operating solar projects. This transaction serves as the most recent example of SolarCity monetizing the underlying cash flows associated with the company’s long-term power purchase agreements with individual off-takers. Unlike the two transactions in April, John Hancock’s injection is not a critical component of the capital stack to initially finance the development and construction of solar projects. This cash equity transaction is regarding solar assets already in operation, across three segments (residential, commercial, industrial), and spread between 18 U.S. states. Within this portfolio, the average FICO score for residential customers is 744, and most of the commercial off-takers are national retailers. News flash: large institutional investor is attracted to diversified portfolio with virtually no risks. Which begs the question, why did SolarCity take a discount on future cash flows and sell now? Just like every other solar company in the 3rd party ownership space, SolarCity is bleeding cash due to the high customer acquisition costs and needs to display short-term revenue to keep shareholders confident in the company’s long-term value proposition as a distributed power provider. See here for a current perspective of the 3rd party ownership climate in the U.S. Despite the success of matching low-risk solar PPA payments with an institution that is all too familiar with generic annuities, SolarCity now has some longer term expense considerations to overcome. They are still responsible for the O&M expenses related to servicing the 200 MW of assets, and they’re responsible for expenses related to decommissioning the PV systems if the PPA term is not extended. As part of the cash equity transaction, SolarCity retains the rights to 99% of the post-PPA cash flows, but it's anyone’s guess how likely it is that post-PPA revenue streams will be realized. Although this transaction structure is new and newsworthy, it’s just another tool in the solar finance industry’s toolbox to monetize future cash flows. SolarCity Cash Flows  (Source: SolarCity)

The jury is still out on whether solar and securitization are a match made in heaven Asset-backed securities have a negative connotation to the layperson, to say the least. But there’s no denying that securitization can play an important role in increasing investor access to specific asset classes, as well as raising affordable sources of financing in capital intensive industries, like solar energy. The key word here is affordable. SolarCity has now sold six tranches of solar-backed securities over the last 30 months, including $49 million on March 1st when the weighted interest rate was almost two percentage points higher than a sale just 12 months earlier. The rise in SolarCity’s cost of capital is troublesome and may cause the company to abandon the new strategy and seek out alternative forms of financing. It’s clear that the 'SunEdison effect’ is having a real impact on investor comfort with the reliability of long-term solar contracts, despite the incredibly low default rates experienced by SolarCity (and others) to date. As long as default rates remain very low and companies continue to drive down the cost of customer acquisition, the opportunity to sell the underlying cash flows of solar projects will remain for both public and private developers.  (Source: GreenTech Media)

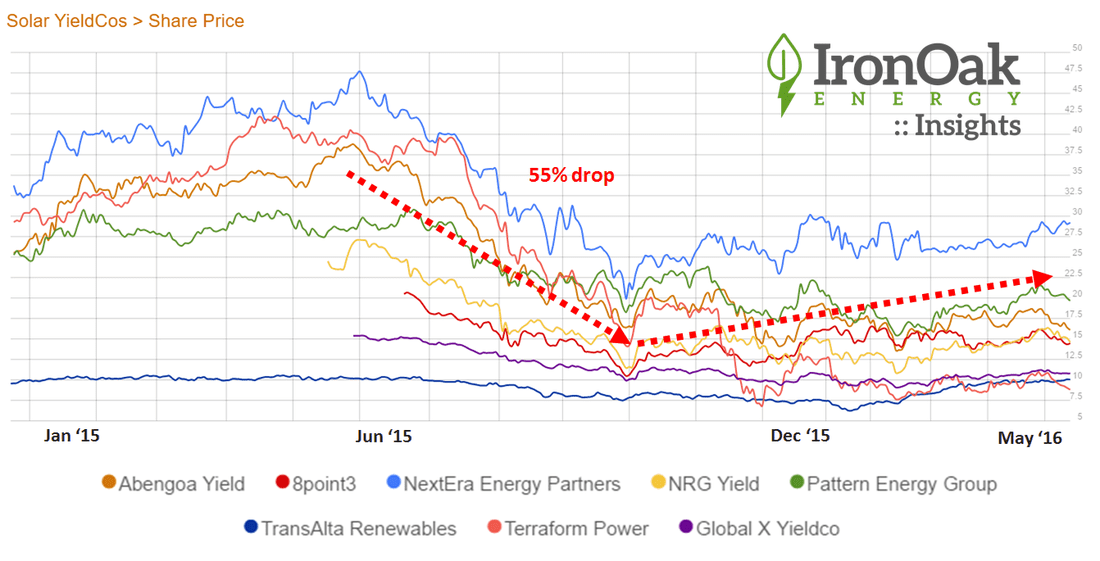

Everyone likes lists. Lists are candy for our mind. Give me a Top 10…, and my mind naturally embraces the elegant hierarchy, 1 better than 2, and way better than 10. A simple rubric for a messy world. So, it was with some curiosity that I digested Ernst & Young’s Renewable Energy Country Attractiveness Index. See renewable energy is complex, and lists are simple, so this makes a good pairing. Like red wine (complex, hence - see, swirl, smell, sip, savor) and chocolate (simply delicious). What do we find? Clearly, United States #1! As if… The BICS - Brazil, India, China, South Africa (sorry Russia) - are all in the Top 11 and are the big upward movers. Just fascinating considering the sheer scale and dynamism of those economies. Latin America is on the rise with Chile, Argentina, and Mexico all in the Top 20 (and Summer Olympics in Rio!). And Europe is increasingly looking like a basket case. Germany, France, United Kingdom, Netherlands, and Belgium all dropped spots. Regrettably, some petulant factions within the EU are backpedaling on much of the industry-paving progress of the previous decades. What a mess. Sophisticated European investors will likely migrate into international renewable markets. After all, a 4% unlevered IRR is not going to winning any beauty contests. The ascendant BICS and Latin American countries are the investor darlings of the moment. But the renewables investment landscape is not as simple as that. For this, we another list! The Venture Capital & Private Equity Country Attractiveness Indexmeasures the...well, it basically says it in the title. Rest assured, United States #1! As if… But some mind-tickling asymmetries arise between these two lists. Ahhh -- when lists tell contradictory stories, it makes us to have think! Some countries have an attractive investment environment for renewable energy but an overall weak (or altogether suspect) environment for VC/PE investors. Take, for instance, Argentina. 18th for renewable energy investing, but a lowly 64th for VC/PE investing. Lest we forget - the economic scene in Argentina can get a little wobbly at times. A similar pattern holds for South Africa, Brazil, Morocco, Egypt, and others. All great places for renewables, but a little shaky for investment in general. So, I leave you with the holy grail concept of risk-adjusted returns. How might you adjust returns to account for risk? Well, that is more of an art than a science. No simple list can tell that story.  Last year, IronOak Energy’s investment advisory practice had some challenges competing against yieldcos on behalf of our solar investor partners.

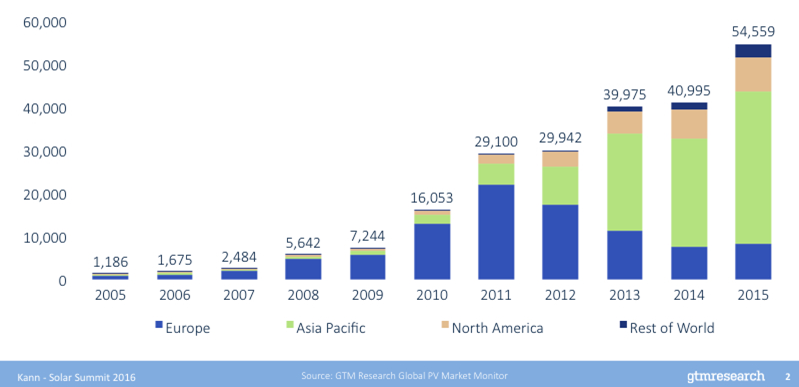

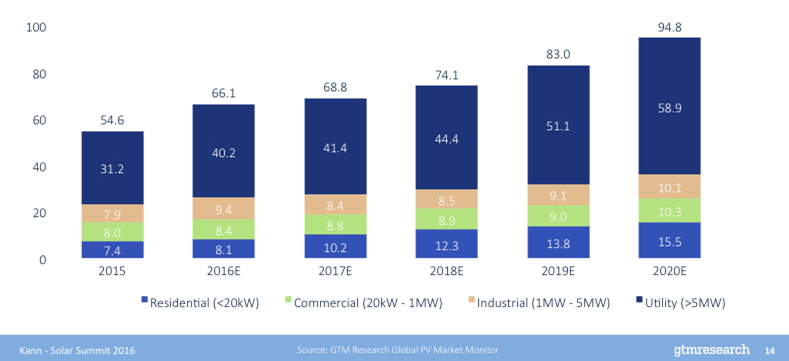

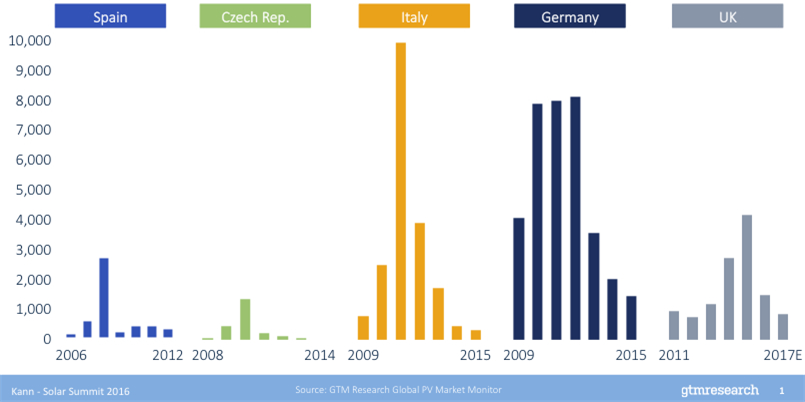

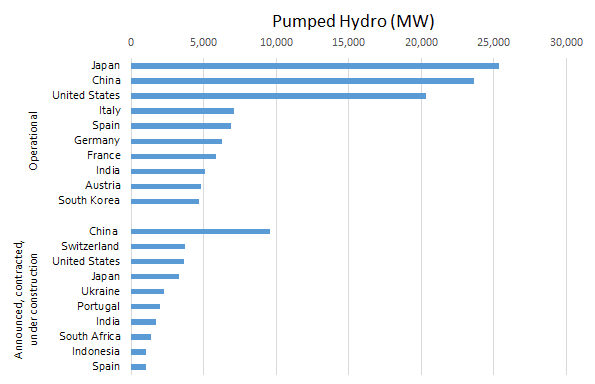

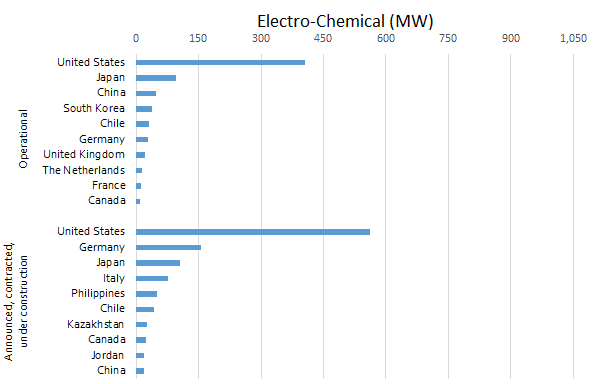

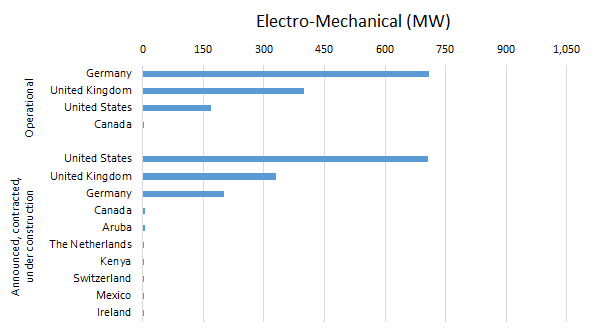

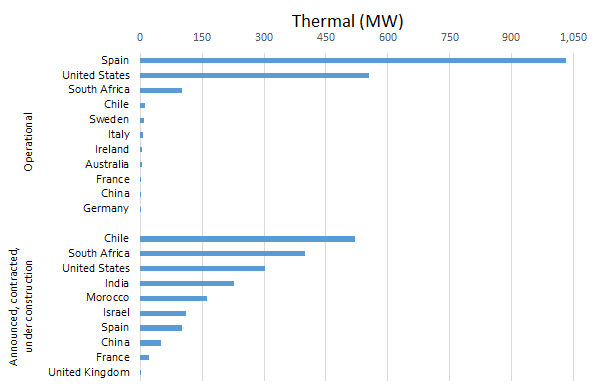

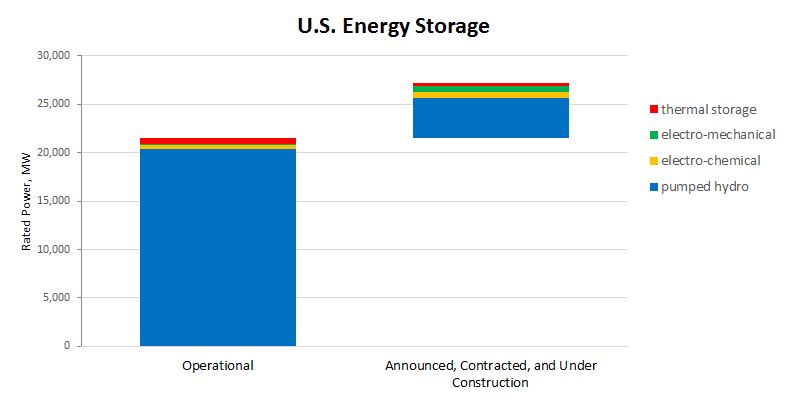

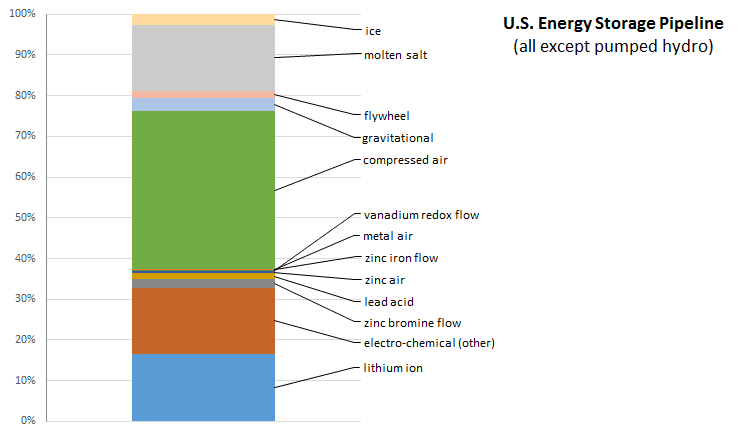

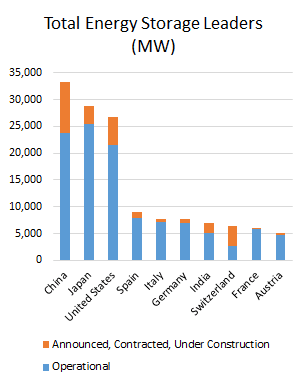

We kept abreast of the yieldco’s up/down trends at IronOak’s stock chart. They were offering what some called “a stupid low” cost of capital. That was sometimes said as a judgment on the the yieldco business model. Other times it was a said with a slight jealousy: “I wish our yields were still attractive at those levels so we could win more deals with predictable long-term cash flows.” Developers licked their lips. Those low-yield requirements made their discounted cash flow models really sing. As we all know, in late summer last year, both developers and yieldcos bought their share of Kleenex boxes. But this was great news for private equity and helped improve their returns. Many claimed the model was broken. We thought that was shortsighted. Sometimes innovators hit a speedbump, but then they hit the accelerator again. Now several yieldcos are getting ready to go to public markets. It’s not time for them to be big-time project buyers at attractive costs, but that time will come. For now, private equity still rules. Everybody loves solar. Well, except for those who think solar panels cause cancer and prevent plant photosynthesis. (Seriously. Summary here.) But we digress… Solar projects makes for great headlines, company brochures, and dinner party conversation. But are these good infrastructure investments? (Let’s keep investments in companies separate for now. Venture capital and public equities are very, very different beasts.) If you ask Warren Buffett, he has already answered, with more than $15B invested in solar (and wind) projects. I hear that he’s a pretty good investor, so that says something. And if you look at the two graphs below, then you should agree that the market is trending up.   Predictable markets, especially at the utility scale, with 5-year projected growth of 1.9x versus 2015. Residential solar also looks strong at 2.1x growth over the same period. However, commercial and industrial markets may only increase about 1.3x, with one-off credit risks that challenge scaling. So, go long on U.S. solar, right? Broadly, yes, but the devil is in the details. Picking the right market, site, developer, offtaker, and finance model will, of course, make or break the deal. And these are just U.S.-specific projections. The world is a big place. Now let’s look at other countries’ experience. Summary: It’s not predictable year-over-year growth for many years. The graph below tells a different story: Solar project investments are better defined as taking a ride screaming with joy and pain on the “solar coaster.”  So, short solar markets in certain countries? Well, maybe, though not technically easy to do since this is mostly private, not public, equity. In summary, should you go long or short on solar infrastructure? Um...yes, let’s grab a beer and talk in more detail. In a previous blog, we reviewed how pumped hydro storage still dominates all storage technologies in the United States, with the existing capacity of 20,356 MW expected to grow by 20% with an additional 4,150 MW. Thermal storage is projected to add 302 MW of rated power to an existing 553 MW (an increase of 54%), electro-chemical approaches will add 602 MW to the existing 405 MW (+148%), and electro-mechanical technologies will add 706 MW to the existing 169 MW (+418%). How does the global picture look? We refer again to results obtained from U.S. DOE’s Energy Storage Database. The figures below show the somewhat dramatic transition between the “old” (existing operating capacity) and the “new” (projects that have been announced, contracted, or are under construction) in energy storage projects around the world. Old school made new: A pumped hydro renaissance? Pumped hydropower looks at the new-fangled batteries and other technologies coming out with regularity, and feels like a person out of place at a hipster bar. But this technology, which has been around since it was first used in Italy and Switzerland in the 1890s (soon after the world’s first hydroelectric dam began operations in Wisconsin in 1882), remains the overwhelming leader in the energy storage arena, both in existing and future capacity. Indeed, with newer variable speed pumps that are better able to coordinate with electric grid needs, a pumped hydro storage renaissance may be under way.  (Source: DOE Energy Storage Database, data downloaded 4/29/16) From the figure above, Japan, China, and the United States are the clear top three in this area, and each are making significant new builds along Switzerland. The scale of pumped hydro is impressive, as new projects in less developed countries such as Ukraine and India represent a higher capacity addition than those from all other technology types and all other countries. All in on the newer energy storage technologiesThe electro-chemical category includes all of types of batteries (e.g., flow, lead acid, lithium ion, metal air, sodium-based, and zinc air) as well as electro-chemical capacitors. From the chart, the United States is the clear leader in this technology type, and its capacity is expected to more than double. Other nations that have already bought into battery storage are projected to buy in even more, such as Japan, China, and Chile, with relative newcomers like Italy, The Philippines, and Kazakhstan jumping in strongly for the first time.  (Source: DOE Energy Storage Database, data downloaded 4/29/16) Current electro-mechanical storage applications, which include compressed air storage, flywheels, and gravitational systems such as railcars, have been tried at scale only in Germany, the United Kingdom, and the United States. And while these three top the areas with new capacity coming on, a larger set of new countries are testing the waters, though admittedly at a very small scale.  (Source: DOE Energy Storage Database, data downloaded 4/29/16) Thermal storage (e.g., ice, molten salt, and other approaches) has also been dominated by three countries—here, Spain, the United States, and South Africa. Here too the technology is diffusing across a much wider array of countries, with most outside of the original top three starting basically from scratch.  (Source: DOE Energy Storage Database, data downloaded 4/29/16) Finally, by way of comparison to the other energy storage approaches, global hydrogen storage is miniscule, as the total of listed projects includes 2.7 MW in Germany and 0.2 MW in France. The method is straightforward—excess electricity is sent through a Proton Exchange Membrane (PEM) to electrolyse water into hydrogen and oxygen. The hydrogen can be stored on-site (as with a “wind to hydrogen” concept for wind turbines) and then later either sold and fed either into pipelines for grid electricity production or used directly for on-site electricity generation in a fuel cell. (It can also be sold for use in fuel cell vehicles, or as an input in ammonia production). Although the base is low, this method of storing energy is expected to more than double in global size, with Canada, Italy, and Germany developing an additional 2, 1.2, and 0.8 MW, respectively. Many future energy storage leaders are starting from scratchIn the final two graphs below, we see the total rated power of energy storage by the leading countries, including both existing capacity (in blue) and capacity expected to come on line soon (orange). As noted before, pumped hydro skews the results. At left, which includes pumped hydro, China, Japan, and the United States will remain the dominant players in energy storage overall, with significant capacity additions expected for these countries as well as Switzerland, which will more than double its storage capacity. Other nations in Europe—like Spain, Italy, Germany, France, and Austria—will be relatively stable when it comes to total energy storage.

(Source: DOE Energy Storage Database, data downloaded 4/29/16)

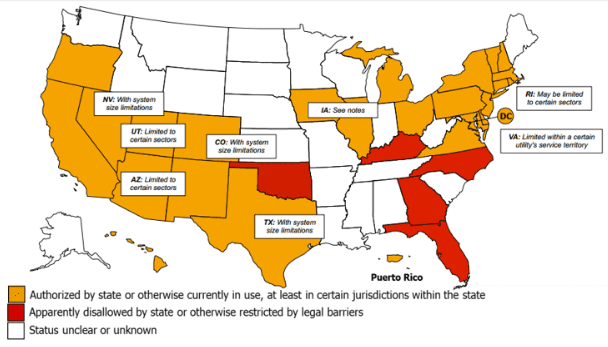

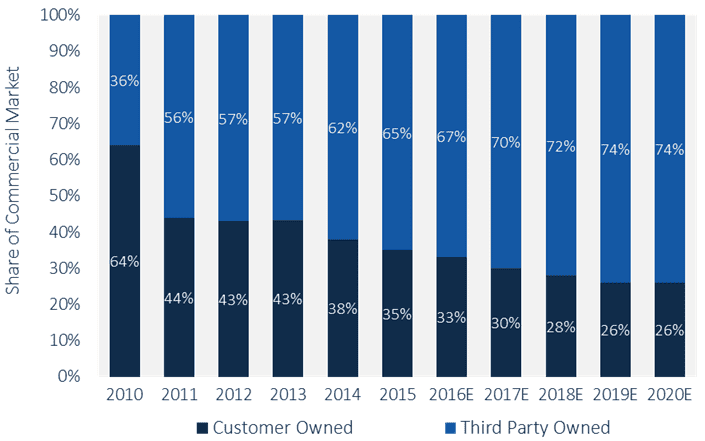

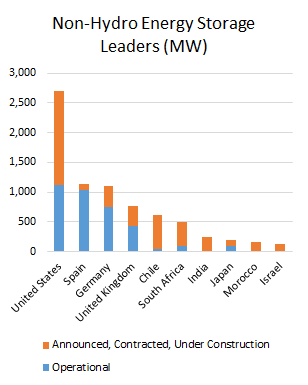

At right, taking out the pumped hydro data, notice first that the y-axis scale has dropped by an order of magnitude! In this non-hydro arena, the United States is the clear global leader. Also notable is that many countries are almost starting from scratch to build energy storage capacity in these non-hydro technologies, including Chile, South Africa, India, Morocco, and Israel, while Germany, the United Kingdom, and Japan will be making significant additions. The lessons? If you’re in the battery or other non-pumped hydro storage areas, be aware that efficiencies are improving in pumped hydro that may be worth paying attention to, at least at the international level. And of course if you’re in the pumped hydro field, you have some new competitors as well. Further reading: States Authorizing 3rd Party Power Purchase Agreements  (Source: DSIRE) First, the bad news: policy battles over 3rd party ownership of solar muddy the waters Just pile it on top of the other cadre of unenlightened policies that North Carolina is behind these days. Yes, North Carolina, my home state, is making headlines for another boneheaded public policy move, this time regarding the highly controversial topic of… solar! The NC Utility Commission (NCUC) recently upheld a law that prevents 3rd party ownership of solar projects. The case that brought the issue into the public limelight concerned a whopping 5.25 kW installation that the environmental advocacy group NC WARN had built to provide electricity to a local church. The two parties signed a 3-year PPA at a discounted rate, which, doing some quick math, might have provided around 23,000 kWh per year valued at around $4,000 or so for the life of the PPA based on prevailing rates. Well, Duke Energy was not having it! The biggest utility in the nation, valued at over $55 billion, opposed NCUC and beat down this encroachment on their business. And just to make an example out of NC WARN, they were slapped a $60,000 fine, which is around 15x more than the electricity that would have been sold in the PPA arrangement. Duke Energy is not entirely foolish to help combat the proliferation of 3rd party ownership, but their choice to do so goes against the countervailing inertia moving us into a more distributed energy future. Duke Energy will surely be fighting an uphill battle on this issues for years to come. North Carolina is not alone in this business of prohibiting 3rd party ownership of solar projects. The state stands in solidarity with Florida, Kentucky, and Oklahoma, which sounds like a NCAA Final Four (pause for sad memories of UNC’s recent loss). Unfortunately, that is where the commonalities stop, because, in the case of solar, competition (in this case with incumbent utilities) is prohibited. The game is rigged in favor of utilities with virtual, if not actual, monopoly power, something that supposedly goes against federal trust law. As a North Carolinian, it is with deep regret that I admit that South Carolina (!) recently passed legislation to allow for 3rd party ownership of solar projects. Georgia has done the same (although not accounted for in the map above). So, take heed, NCUC, your neighbors to the south are upstaging you on the transition to clean energy. Well done. Just add it to the list... On a positive note, 3rd party ownership trends are helping to unlock potential in the behind-the-meter corporate solar market Commercial PV Installations by Ownership Structure  (Source: GreenTech Media)

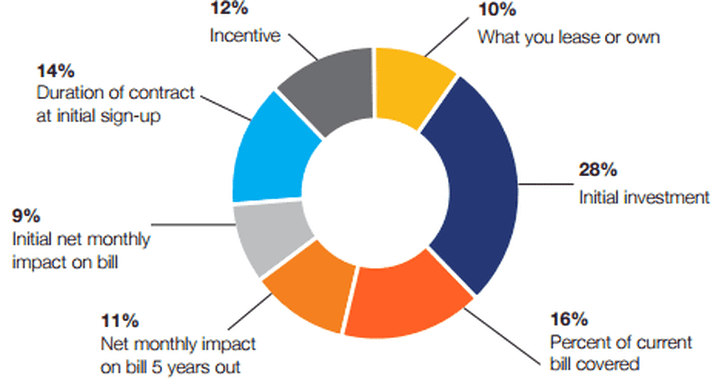

With all of the pushback on 3rd party ownership of solar in certain states, one has to consider what might happen if this was allowed. Well, one thing is for certain - corporations would be buying into solar, and likely in a big way. This is, after all, the situation that we see in states that allow 3rd parties to sell electricity from solar projects to corporations. As solar has become more competitive with prevailing retail electricity rates, corporations have started to see locking in stable electricity prices from solar as a complete OpEx no-brainer. Though a handful of corporations opt for the direct ownership and financing approach, the vast majority are seeking 3rd party owners to provide them with solar solutions. And those trends are expected to continue, as shown in the projections above. I go into further detail on this topic in a previous blog. So, what is to like and dislike about this arrangement? One the one hand, 3rd party ownership does fundamentally decentralize the electricity provision business, especially as behind-the-meter applications become more reliable and cost-effective. That is seen as a threat to incumbent utilities who have historically been the end-all-be-all of power provision. Setting aside utility concerns for revenue loss, the real question is whether utilities can meet the needs of large offtakers looking for distributed power solutions. The answer is yes and no, depending on the utility. It seems like 3rd party solar ownership is here to stay, so what’s the catch? This gap in the market opened the door for an explosion of independent power producers, offering a staggering array of behind-the-meter solutions to customers. Some of these we have come to know well - SolarCity, SunRun, Vivint, etc. But there are many others vying for a place near the top of the pecking order. So, what of the risk of working with these solar companies? It really boils down to counterparty risk. Two parties really have to believe that each other will continue to exist as solvent enterprises for decades to come. Not a trivial proposition from the standpoint of a corporation analyzing the evolution of the solar industry, perhaps for the first time. Clearly, the ongoing tumult of the growing solar industry (aaahh SunEdison chuuu) brings to light the sometimes ugly process of picking winners and losers. It would not be unreasonable to assume that the landscape of solar companies out there will continue to change for some years to come. So, why should you sign a decades-long PPA with a company that may not continue to exist for the next five years? That is the question of the moment. But if the data are any indication, corporations are becoming increasingly comfortable with signing long-term PPAs with 3rd party solar power producers, not to mention homeowners. So, back to the original story, what are the NCUC and Duke Energy, in a classic “tail wagging the dog” relationship, so worried about? It might be the “adapt or die” mantra that has been reverberating around the industry since the collapse of several European utility titans. But rather than adapting, they are digging in their heels on an issue that 46 other states in the U.S. have already come to an agreement on. If there is anything that we can agree about the future, it is that change will be ever present. 4/30/2016 It’s the offtaker, stupid! What we should have known from the start about community solarRead Now What’s new? As many have predicted, community solar continues its nationwide growth. We previously discussed the fourteen states that have adopted specific enabling legislation for community solar. With the growth in business potential, more and more states are working to adopt or revise policies to accommodate this new model for distributed energy generation. According to the NC Clean Technology Center, in Q1 2016, seven states have considered, amended or clarified rules governing community solar programs; and in states that are slow to respond, utilities are taking the lead, submitting proposals for community solar programs without a specific enabling legislative framework in place. According to SEPA’s recently released report, “Community Solar: Program Design Models,” there were 68 active programs in 23 states in the summer of 2015, with many more programs being planned. Geographic Distribution of Community Solar Projects  (Source: SEPA) In New York, EnterSolar started construction of the first community solar project in the state. Relatively small in terms of capacity (less than 1 MW), the project is developed under New York’s first phase for community solar development that limits development to areas with the highest grid locational benefits and to low-income communities. This month New York enters the second phase of the program that allows for full implementation of net metered community solar projects across the state. Many developers are already working hard to secure development contracts, and even the city of New York has introduced a municipal plan to promote community solar developments within city neighborhoods. What’s wrong? Nothing is wrong with community solar. On the contrary, we think that community solar is awesome. However, despite its great potential to unlock solar energy to more than half of electric consumers in the U.S., and although it is gaining traction nationwide, development rates for community solar are nevertheless 20% lower than expected. Even in states that have addressed management structure and regulatory uncertainty concerns projects are still not springing up as one would have expected. So what is it? Why aren’t we seeing more community solar projects? It’s the offtaker, stupid! The reality on the ground is that developers and utilities are still struggling with selling community solar to customers. Relatively complex in structure and less known than other models of distributed solar generation, community solar is a hard sale. Customers are wary of entering into unfamiliar financial adventures involving multiple parties, especially when the transaction involves an upfront investment as is the case with most community solar schemes. Part of the challenge lies with the fact that customer attitudes to community solar vary. While some programs are fully subscribed and thriving, others are underachieving. Many have tried to identify the winning set of program features that makes a community solar project appealing, but because regulatory frameworks, transaction structure, and management schemes vary greatly from one project to another, identifying best practices from existing projects has proved to be an elusive task. However, a recent study conducted by Pacific Consulting Group, might have finally revealed the answer to the question of what makes a community solar project successful. Taking a creative approach to solving a persistent problem, PCG focused on customers instead of projects. PCG conducted a market survey among potential offtakers in eight community solar states, asking respondents questions aimed at identifying how market acceptance of community solar changes with project features. Unsurprisingly, the number one factor in customer acceptance is initial investment; projects that do not include an initial investment or require only a small upfront investment are highly valued. The second is percentage of electricity bill to be covered by the investment; the lower the percentage of the bill covered, the less attractive is the project. Together, the two attributes account for 20% of total importance. Other interesting findings are that customers value savings five years out as more important than immediate savings (suggesting that customers are not intimidated by the long-term commitment associated with community solar), customers are largely indifferent to what they lease or own, and are not persuaded by incentives other than the potential payback (e.g., late fee forgiveness). Relative Importance of Seven Program Attribute on the Decision to Adopt Community Solar  (Sources: PCG; SEPA)

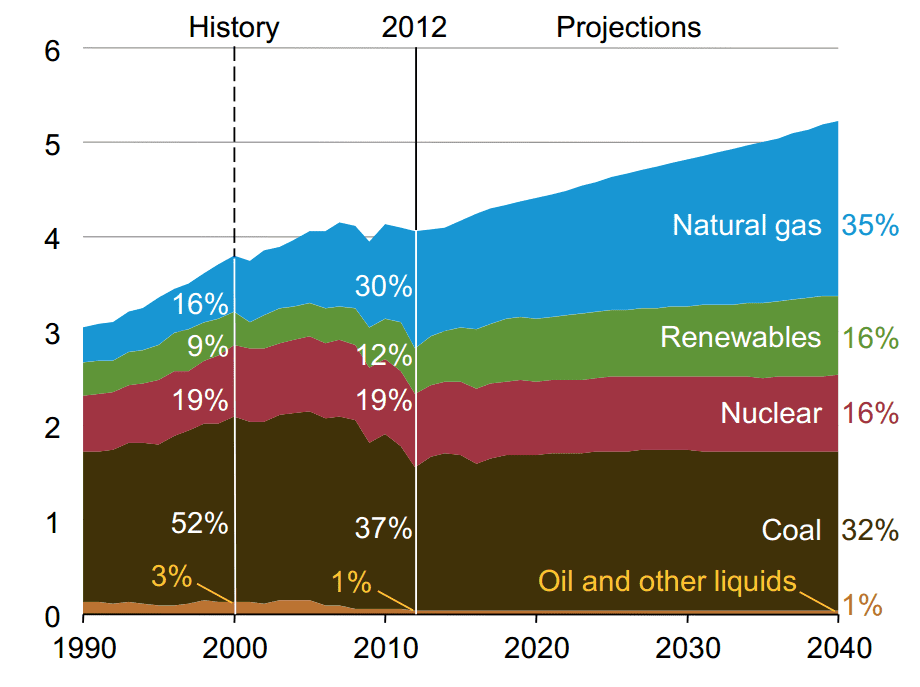

The study also measured customer responsiveness to marketing approaches and revealed interesting trends among communities. The most important findings are that messages emphasizing customer ownership and individual economic gains resonate better than messages emphasizing conservation or “green” considerations. Utilities, nonprofits, and solar organizations enjoy better credibility and therefore have better prospects in influencing potential customers than other entities or individuals (indicating the value of business partnerships). Also, personal messages targeting individual customers are more effective than mass media (with a message on the utility bill being the most effective form of customer engagement). All I want is peace of mind Understanding how to approach customers and how to tailor transactions in a manner that is appealing to potential offtakers is very important for the continued growth of community solar, but it is not enough. Even after we have addressed project features, payout structure, and marketing strategies, we still need to find an entity that will manage the project once it is operational, and long-term management of multi-party endeavors is costly. Some states have tried to address this concern by introducing an intermediary special purpose entity responsible for aggregating membership interests and managing the relationship with the local utility. But the question of cost and management remained largely unanswered, at least until now. Responding to market needs, community solar management firms are emerging. Firms like Clean Energy Collective offer management platforms that ease operations, reduce costs, and give offtakers, investors, and utilities exactly what they need - peace of mind. If you were to form your opinions on renewable energy from Energy Information Agency (EIA) reports and datasets, you might be under the illusion that we are reaching a peak in distributed solar and wind development, among other non-hydro renewables. For those less familiar, EIA provides a robust dataset of energy consumption and costs going back to 1960 in many cases, which they supplement with forward-looking projections to 2040 in their Annual Energy Outlook. Though they are considered a non-partisan research branch of the U.S. government, their data seems to represent a particularly pessimistic, and at times downright false, perspective on what is happening with renewable energy development.  (Source: Cleantechnica)

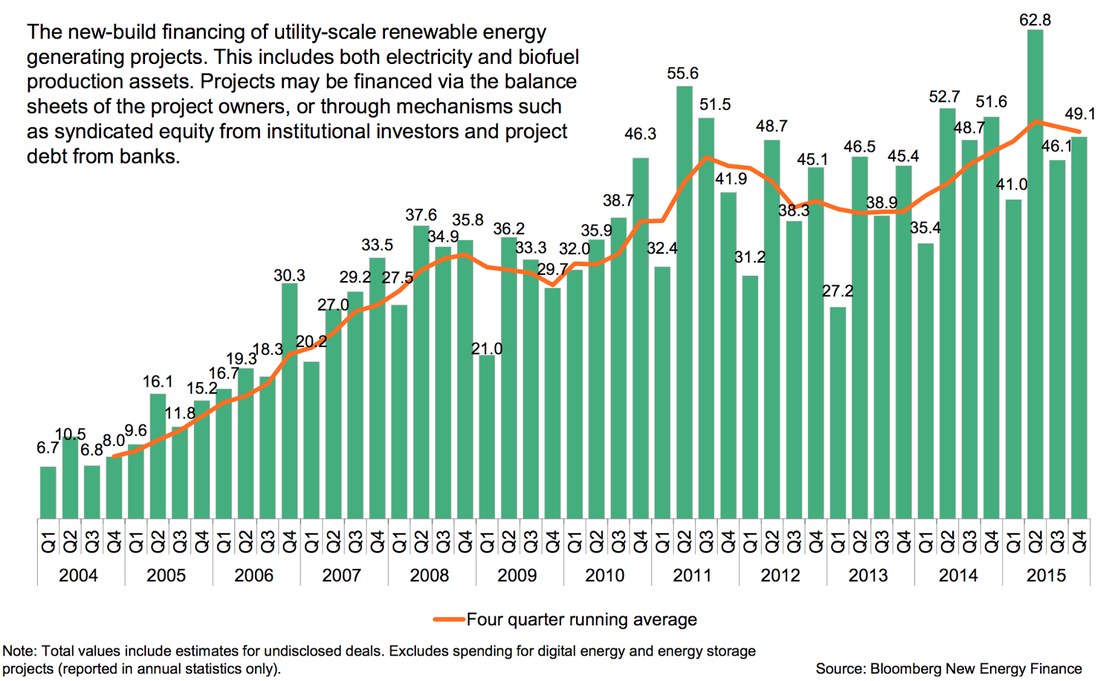

EIA bearish on renewables, despite reality on the ground Digging into the numbers, the EIA forecasts a bleak period of next to no growth in non-hydro renewables until nearly 2030. In fact, projections to 2040 have renewables at only 16% of the U.S. energy portfolio (currently at 12%), while natural gas continues to grow and even coal only decreases marginally. So, for the next 24 years, the EIA would have us believe that we should get prepared for...very incremental shifts from the present day status quo. Not nearly the renewable energy transition that we would hope for. Now, on the one hand, the U.S. electricity generation stock is absolutely massive, and the inertial pull of path dependency and legacy infrastructure investments will anchor the electric grid for decades to come. This general sentiment likely colors the views of the EIA. But the plain fact of the matter is that this supposition is being undermined left and right by the remarkable growth in distributed generation development, growth that has been consistently, bordering on intentionally, dismissed in the EIA’s future projections. EIA bullish on coal, again despite reality on the ground Why does the EIA remain bullish on coal, an industry that is undergoing a massive contraction with few new plants scheduled to come on line and many more being taken off? On the other side of the coin, why does the EIA remain so tepid about acknowledging the clear shift in the energy market towards cheap, clean distributed energy? The answer is anyone’s speculation, and there has been a long-running and healthy debate captured nicely here. Many concerns revolve around the lagged cost and price information that the EIA promulgates, which perhaps indicates the workings of a slow government bureaucracy. But is that really an excuse, when there are abundant publicly available datasets that detail distributed energy development and economics from the ground up? More important than diagnosing this systemic bias is the fact that EIA projections are used to inform U.S. government policy. Many are working to combat the anchoring effect of EIA (see here and here), and there is growing awareness that the EIA does not have the final word on what is happening in the dynamic energy industry. Forecasting the future of energy may be a fool’s errand, but let’s hold EIA to a higher standard Energy forecasts are as plentiful as they are wrong. It is not surprising that the EIA, like many other agencies and research groups gazing into our energy future, has not hit the mark on their forecasts. What is more worrying is that even their data on our current energy system is misrepresentative of the reality on the ground. At risk of being a bit blasphemous, let’s suppose that scientists are not always objective, which if you assume is the case with the EIA, then you have to start wondering what is the agenda behind presenting such a skewed picture in their datasets and reports. Perhaps it is benign neglect of the changing energy landscape beneath their feet, or maybe it is that the movement towards distributed renewables poses more of a threat to the status quo than many believe. Fortunately, there is some evidence that the EIA may finally be ready to come clean (pun intended) on their energy forecasts, but until they do let us continue to cast a skeptical eye on what the EIA has to say about the transition to renewable energy. Institutional investors have been reluctant to invest in solar, until now Perceived risks have long dissuaded institutional investors from venturing too deep into solar investments. Fortunately, perceptions can change. Whereas once the solar industry was hampered by the perception that technology was risky, markets were untested, and policy uncertain, now the solar industry is increasingly seen as a low-risk infrastructure investment that is increasingly enticing for the less risk tolerant institutional investors out there. Asset Financing for New-Build Renewable Energy Assets ($B)  To be sure, the solar investment space is pulling in interest from institutional investors, but it is also being pushed out of many fixed income and treasury investments due to the extended period of low interest rates.

Now that those “risk-free” assets are now also return-free, investors are anxious to explore investments with stable and predictable yields, ideally that generate free cash flows. As solar performs more like an infrastructure investment, with contracted cash flows, predictable technology, and a very long runway of future demand, interest from institutional investors is piquing. The question is - can solar meet the scale and risk-return profiles that institutional investors require? Can clean energy projects match the capital and risk profiles to entice investment? There are many ways that institutional investors may want to increase their allocation in clean energy - green bonds, low-carbon investment funds, etc. — but here I am going to focus on direct investments in projects. Over the last decade, the solar industry has expanded into a highly diffused ecosystem comprised of a large range of developers, EPCs, OEMs (though many fewer of these), and financiers. On the financing side, the availability of debt and tax equity has been a key driver of where and what type of projects could be built, and sponsor equity providers have come in as the final layer of the capital stack. Many solar projects with stable cash flows for 15-20 years and limited construction risk can yield returns of 10% or more, which easily beats the returns that can be achieved in the bond market. To really catch the eye of an institutional investor, portfolio sizes need to be in the $100s of millions, ideally yielding unlevered returns of 8% or more. Though large scale projects and bigger portfolios of projects have started to come through the pipeline, it is still difficult for a single developer to create an investment opportunity of the scale and risk profile that serves the needs of institutional investors. Even when these investment opportunities exist, institutional investors are wary of direct investments that expose them to illiquidity or diversification risk. Because of this, much of institutional investment to date has been in providing debt restructuring or acquiring an equity stake in operating assets, as most investors do not want to take on development risk. This is changing, but this mismatch remains an obstacle for moving beyond opportunistic engagement with institutional investors. As a result, some funds specializing in clean energy and low carbon infrastructure investment have emerged to act as stewards of institutional dollars. But will this be enough to really jumpstart institutional investment into solar projects? Asset-backed securities hold the key to bringing institutional investors on board In reality, institutional funds are not going to become big players until a market emerges that can bundle clean energy projects into securities and match institutional investor appetite. And given the predictable cash flows generated by solar projects with long-term PPAs interconnected in stable markets, these projects may actually lend themselves well to forming relatively low-risk, transparent, cash-generating securities. The key here boils down to risk mitigation. When a portfolio of solar project cash flows are pooled into one fund, that fund serves to protect the investor from the developer/sponsor’s corporate risk, which allows for standardized securities to be issued against the capital in that pool. Then, investors have a tradable security through which to commit capital to solar infrastructure investment. If these securities are well received in the market, they can create a virtuous cycle of demand-pull for the underlying asset, in this case solar. Beware: this virtuous cycle also occurred for the housing industry in response to mortgage-backed securities, so this positive feedback can have distortionary impacts on the market as well. At least presently, the solar industry does not seem to invite the same overzealous market speculation that threw the housing industry into a downward spiral. So, are we seeing the emergence of clean energy-backed securities to help leverage institutional investor capital? To some degree, the answer is yes. We can see this primarily in the rise of the green bond market. Bonds as a debt instrument, generate a contracted cash flow, which can back a security. The global green bond market grew to over $40B in 2015, a portion of which was asset-backed securities used to finance aggregate portfolios of smaller debt facilities into institutional investor-sized offerings. But there is a lot of work to do on expanding clean energy finance beyond the bond market. So, keep a lookout for innovations in solar securitization, as it holds the key to attracting institutional investors. Related data points:

Further reading:

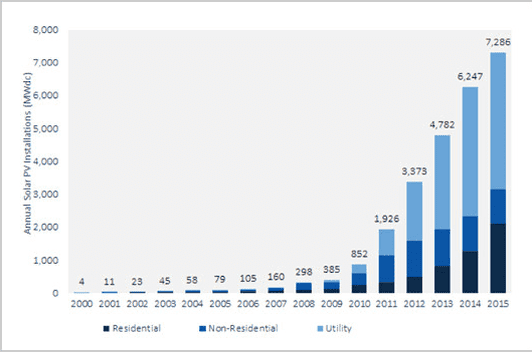

The post-mortem reports are coming in droves as SunEdison prepares to file for bankruptcy. There are many diagnoses of the fall of this giant, but the common thread running through all of them is that SunEdison wanted to become the preeminent market force in the solar industry, but lacked the patience to build to that stature without burdening the company with excessive risk. And that risk, largely in the form of over-leverage, has come back to bite them in a big way.

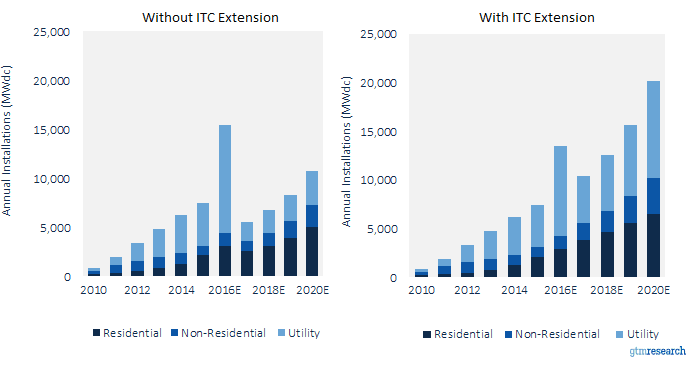

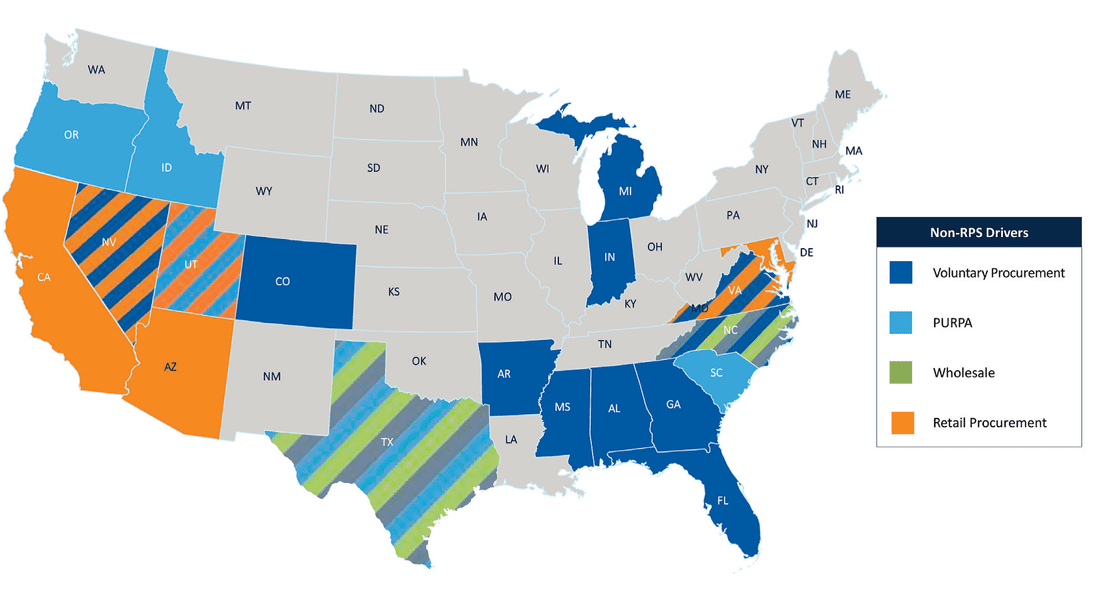

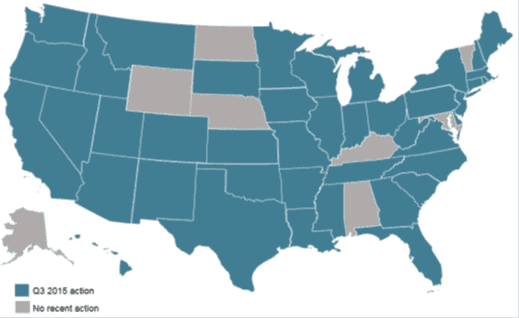

Until the last year or so, it seemed as though SunEdison was the most prescient player in the market. They took advantage of historically low interest rates to use leverage to build and acquire solar assets at an unprecedented pace. Of course, revenue growth could not keep up with the accumulation of what became nearly $12B of debt by 2015. It was a classic market share play gone awry. By the time they committed to this path, the solar industry was likely not large enough to accommodate the growth expectations baked into their corporate strategy. They had to start acquiring anything and everything, often through massive overbidding for projects, which further cut into their increasingly small margin for error. As a result, they have been hemorrhaging EBITDA since 2012. But, hey, Amazon did the same thing for years. The only difference is that this model does not work in infrastructure companies dealing in hard assets. Growth at all costs is not a sustainable strategy When you start on the growth hamster wheel, it is hard to find an opportune moment to get off. In order to maintain the illusion that SunEdison was still a financially sound company with healthy growth prospects, it had to double down time and again on their acquisition strategy, ultimately culminating in the failed attempt to acquire Vivint. That marriage was always going to be an awkward one, but it still lent SunEdison the air of being the most ambitious behemoth in the market, and maybe adding Vivint to the increasingly diverse cauldron of business lines could conjure something greater than the sum of its parts. But the convoluted amalgam of yieldcos and mergers only widened the breach in the hull. This has all come to a head with the proliferation of recent news that suggests that SunEdison has long been in internal panic mode. The Vivint deal was never consummated, and a nasty lawsuit is on the horizon. The relationships with Terraform Power and Terraform Global are as tenuous as ever, various executives have left (of their own volition or not, who is to say), and there are a number of investigations into the accounting and financial reporting practices at the company. SunEdison’s debacle is an anomaly, but still serves as a cautionary tale There is no telling how the bankruptcy proceedings will play out, but it is certainly going to entail a massive sell-off of SunEdison’s assets to pay off creditors. This has already started in India, where they recently announced 450 MW of projects for sale. Whether SunEdison can emerge from the wreckage with anything intact is anyone’s guess. And whether there was actual merit in their growth strategy is also a point of contention. You can add SunEdison to the Abengoa’s of the recent past—cautionary tales in how growing too big, too fast, and with too sprawling and risky of a corporate strategy can lead to truly fantastic collapses. The naysayers may point to SunEdison as evidence of some underlying weakness in the value proposition of solar for large developers and investors. But when you look closely at the autopsy, you can see clear signs that this giant was destined to fall under the weight of over-leverage, rapid expansion into risky markets, suspect acquisitions, and perhaps a bit of hubris from management. In the backdrop of the sensational demise of SunEdison, companies such as First Solar and SunPower have been excelling in the current market environment. In our previous monthly reports we have focused on state solar policies. Our research indicated a growing trend among state legislators and regulators to review, amend, and in several cases, phase out or even cancel solar incentives and long-standing, proven solar policies. Although this process could be viewed as a natural regulatory action in response to a market reaching maturity, it has nonetheless taken its toll on the solar market. After the Nevada Public Utility Commission’s controversial December 2015 decision to slash net energy metering, many residential solar installation companies halted operations in Nevada, with giants like SolarCity and Sunrun exiting the state. Similarly, Michigan’s legislature is considering a change to its solar policy that will reimburse generators at wholesale rather than retail rate, making the state’s thriving solar industry nervous. In February, Massachusetts reached its net metering and REC caps, halting operations of solar developers and installers in a state that has more solar jobs than any other state except California. And North Carolina’s lucrative solar tax credit is set to expire at the end of this year, creating uncertainty and concern among local industry players in one of the nation's largest solar markets. Policy uncertainty is never a good thing. However, what many state-level regulators and legislators tend to forget is that keeping policies unchanged is not enough; to continue to grow, the solar industry needs certainty as much as it needs stability. In a constantly changing regulatory environment, threats are almost as much of a problem as actual changes. Initiatives to review or amend policies, increase rates, or decrease incentives make investors wary of new investments, thereby escalating the cost of raising capital. Thus, while DC legislators have contributed their share to the national effort to create certainty and stability in the solar market, state legislators are failing to do their part. This is rather sad news for the solar industry that celebrated the ITC extension, but relies on states’ policies to continue driving investments in solar energy. Indeed, renewable portfolio standards account for more than 50% of investments in utility solar, and net energy metering is considered the main driving force behind residential rooftop solar. However, it is not all grim for the solar industry. Despite the uncertainties from state to state, the industry continues to grow. The quarterly SEIA/GTM Research U.S. Solar Market Insight report for Q4 2015, released in early March, predicts that the solar market will grow 119% in 2016. As in previous years, most of the projected added capacity is attributed to utility scale installations. But if many states are not providing the stable regulatory framework required for a healthy business environment, where is this substantial projected growth in utility scale solar coming from? Before Congress extended the ITC, the 30% tax benefit for solar installations was set to drop to 10% on January 1, 2017, and to expire in 2018. This tax cliff created an incentive to bring as many projects as possible online before the 2017 drop down, thus driving the unprecedented expected growth in 2016. Utility scale installations require long planning and development, so although the ITC was extended last year, it was too late for players to react to the new tax environment. This is why installations in 2017 are expected to fall significantly, while commercial and residential PV will be less affected. The effect of the ITC extension on the different solar sectors can be seen in the graph below. U.S. PV Installations With and Without ITC Extension, 2010-2020  (Source: GTM Research) Moreover, there is another federal framework that drives investments in utility scale solar. Unbeknownst to many, the federal Public Utility Regulatory Policies Act of 1978 (PURPA) is gradually emerging as a useful tool for utility scale developers in a post-RPS world. Enacted in response to the 1973 energy crisis, PURPA imposes a mandatory obligation on utilities to purchase renewable energy from “Qualified Facilities” (QF) at the utility’s avoided cost. To meet the requirements for a QF, an energy-generating facility must not exceed 80 MW and its primary energy source must be biomass, waste, geothermal, or renewable resources. With prices per megawatt-hour in the $40 to $60 range, utility solar is at cost parity with natural gas, making it a strong competitor in PURPA’s avoided cost markets. In 2015 over 500 MW of PURPA-driven projects came online in North Carolina, and states like Texas, South Carolina, Utah, Oregon, and Idaho are also leading the way in utilizing PURPA for utility scale solar. States With >50 MWdc Non-RPS Utility PV in Development  (Source: GTM Research)

As a federally mandated purchase, PURPA solar projects are not subject to state solar caps. Moreover, FERC regulations define “avoided cost” as the incremental costs to an electric utility of electric energy, capacity, and environmental externalities fees which the utility will incur if not purchasing electricity from the QF. The broad definition of “avoided cost” allows more facilities to enjoy QF status. However, despite the seemingly positive outlook for PURPA’s potential for solar developers, one must remember that it is very hard to enforce a PPA on a utility that does not want to enter one. One way of deterring QF developers from engaging with uninterested utilities is to propose terms and conditions that are more onerous to the QF than to non-PURPA counterparties. While FERC has succeeded at curtailing such practices, bad faith negotiation tactics are hard to prove and only few developers are willing to pursue costly litigation in an effort to obtain a PPA with an obstinate utility. To reduce transaction costs and assist smaller developers in negotiating with utilities, certain states have adopted standard contract rates for QFs of up to 10 MW (California up to 20). The standard contract makes it nearly impossible for utilities to avoid purchasing electricity from QFs. It is therefore not surprising that utilities in leading solar PURPA states are requesting utility commissions to reduce standard rates contracts caps. Late in March, the Oregon PUC approved Pacific Power’s request to reduce the eligibility cap for solar generation at QFs to three from ten MW, and a similar motion by Duke Energy was rejected by the North Carolina PUC late last year. As the price for solar generation continues to drop, we are expecting to see more PURPA driven PPAs across the nation. Whether PURPA PPAs will provide the necessary certainty and stability the market is currently lacking depends on FERC’s willingness to enforce its rules on avoided cost mandatory purchases, and Public Utility Commissions’ ability to withstand utility pressure to reduce standard contracts rates caps. Energy storage offers too many behind-the-meter benefits to consumers and grid operators to not become a common, if not essential, part of commercial PV projects. The myriad benefits of energy storage validate the basis of a beloved food analogy: “Energy storage is the new bacon—it makes everything better.”

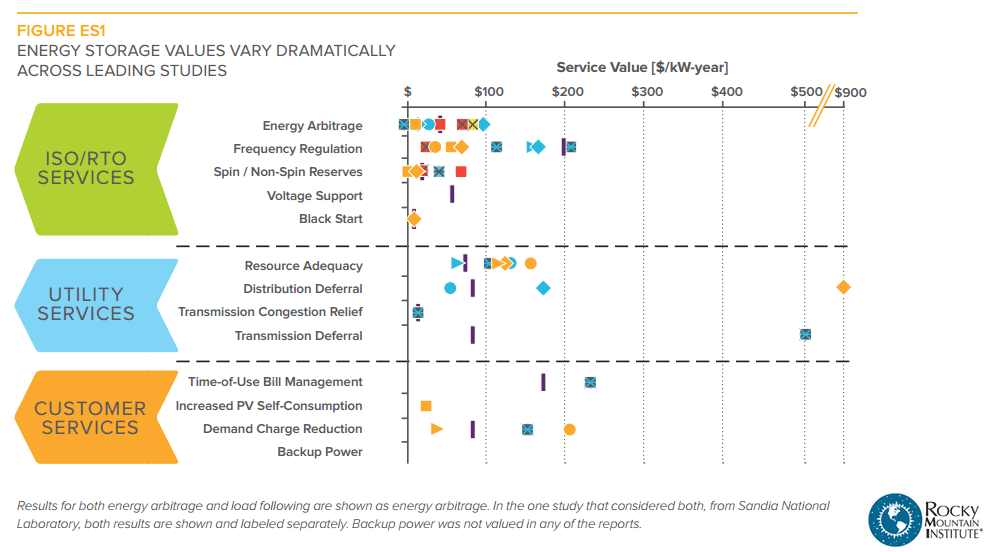

The consumer-centric benefits are the most widely discussed, and they usually focus on shaving peak demand by reducing costly demand charges for commercial customers. In addition to mitigating demand charges, solar plus storage allows end users to benefit from time-of-use bill management, backup power availability, and increased PV self-consumption. Moving up the food chain, utilities can use energy storage to achieve resource adequacy, transmission congestion relief, and transmission deferral. Finally, Independent System Operators, or ISOs, benefit greatly from energy storage predominantly by increasing frequency regulation, but also via voltage support and energy arbitrage. PJM’s Atlantic-coast-to-Illinois territory became the first ISO to provide monetary incentives ($40-$50 per MWh) for grid-scale storage that directly addresses frequency regulation. On a related note, let’s talk about those scary “death spirals.” The U.S. energy storage market will be 8 times bigger in 2020 than it was in 2015, reaching 1.6GW of installed storage capacity. By 2020, the utility death spiral will have fully taken hold and grid defection will be occurring all over the country, right? I think not. In 2014, I contributed to a Rocky Mountain Institute paper called The Economics of Grid Defection, which seemed to briefly serve as a crystal ball for the nascent energy storage industry. But no more than two years after the report was released, even a modest amount of grid defection seems highly unlikely given the proactive efforts by utilities nationwide to design pilot projects and sustainable policies that integrate solar plus storage with existing grid infrastructure. The energy storage market will begin to resemble more of a shared economy rather than an increasing number of grid-defected silos. The availability of storage devices, both directly from the ramped up manufacturing as well as second-hand batteries from electric vehicles, will provide a sustained supply of storage assets to expand grid storage capacity. These are both compelling sources of affordable storage assets, and certainly a reason to believe the repeated headlines regarding anticipated drops in energy storage costs. The solar plus storage revolution is being driven by cost effectiveness and scalability, two key drivers that provide a strong signal for future growth. Navigating murky waters: Accessing the ITC for solar + storage projects It’s inevitable that developers compare the benefits of energy storage to the well understood benefits of solar PV systems. The reality is that the technology for deploying and optimizing energy storage is much more complicated than solar, which impacts the bankability and clear financing strategies needed for exponential capacity growth. Prioritized revenue streams from solar plus storage projects include basic kWh production from PV, in addition to the benefits derived from stored, dispatchable electricity when rates are peaking to shave off much more demand charges than solar could have ever done on its own. Aside from contracted revenue from the end user, determining the ability for solar plus storage projects to qualify for the 30% ITC (Investment Tax Credit) is a critical factor for getting projects to hit desired investment return thresholds. Solar plus storage installations qualify for the 30% ITC, but developers need to pay close attention to system design to ensure that the intended cost basis appropriately applies to the ITC’s rules and regulations. A few key insights include:

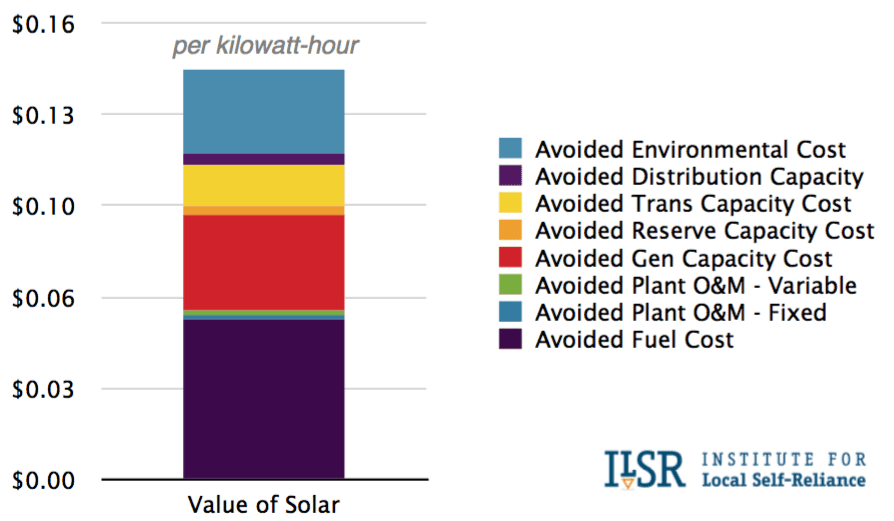

3/30/2016 What future Value of Solar policies could mean for the solar industry: 3 key things to knowRead Now There has been a wave of contentious net metering policy battles waged across the U.S. in 2016. Some net metering policies have remained largely intact, as in California, though much to the chagrin of the utilities. Other net metering policies, such as those in Nevada, have been fundamentally restructured, to put it kindly - though many would say they were just plain gutted. As with the ITC, a significant part of the solar industry formed around the net metering policy structure, and like many industries is reluctant to let go of such a foundational policy. But the aforementioned battles beg the question - is net metering the appropriate policy for solar looking to the future? Many believe that it has been a necessary stopgap policy measure, but not one that needs to live in perpetuity. One alternative that has been floated is the idea of a Value of Solar (VOS) policy that seeks to compensate solar based on a more nuanced understanding of the value that it provides to the grid. That is an easy enough idea to get behind, in theory, but just what could VOS mean for the industry?  (Source: Institute for Local Self-Reliance)